Paycheck Calculator: Your Real Net Pay in 2026

Paycheck Calculator

Estimate take-home pay per paycheck and per year with detailed “paystub-style” breakdown, optional contributions, and either flat or progressive taxes (worldwide-friendly).

Inputs

Results

Net pay (per paycheck)

—

Gross: —

Income tax (per paycheck)

—

Withheld (tax + employee contrib): —

Take-home rate

—

Effective tax on taxable: —

Paychecks per year

—

Effective tax on gross: —

Annual totals (estimate)

Gross: — • Net: —

Income tax: — • Employee contrib: — • Total withheld: —

Pre-tax deductions: — • Post-tax deductions: —

Gross hourly (est): — • Net hourly (est): —

Representative paycheck (paystub-style)

If you set “bonus paid once”, only that paycheck will look different; the table below shows every paycheck.

- Flat tax: enter one % (simple).

- Progressive: enter your bracket caps and marginal rates.

- Employee contributions: use for social insurance, provident fund, etc.

- Employer contributions: shows “employer total cost” (useful for CTC-style comparisons).

Per-paycheck breakdown (1 year)

| Paycheck | Gross | Bonus | Pre-tax | Taxable | Income tax | Employee contrib | Post-tax | Net pay | Employer cost |

|---|

Results appear after you click “Calculate.”

In This Article

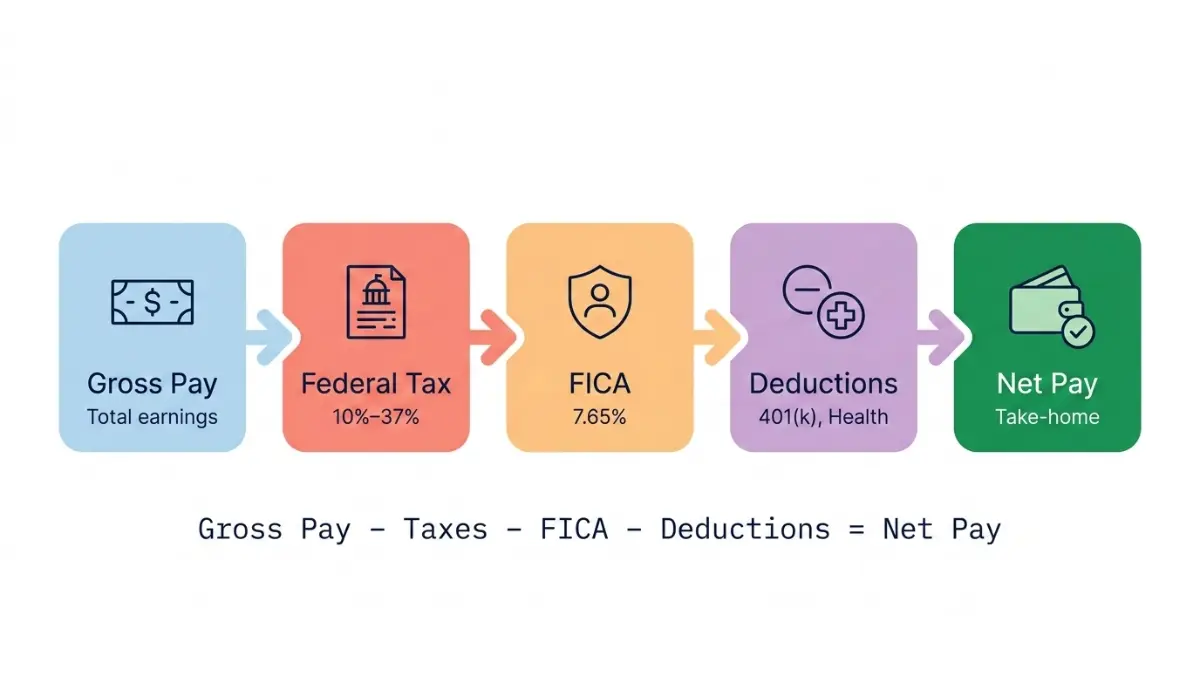

Your paycheck calculator shows your real net pay — what actually lands in your bank account after federal taxes, FICA, state taxes, and deductions are removed. For a $60,000 salary paid biweekly, most Americans take home roughly $1,529 per paycheck, not $2,307. The gap is taxes and deductions — and this guide explains every dollar.

