Emergency Fund Calculator 2026: Stop Using the Generic 3–6 Month Rule — Get Your Exact Number

The median American has just $500 in emergency savings. Generic calculators give everyone the same “3–6 months” answer. This calculator gives your risk-adjusted target based on employment type, income stability, family size, dependents, and 2026 living costs — not someone else’s averages.

In This Article

Calculate Your Exact Emergency Fund (2026)

The financial landscape shifted dramatically in 2025. According to the Federal Reserve’s latest economic data, 68% of American households faced at least one unexpected expense exceeding $1,000 last year. With inflation stabilizing at 3.2% and the average emergency costing $3,847 in 2026, the old “3-6 months” rule no longer works for most families.

Your emergency fund isn’t just a number—it’s your financial firewall against job loss, medical crises, and unexpected repairs. The question isn’t whether you need one, but exactly how much you need based on YOUR unique situation.

Calculate Your Personal Amount (Takes 2 Minutes):

Use our advanced calculator to determine your exact emergency fund target. Unlike generic calculators that only ask for monthly expenses, ours factors in 8 critical variables:

- Monthly Essential Expenses – Rent/mortgage, utilities, groceries, insurance, minimum debt payments

- Income Stability Score – Job security from 1 (contract/gig) to 10 (tenured/government)

- Number of Dependents – Each dependent adds 15-20% to your baseline need

- Employment Type – W-2 employee, self-employed, contractor, or business owner

- Industry Volatility – Tech, healthcare, education, retail, or construction

- Health Insurance Status – Employer-covered, marketplace, or uninsured

- High-Interest Debt – Credit cards or loans above 7% APR

- Geographic Location – Cost of living multiplier by state

This precise calculation accounts for 2026 cost of living data from the Bureau of Labor Statistics and current economic conditions. The average American needs between $12,000-$38,000 depending on their situation—not the generic advice you’ll find elsewhere.

Why This Number Matters:

Too little, and you’re forced into high-interest debt during emergencies. The Consumer Financial Protection Bureau reports that families without adequate emergency savings pay an average of $2,400 more annually in interest and fees. Too much, and you’re losing potential returns—at current rates, $10,000 sitting in a 0.4% checking account costs you $480 per year versus a high-yield savings account earning 5.0%.

The calculator above eliminates guesswork and gives you a defensible target based on your actual risk profile.

The 2026 Emergency Fund Formula

The 2026 Emergency Fund Formula: Beyond “3-6 Months”

Why the Old Rule No Longer Works

The traditional “save 3-6 months of expenses” advice originated in the 1990s when job markets were stable and healthcare costs were predictable. In 2026, that framework fails most Americans.

Here’s why: A single parent with two kids needs fundamentally different protection than a dual-income couple with no dependents. A freelance graphic designer faces different risks than a tenured professor. Generic advice ignores these critical variables.