The Formula: Gross Pay − Federal Tax − FICA − State Tax − Deductions = Net Take-Home Pay

Most Americans are surprised their paycheck is $400–$800 less than expected. You’re not alone — and by the end of this guide, you’ll know exactly why, and how to legally keep more.

How to Use This Paycheck Calculator (Salary & Hourly)

Our free paycheck calculator above handles salary workers, hourly employees, and international users across 22 currencies. Here’s how to get the most accurate net pay result in under 60 seconds.

Step-by-step:

- Choose Currency & Pay Frequency — Select USD, GBP, AUD, EUR, or 18 others. Pick weekly, biweekly, semi-monthly, monthly, or yearly.

- Select Salary or Hourly Mode — Salary mode: enter annual gross. Hourly mode: enter rate + regular hours + overtime hours per week.

- Enter Bonus & Commission — Add annual bonus (spread evenly or paid in one paycheck) and commission income.

- Add Pre-Tax Deductions — Enter your 401(k) percentage or fixed amount, health insurance premium per paycheck, and HSA contributions. These reduce your taxable income directly.

- Set Tax Mode — Use flat rate for a quick estimate. Switch to progressive brackets to enter your exact federal and state rates for maximum accuracy.

- Enter Employee Contributions — For US workers, enter 7.65% for FICA (Social Security + Medicare combined). For UK workers, use National Insurance rates.

- Click Calculate — See your net pay per paycheck, annual totals, effective tax rate, and a full paystub-style breakdown instantly.

| Input Field | What to Enter | 2026 Example |

|---|---|---|

| Annual Salary | Gross yearly pay | $60,000 |

| Pay Frequency | How often paid | Biweekly (26x/yr) |

| Pre-Tax 401(k) | % of gross per paycheck | 6% ($138/pp) |

| Health Insurance | Premium per paycheck | $75/pp |

| Employee FICA | Social Security + Medicare | 7.65% |

| Flat Tax Rate | Federal + state blended | 22% federal |

💡 Pro Tip: Toggle to progressive brackets and enter your actual state rate separately for a result that’s within 1–2% of your real paycheck.

If you earn hourly wages, pair this tool with our overtime calculator to model exactly how overtime hours affect your weekly take-home pay.

What’s Actually Deducted From Your Paycheck in 2026

This is what SmartAsset, ADP, and PaycheckCity don’t show you clearly. Here is every deduction line, with verified 2026 rates.

Federal Income Tax Withholding 2026

Federal income tax is progressive — meaning higher income is taxed at higher rates, but only on the income within each bracket, not your entire salary.

2026 Federal Tax Brackets (Single Filers):

| Taxable Income | Rate |

|---|---|

| $0 – $11,925 | 10% |

| $11,926 – $48,475 | 12% |

| $48,476 – $103,350 | 22% |

| $103,351 – $197,300 | 24% |

| $197,301 – $250,525 | 32% |

| $250,526 – $626,350 | 35% |

| Over $626,350 | 37% |

2026 Standard Deduction: $16,100 (single) | $32,200 (married filing jointly)

🆕 2026 Key Changes — One Big Beautiful Bill:

- Senior deduction: additional $6,000/year for individuals 65+ (phases out above $75,000 AGI)

- SALT deduction cap raised to $40,400 in 2026

- Standard deduction increased from 2025 levels

The IRS Tax Withholding Estimator helps you verify your W-4 is set correctly for these updated brackets.

FICA Taxes — Social Security & Medicare 2026

FICA is automatic and mandatory. It funds Social Security and Medicare programs for every W-2 employee in the US.