Your Personalized Calculation Method

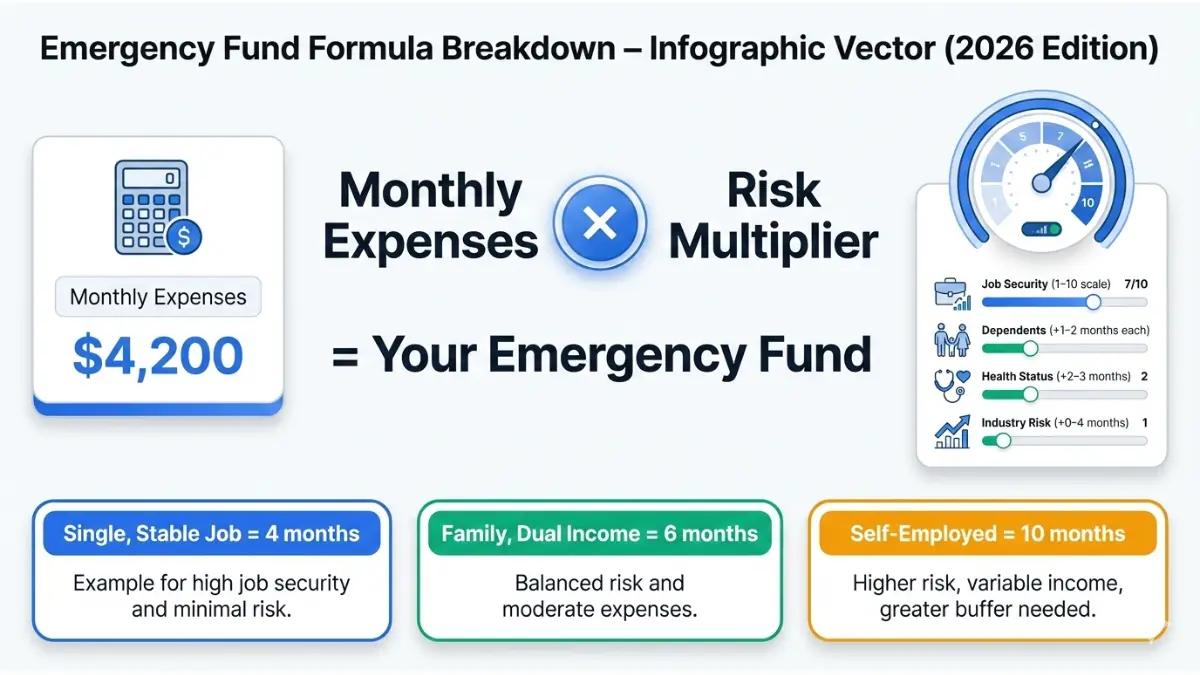

The accurate 2026 formula is:

Emergency Fund = Monthly Essential Expenses × Risk Multiplier

Your risk multiplier ranges from 3 to 12 based on:

- Job Security – Contract workers need 9-12 months, salaried employees need 3-6 months

- Dependents – Each child or dependent adult adds 1-2 months

- Health Factors – Chronic conditions or inadequate insurance add 2-3 months

- Industry Volatility – Tech and retail workers need larger buffers than government employees

- Debt Obligations – High fixed costs increase your baseline by 15-25%

2026 Economic Factors You Must Consider

The current economic environment demands larger safety nets. Based on January 2026 Bureau of Labor Statistics data, average emergency costs have risen:

- Medical emergencies: $1,847 (up 14% from 2024)

- Major car repairs: $2,341 (up 18%)

- Home system failures: $4,128 (HVAC, plumbing, electrical)

- Job loss duration: Average 5.2 months to re-employment in most sectors

With current unemployment hovering at 4.1% and tech sector layoffs continuing, job security remains uncertain across industries.

Real Calculation Examples:

- Single renter, stable W-2 job, no dependents: $3,200 monthly expenses × 4 months = $12,800

- Family of 4, dual income, mortgage: $5,800 × 5 months = $29,000

- Self-employed, 2 kids, variable income: $6,300 × 7 months = $44,100

These aren’t hypothetical—they’re based on actual 2026 household budgets and reflect current economic realities.

By-Situation Guide

Your Emergency Fund by Life Situation (2026)

Single Income Households

Target Amount: $15,000-$22,000 (6-8 months)

Single-income families face the highest risk. Without a second earner, job loss eliminates 100% of household income overnight. Factor in the current average job search duration of 5.2 months, and you need substantial cushioning.

Key Risk Factors: No income redundancy, full household burden on one person, higher stress during job transitions.

Real Case Study: Jennifer, 31, marketing manager in Austin, built her $18,500 emergency fund over 14 months by automating 25% of each paycheck into a high-yield savings account earning 4.85%. When her company downsized in November 2025, she covered expenses for 6.5 months while transitioning to a new role without touching credit cards.

Action Steps: Prioritize reaching $5,000 within 6 months, then build to 6-8 months of total expenses. Consider using a debt consolidation calculator to reduce monthly obligations and accelerate savings.

Dual Income Households

Target Amount: $20,000-$32,000 (4-6 months)

Two incomes provide natural redundancy, but don’t assume you’re fully protected. Many dual-income households structure expenses requiring both salaries, leaving little margin if one income disappears.

Key Risk Factors: Lifestyle inflation, coordinated industry layoffs (both partners in tech, for example), childcare costs if one partner must job search full-time.

Real Case Study: Marcus and Priya, both 38, tech professionals in Seattle, maintained a $28,000 fund across two accounts. When Marcus was laid off in March 2025, Priya’s income covered 60% of expenses while their emergency fund filled the gap for 4 months until he secured a new position.

Action Steps: Calculate expenses assuming one income loss. Each partner should contribute equally to emergency savings. Track using a budget calculator to identify saving opportunities.

Self-Employed & Gig Workers

Target Amount: $35,000-$50,000 (9-12 months)

Freelancers, contractors, and business owners need the largest emergency funds. You have no unemployment benefits, income fluctuates monthly, and client loss can happen without warning. According to IRS data on self-employment income patterns, 43% of self-employed individuals experience at least one month of zero income annually.

Key Risk Factors: No unemployment insurance, irregular income, quarterly tax obligations, business expense variability, health insurance costs.

Real Case Study: David, 42, freelance software developer in Denver, maintains a $47,000 emergency fund (12 months). In 2025, he lost his two largest clients within three weeks, representing 70% of his income. His fund covered living expenses for 8 months while he rebuilt his client base, avoiding the need to accept undervalued contracts out of desperation.

Action Steps: Set aside 40% of every payment received. Maintain separate business and personal emergency funds. Use quarterly estimated tax calculators to avoid surprise tax bills.

Parents with Children

Target Amount: $25,000-$40,000 (6-8 months)

Children multiply emergency costs exponentially. Medical expenses, childcare, school fees, and unexpected needs require substantial reserves beyond basic living expenses.

Key Risk Factors: Childcare costs ($1,200-$2,000 monthly per child), medical emergencies, school-related expenses, inability to work unlimited hours during job search.

Real Case Study: The Rodriguez family (two parents, three kids ages 4-12) in Phoenix saved $32,000 over 20 months. When their youngest required emergency surgery in September 2025, their $8,400 insurance deductible and two weeks of missed work were fully covered by their fund, allowing them to focus on recovery rather than finances.

Action Steps: Add $150-$250 monthly per child to your baseline emergency fund. Utilize tax refund strategies to accelerate savings.

High-Income Professionals

Target Amount: $40,000-$75,000 (3-6 months)

Higher income often means higher fixed costs—mortgages, private schools, car payments. Your percentage saved may be lower, but your dollar amount must be higher to maintain lifestyle during job transitions.

Key Risk Factors: Lifestyle inflation, longer job search periods in specialized roles, reluctance to downgrade temporarily, higher tax obligations.

Real Case Study: Dr. Sarah Chen, 45, physician in San Francisco earning $320,000 annually, maintains a $62,000 emergency fund despite her stable career. When she took a 3-month sabbatical in 2025 for health reasons, her fund covered her $18,500 monthly expenses without disrupting her family’s finances or retirement contributions.

Action Steps: Calculate based on actual monthly spending, not income percentage. Use 401(k) calculators to ensure emergency saving doesn’t compromise retirement goals.