2026 FICA Rates:

| Tax | Employee Rate | Employer Match | Wage Cap |

|---|---|---|---|

| Social Security | 6.2% | 6.2% | $184,500 (↑ from $176,100) |

| Medicare | 1.45% | 1.45% | No cap |

| Additional Medicare | 0.9% | None | Over $200,000 (single) |

| Total Employee FICA | 7.65% | 7.65% | — |

FICA Impact by Salary Level:

| Annual Salary | Social Security Tax | Medicare Tax | Total FICA/Year |

|---|---|---|---|

| $50,000 | $3,100 | $725 | $3,825 |

| $75,000 | $4,650 | $1,088 | $5,738 |

| $100,000 | $6,200 | $1,450 | $7,650 |

| $184,500+ | $11,439 (max) | No cap | $11,439+ |

The Social Security wage base increase to $184,500 is confirmed by the Social Security Administration’s 2026 fact sheet. If you earn above this threshold, your Social Security deduction stops mid-year — a meaningful net pay increase in Q3/Q4.

Pre-Tax Deductions That Legally Lower Your Tax Bill

These deductions reduce your taxable income before any tax is calculated — the most powerful lever you have on your net pay.

2026 Pre-Tax Contribution Limits:

| Deduction Type | 2026 Limit | Tax Benefit |

|---|---|---|

| 401(k) Traditional | $23,500/year | Reduces federal + state taxable income |

| 401(k) Catch-Up (50+) | $31,000/year | Same + extra catch-up |

| HSA Individual | $4,300/year | Triple tax advantage |

| HSA Family | $8,550/year | Same |

| FSA (Medical) | $3,300/year | Pre-tax medical spending |

| FSA (Dependent Care) | $5,000/year | Childcare pre-tax |

Our detailed guide on HSA vs 401(k) tax strategy breaks down exactly how combining both accounts can save a $75,000 earner over $3,200 in taxes annually. For 401(k) contribution strategy, the IRS 401(k) resource page confirms all 2026 limits.

State Income Tax: What Changes by Location

State taxes vary dramatically and are the single biggest variable in your take-home pay calculator result.

| State | Income Tax | Notes |

|---|---|---|

| Texas, Florida, Nevada | 0% | No state income tax |

| Washington | 0% | No income tax (capital gains tax only) |

| California | Up to 13.3% | Highest in the US |

| New York | Up to 10.9% | NYC adds 3.0–3.9% local tax |

| New Jersey | Up to 10.75% | |

| Illinois | 4.95% (flat) | Flat rate state |

A $70,000 earner in Texas takes home approximately $6,800 more per year than an identical earner in California — purely from state tax differences. Use progressive bracket mode in our calculator and enter your exact state rate for pinpoint accuracy.

Real Paycheck Examples: Salary vs. Hourly Workers in 2026

These are real calculations using 2026 IRS rates — not hypothetical estimates.