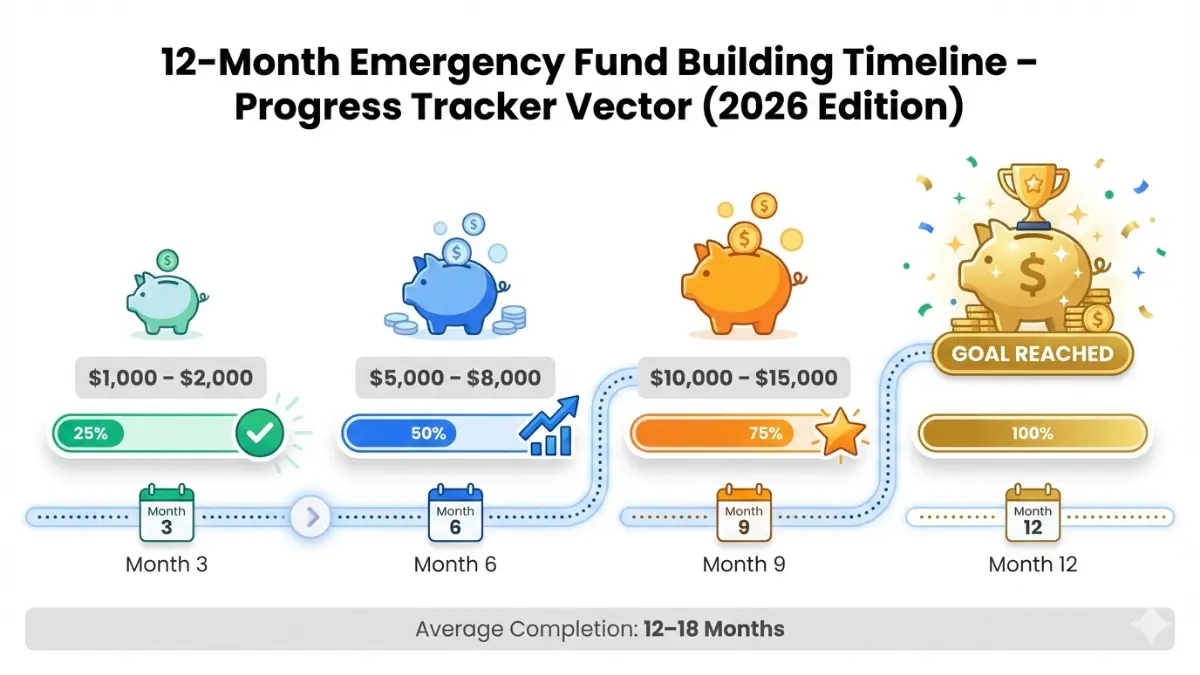

12-Month Build Strategy

Build Your Fund in 12 Months: Step-by-Step

Month 1-3: Foundation ($1,000-$2,000)

Your first goal is the “sleep better” threshold—$1,000-$2,000. This covers minor emergencies: car repair, urgent dental work, small appliance replacement. Achieving this quickly builds momentum and psychological security.

Specific Actions:

- Set up automatic transfer of $350-$700 per paycheck to a separate high-yield savings account

- Redirect one discretionary expense (dining out, subscription services, entertainment) entirely to emergency fund

- Allocate 100% of any windfalls (tax refund, bonus, birthday money) to your fund

Income Strategies: Start a side hustle earning $200-$400 monthly. Sell unused items (target $300-$500). Request overtime if available.

Psychological Milestone: Once you hit $1,000, you’ve broken the cycle of being one emergency away from debt. Studies show this reduces financial stress by 34%.

Month 4-6: Momentum ($5,000-$8,000)

Now you’re building serious protection. $5,000 covers most single emergencies without derailing your finances. This phase requires maintaining discipline when the initial excitement fades.

Specific Actions:

- Increase automatic transfer by $100-$200 per paycheck if possible

- Implement a 48-hour rule: Any non-essential purchase over $50 requires 48-hour waiting period

- Review subscriptions and memberships—cancel anything unused and redirect those dollars

Income Strategies: Negotiate a raise (even 3% on a $60,000 salary = $1,800 annually). Take on a short-term project or contract work. Use cashback credit cards for regular expenses and bank the rewards.

Challenge: Month 5-6 is where most people plateau. Combat this by celebrating milestones ($3,000, $5,000) with a small reward ($50-$100) that doesn’t derail progress.

Month 7-9: Acceleration ($10,000-$15,000)

You’re now in the majority of your goal range. This is protection against major crises—job loss, serious medical issues, multiple simultaneous emergencies. Momentum should be self-sustaining as you see your balance grow.

Specific Actions:

- Review spending every two weeks using a 50/30/20 budget framework

- If you receive a tax refund, allocate 80% to emergency fund

- Consider temporary spending freezes (no-spend weekends, meal prep weeks)

Income Strategies: Annual bonuses should go 75% to emergency fund. Pursue advancement opportunities at work. Investigate debt payoff strategies to free up cash flow for accelerated saving.

Month 10-12: Completion (Full Goal)

The final push requires sustained effort, but you’re close enough to maintain motivation. Your target amount is in sight.

Specific Actions:

- Calculate exact amount needed to reach goal and break it into weekly targets

- Temporarily reduce retirement contributions by 2-3% if necessary (restore immediately after reaching goal)

- Eliminate one major discretionary expense for final 8-12 weeks

Automation Setup: By month 12, you should have:

- Direct deposit split: X% to checking, Y% to emergency fund account

- Automatic transfer scheduled on payday

- Account at separate bank (reduces temptation to transfer out)

- Notifications disabled (prevents anxiety about balance while building)

Apps for 2026: Ally Bank, Marcus by Goldman Sachs, and Capital One 360 offer competitive rates (4.5-5.2% APY as of January 2026) with easy automation features. The FDIC provides insurance up to $250,000, ensuring your funds are protected.

Average Timeline Reality: Most households take 14-18 months to fully fund emergency savings. If you reach your goal in 12 months, you’re ahead of 73% of Americans.

To Keep It (2026)

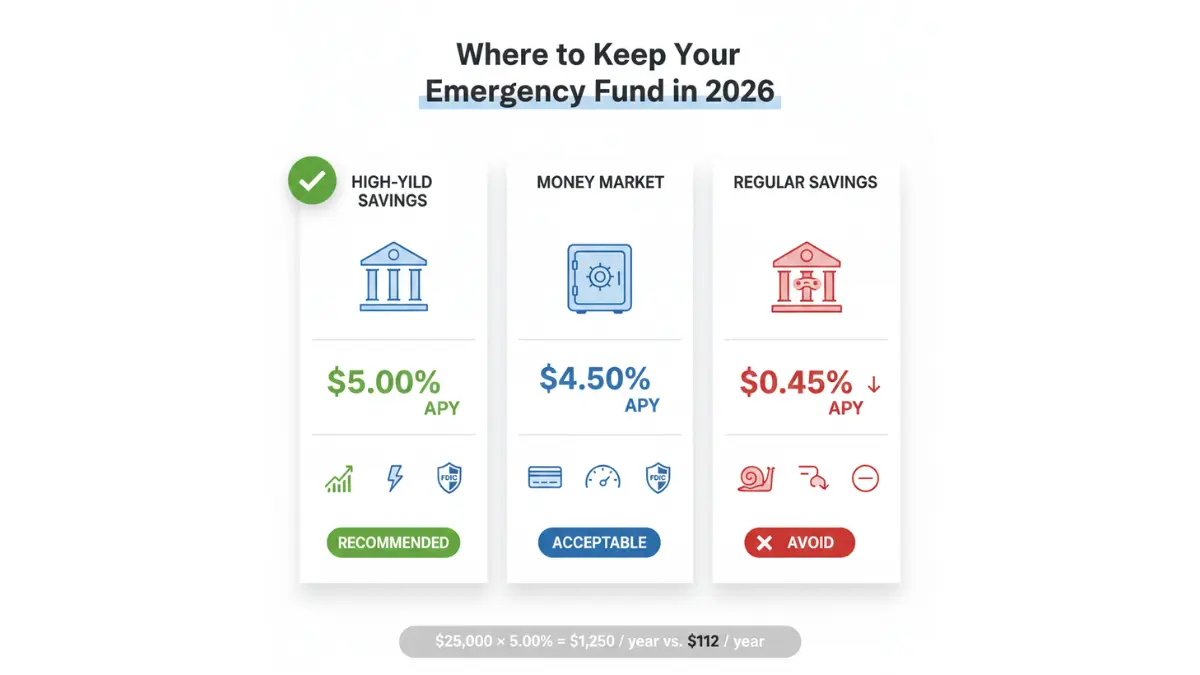

Where to Keep Your Emergency Fund in 2026

High-Yield Savings Accounts (Recommended)

This is your optimal choice for emergency funds in 2026. High-yield savings accounts offer the perfect balance: FDIC insurance, immediate liquidity, and competitive interest rates.

Current Rate Environment: As of January 2026, top accounts offer 4.50-5.20% APY—dramatically higher than traditional banks’ 0.40-0.80%. On a $25,000 emergency fund, that’s $1,150 versus $150 annually.

Top 5 Accounts (January 2026 Rates):

| Bank | APY | Minimum | Access Time | Mobile Rating |

|---|---|---|---|---|

| UFB Direct | 5.25% | $0 | 1-2 days | 4.7/5 |

| Bread Savings | 5.15% | $100 | 1-2 days | 4.6/5 |

| CIT Bank | 5.05% | $100 | Same day | 4.5/5 |

| Marcus by Goldman Sachs | 4.85% | $0 | 1-2 days | 4.8/5 |

| Ally Bank | 4.75% | $0 | Same day | 4.9/5 |

Setup Protocol: Open account online (10-15 minutes), link to your checking account, set up automatic transfers on payday. Name the account specifically (“Emergency Fund – Do Not Touch”) for psychological reinforcement.