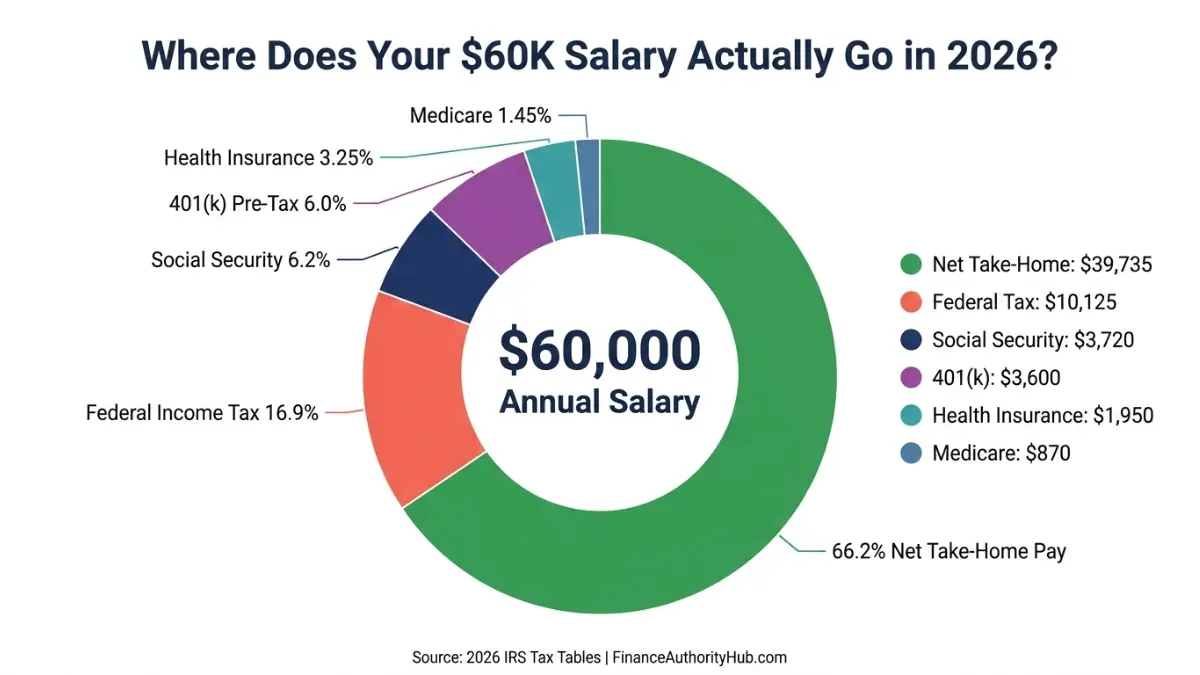

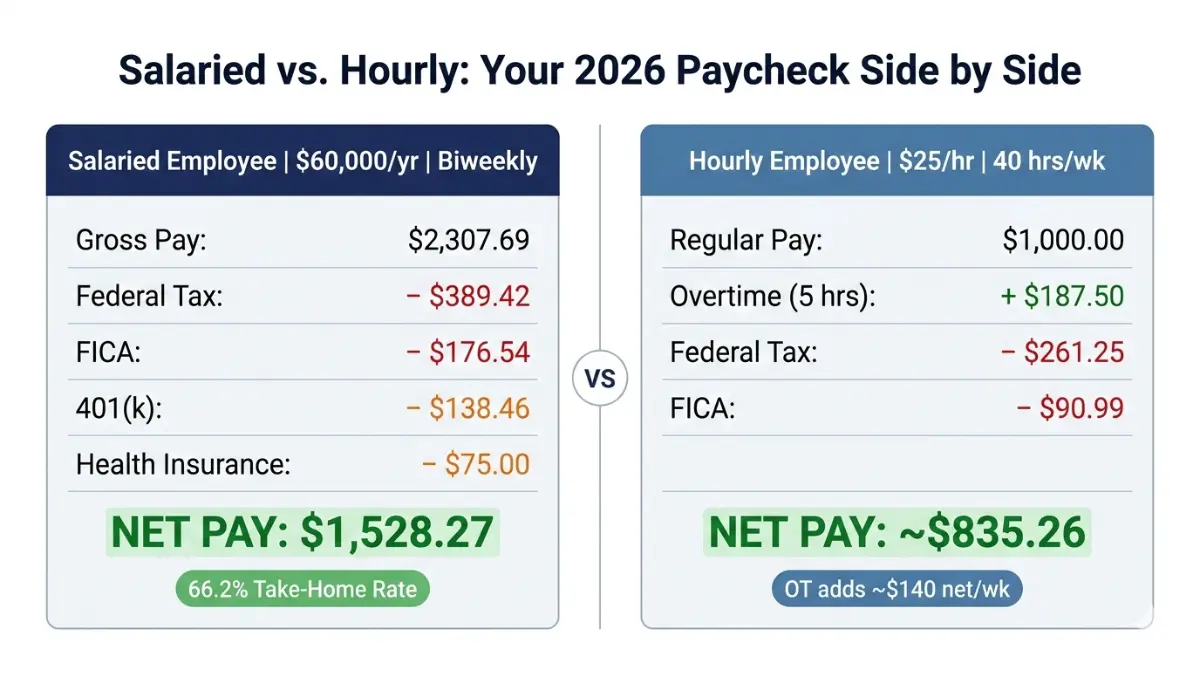

Example 1: Salaried Employee — $60,000/Year, Biweekly, Single Filer

| Line Item | Per Paycheck | Annual |

|---|---|---|

| Gross Pay | $2,307.69 | $60,000 |

| Federal Income Tax (22% effective) | $389.42 | $10,125 |

| Social Security (6.2%) | $143.08 | $3,720 |

| Medicare (1.45%) | $33.46 | $870 |

| 401(k) Pre-Tax (6%) | $138.46 | $3,600 |

| Health Insurance (est.) | $75.00 | $1,950 |

| Net Take-Home Pay | $1,528.27 | $39,735 |

| Effective Take-Home Rate | 66.2% | — |

This worker earns $60K but takes home $39,735 — a $20,265 gap. That’s not a mistake; it’s taxes plus smart pre-tax savings working together. To see how this net pay fits a mortgage, use our home affordability calculator to find what you can realistically buy.

Example 2: Hourly Worker — $25/Hour, 40 Hours/Week + Overtime

| Scenario | Hourly Rate | Weekly Hours | Weekly Gross |

|---|---|---|---|

| Regular Only | $25.00 | 40 hours | $1,000 |

| With 5 OT Hours | $25.00 + $37.50 OT | 45 hours | $1,187.50 |

Weekly net pay (regular, single, ~22% effective): ~$820 Weekly net pay (with overtime): ~$960

Important: Overtime is not taxed at a higher rate. It’s taxed identically to regular pay. The confusion arises because extra income may push you into the next bracket for that period. Our hourly to salary calculator converts any hourly rate to an annual equivalent instantly.

Example 3: Bonus Paycheck — Why It Feels Like You’re Taxed More

Bonuses are taxed at the 22% federal supplemental wage rate (flat), regardless of your actual bracket. A $5,000 bonus means $1,100 withheld for federal tax alone — before FICA.

Strategy: Ask payroll to spread your bonus across multiple paychecks to smooth the withholding. You don’t pay more tax overall; it just hits less in one shot.