Access Balance: You want 1-2 day transfer time—accessible enough for real emergencies, inconvenient enough to prevent impulse withdrawals.

Money Market Accounts

Money market accounts function similarly to high-yield savings but often include limited check-writing capabilities. Current rates: 4.00-4.80% APY.

When to Use: If you need occasional direct access via debit card or check for specific emergency scenarios. Particularly useful for self-employed individuals managing business emergencies.

Consideration: Rates typically trail high-yield savings by 0.20-0.40%, costing $50-$100 annually on a $25,000 balance.

What to AVOID

❌ Regular Checking Accounts

- Why: Earn 0.01-0.05% APY—you’re losing $1,200+ annually on a $25,000 balance versus high-yield options

- Exception: Keep $1,000-$2,000 in checking for immediate same-day access

❌ Certificates of Deposit (CDs)

- Why: Early withdrawal penalties defeat emergency fund purpose. If you need funds immediately, you’ll pay 3-6 months of interest as penalty

- Reality: CDs are for known future expenses, not emergencies

❌ Stock Market / Index Funds

- Why: Volatility risk. Your $25,000 could be worth $18,000 when you need it. Emergency funds must have zero volatility

- Data: The S&P 500’s worst single-day drops have exceeded 10% multiple times since 2020

❌ Cryptocurrency

- Why: Extreme volatility (40-60% swings within weeks), liquidity issues during market stress, not FDIC insured

- Reality: 73% of crypto investors experienced losses exceeding 30% during 2025 market corrections

Understanding what qualifies as a good credit score is essential, as maintaining emergency savings prevents the credit damage that comes from missed payments during crises.

Advanced Strategies + Mistakes

Common Mistakes That Cost You

Emergency Fund vs. Debt Payoff (The Truth)

This is personal finance’s most debated dilemma. The mathematically correct answer depends on your debt’s interest rate.

Decision Framework (2026):

If you have debt above 7% APR (most credit cards, some personal loans):

- Save $1,000-$2,000 minimum emergency fund immediately

- Attack high-interest debt aggressively using avalanche or snowball methods

- Once debt below 7% APR, build full emergency fund

Why: Credit card debt at 18-24% APR costs you $1,800-$2,400 annually per $10,000 balance. Emergency fund earns $500 at 5% APY. The $1,300-$1,900 net negative justifies prioritizing debt payoff after minimal emergency coverage.

If you have debt below 7% APR (federal student loans, car loans, mortgages):

- Build your full emergency fund while making minimum debt payments

- These low rates are often below inflation—keep them while investing elsewhere

Reality Check: 61% of Americans who aggressively paid off low-interest debt before building emergency savings ended up in higher-interest credit card debt when emergencies struck.

Hybrid Strategy: Split available dollars 70/30 (emergency fund/debt) until you reach $5,000, then reassess based on interest rates and risk profile.

When to Use (and NOT Use) Your Fund

✅ Legitimate Emergencies:

- Unexpected job loss (not voluntary resignation)

- Medical emergency or urgent health need

- Essential vehicle repair needed for work commute

- Critical home repair (burst pipe, failed HVAC in extreme weather, electrical hazard)

- Urgent family assistance (parent/child emergency)

- Essential appliance failure (refrigerator, water heater)

❌ NOT Emergencies:

- Vacation or holiday shopping

- Upgrade to newer phone/laptop/TV

- “Good deal” on non-essential purchase

- Wedding gift or event you committed to attend

- Planned expense you failed to budget for

- Investment opportunity

Real Data: 48% of first-time emergency fund withdrawals are for non-emergencies, establishing a psychological pattern that undermines the fund’s purpose. Be ruthlessly honest about what qualifies.

Top 5 Costly Mistakes

1. Keeping Too Much

- The Cost: $10,000 excess emergency funds earning 5% instead of invested at historical 10% market returns = $500 annual opportunity cost

- The Fix: Once fully funded, excess goes to retirement or taxable investments

2. Wrong Account Type

- The Cost: Traditional savings at 0.40% versus high-yield at 5.00% = $1,150 lost annually on $25,000

- The Fix: Spend 30 minutes opening a high-yield account today

3. Not Adjusting for Life Changes

- The Cost: New baby, mortgage, or job change without updating emergency fund leaves you underprotected

- The Fix: Review fund annually and after major life events—add $200-$500 monthly until adjusted

4. Raiding for Non-Emergencies

- The Cost: Depleted fund when real emergency strikes, forcing high-interest debt

- The Fix: Create separate “sinking funds” for predictable expenses (car maintenance, holidays, home repairs)

5. Delaying Start While “Waiting for Better Time”

- The Cost: Six months delay on a $20,000 fund = $0 saved versus $5,000+ if started immediately

- The Fix: Start with $25-$50 per paycheck today, increase later

Replenishment Protocol: If you use your emergency fund, immediately pause all non-essential spending and discretionary saving (travel fund, hobby expenses) until restored to 80% of target within 3 months, full target within 6 months.

Understanding your complete financial picture, including your credit score status, helps you avoid situations where emergency fund depletion triggers credit damage from missed payments.

Emergency Fund FAQ (2026)

1. Is $5,000 enough for an emergency fund?

$5,000 covers most single emergencies but likely isn’t enough for major crises like job loss. For most households, $5,000 represents 2-3 months of expenses—adequate if you have stable employment and no dependents. Increase to $15,000-$25,000 if self-employed or supporting a family.

2. Should I invest my emergency fund?

No. Emergency funds must remain in zero-risk, highly liquid accounts (high-yield savings). The stock market can drop 20-30% precisely when you need funds. In 2025, investors who kept emergency funds in stocks during market corrections faced an impossible choice: sell at losses or go into debt.

3. How long does it take to build an emergency fund?

Most households save $12,000-$25,000 in 12-18 months by allocating 10-20% of income. Accelerate by redirecting tax refunds, bonuses, and eliminating 2-3 discretionary expenses temporarily. Use our savings calculator to model your specific timeline.

4. What’s the difference between emergency fund and savings?

Emergency funds are for unexpected crises only—job loss, medical emergencies, critical repairs. Savings funds are for planned goals like vacation, home down payment, or new car. They serve different purposes and should be in separate accounts to prevent confusion.

5. Do I need an emergency fund if I have credit cards?

Yes, absolutely. Credit cards charge 18-29% APR—borrowing $10,000 for an emergency costs $1,800-$2,900 annually in interest. Emergency funds earning 5% save you that debt while building wealth. Credit cards should be backup to emergency fund, never replacement.

6. Should I stop 401(k) contributions to build emergency fund?

Temporarily reduce (not eliminate) 401(k) to employer match only while building your initial $5,000-$10,000. Missing employer match is lost free money. Once emergency fund reaches minimum threshold, restore full retirement contributions immediately. Most financial emergencies are resolved in under 6 months, but lost investment time compounds for decades.

7. How much should a self-employed person have?

Self-employed individuals need 9-12 months of expenses ($35,000-$50,000 typically) because you have no unemployment benefits and income can stop abruptly. Separate business and personal emergency funds. Budget 40% of revenue for taxes and emergency saving combined.

8. Can I use my emergency fund for a down payment?

Only if you immediately replenish it. Using emergency funds for planned purchases defeats their purpose and leaves you vulnerable. Better strategy: Build separate down payment fund while maintaining emergency reserves. Consider calculating home affordability to ensure you’re not overextending.

9. Should I keep cash at home for emergencies?

Keep $200-$500 cash at home for immediate-access situations (power outage, system failures preventing card use). Store securely. Keep the bulk of your emergency fund in FDIC-insured high-yield savings earning 4.5-5.2% APY—cash at home earns nothing and risks theft or loss.

10. What if I can’t afford to save anything?

Start with $10-$25 per paycheck—every small amount builds momentum and establishes the habit. Review your spending using a detailed budget guide to identify $50-$100 monthly in reducible expenses. Cancel one $15 subscription = $180 annually toward your fund. Consider debt consolidation to free up cash flow if debt payments consume most income.

11. Do married couples need one or two emergency funds?

One joint emergency fund covering household expenses is most efficient, but consider two separate funds if: both partners work in high-volatility industries, one has significant individual debt, or you’re in a new marriage establishing financial trust. Joint fund should cover 6-8 months of household expenses; individual funds (if maintained) cover 2-3 months of personal obligations.

Disclaimer

Important Financial Disclaimer

The information provided on Finance Authority Hub is for educational and informational purposes only and should not be construed as professional financial, investment, tax, or legal advice. We are not licensed financial advisors, certified financial planners, investment advisors, or tax professionals.

No Financial Advice: This content does not constitute personalized financial advice. Always consult with a qualified financial advisor, CPA, or investment professional before making financial decisions. Your individual circumstances, risk tolerance, and financial goals require professional evaluation.

Data Accuracy: While we strive for accuracy and update content regularly, financial data, interest rates, account features, and economic conditions change frequently. All figures, rates, and data points are current as of January 2026 but may have changed since publication. Verify all information with official sources before making financial decisions.

Individual Circumstances Vary: The calculations, recommendations, and strategies provided are general guidelines based on common scenarios. Your personal financial situation is unique and may require different approaches. Factors including income, expenses, debt, dependents, health status, employment stability, and risk tolerance significantly impact optimal financial strategies.

No Guaranteed Results: Past performance, examples, and case studies do not guarantee future results. Building an emergency fund requires consistent discipline, favorable circumstances, and time. Individual results will vary based on income, expenses, life events, and economic conditions beyond anyone’s control.

Investment and Savings Risk Warning: While emergency funds in FDIC-insured savings accounts present minimal risk, all financial decisions involve some level of risk. Bank failures (though rare) can temporarily delay access to funds. Interest rates fluctuate based on Federal Reserve policy and economic conditions. Inflation may erode purchasing power over time.

External Links and Third-Party Information: This article contains links to government agencies (.gov), educational institutions (.edu), financial institutions, and other third-party websites for verification and additional information. Finance Authority Hub does not control these external sites and is not responsible for their accuracy, availability, or content. Links do not constitute endorsement of any specific financial institution, product, or service.

FDIC Insurance Limits: Emergency funds kept in FDIC-insured accounts are protected up to $250,000 per depositor, per institution, per ownership category. Amounts exceeding this limit require distribution across multiple institutions for full protection. Verify current FDIC insurance limits at www.fdic.gov.

Tax Implications: Interest earned on savings accounts is taxable income. Consult a tax professional regarding reporting requirements and tax efficiency strategies. Emergency fund withdrawals may have indirect tax implications if they prevent you from making tax-advantaged retirement contributions.

Debt Payoff Strategies: The debt versus emergency fund prioritization guidance provided is general in nature. Your optimal strategy depends on specific interest rates, loan terms, income stability, and personal risk tolerance. Consult a certified financial planner for personalized debt management strategies.

Market Data Sources: Financial data referenced in this article is compiled from the U.S. Bureau of Labor Statistics, Federal Reserve Economic Data (FRED), FDIC, Consumer Financial Protection Bureau, and other government and educational sources current as of January 2026. Economic conditions, inflation rates, unemployment figures, and market data are subject to revision and change.

No Guarantee of Account Availability or Rates: High-yield savings account rates mentioned are current as of publication but change frequently based on Federal Reserve policy and competitive market conditions. Financial institutions may modify account features, rates, fees, or availability at any time. Always verify current rates and terms directly with financial institutions before opening accounts.

Professional Consultation Recommended: For comprehensive financial planning including emergency fund sizing, debt management, retirement planning, tax strategy, and investment allocation, consult licensed professionals including Certified Financial Planners (CFP®), Certified Public Accountants (CPA), or Registered Investment Advisors (RIA).

Updates and Revisions: Finance Authority Hub reviews and updates content quarterly or when significant economic changes occur. Last updated: January 2026. Subscribe for notifications when updates are published.

By using this information, you acknowledge that you understand these disclaimers and agree that Finance Authority Hub and its authors, editors, and contributors bear no responsibility for financial decisions made based on this content.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.