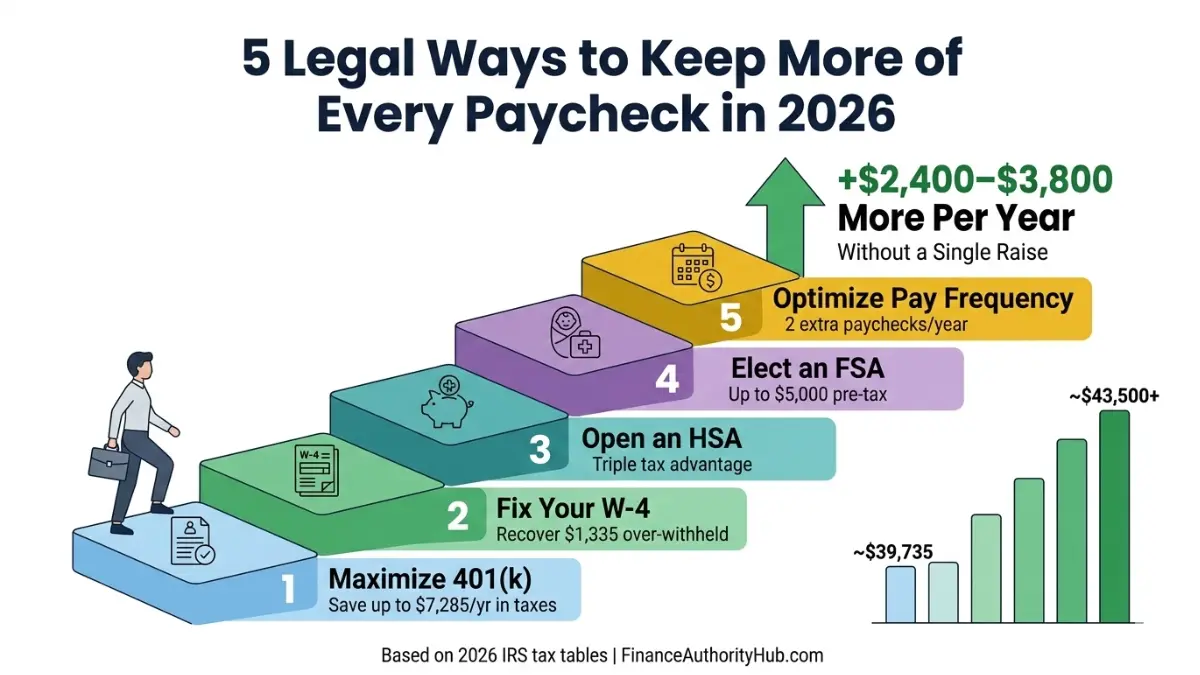

5 Proven Ways to Increase Your Real Net Pay in 2026

This is what no competitor calculator page shows you. Our expert panel identified these five moves as the highest-ROI actions available to US employees in 2026.

1. Maximize Your 401(k) Pre-Tax Contribution

Every $1,000 contributed pre-tax saves approximately $220 in federal tax (22% bracket) and up to $99 in state tax (California). A worker maxing $23,500 saves up to $7,285 in combined taxes. Use our 401(k) calculator to model your exact savings.

2. Fix Your W-4 Withholding

Most Americans over-withhold by an average of $1,335/year according to IRS data — giving the government an interest-free loan. Use the IRS W-4 withholding estimator to recalibrate. Correcting a W-4 can add $50–$120 per paycheck immediately.

3. Contribute to an HSA — The Triple Tax Advantage

HSA contributions are pre-tax going in, grow tax-free, and come out tax-free for medical expenses. A family contributing the $8,550 maximum saves $1,881 in federal taxes (22% bracket) annually. Read the full breakdown in our HSA tax strategy guide.

4. Elect FSA for Childcare or Medical Spending

A Dependent Care FSA lets you pay up to $5,000 in childcare pre-tax — saving $1,100+ for a 22% bracket earner. Medical FSA covers co-pays, glasses, dental, and prescriptions. The IRS FSA overview confirms 2026 contribution rules.

5. Model Pay Frequency to Optimize Cash Flow

Biweekly (26 paychecks) vs. semi-monthly (24 paychecks) creates two “extra paycheck” months per year for biweekly workers. Those months, your fixed expenses stay the same but income is higher — a natural savings opportunity. Pair this with our savings calculator to project the compounding effect.

What This Means For You: A $60,000 earner who correctly adjusts their W-4, contributes 6% to 401(k), and maxes their HSA individual contribution can increase effective annual net pay by $2,400–$3,800 without a single dollar of raise.

Once you know your real net pay, the next logical step is building a full financial picture. Our debt-to-income ratio calculator shows whether your take-home pay supports your current debt load — a critical number before any major financial decision.

Paycheck Calculator for UK, Canada & Australia: 2026 Key Differences

Our paycheck calculator supports 22 currencies and worldwide tax modeling. Here’s how to configure it for the three most-used non-US markets among our readers.

| Country | Key Deduction | 2026 Rate | How to Set in Calculator |

|---|---|---|---|

| 🇺🇸 USA | Social Security + Medicare (FICA) | 7.65% employee | Employee contribution %: 7.65% |

| 🇬🇧 UK | National Insurance (Class 1) | 8% on £12,570–£50,270 | Employee contrib: 8%; use progressive brackets for income tax |

| 🇨🇦 Canada | CPP + EI contributions | 5.95% CPP + 1.66% EI | Combined employee contrib: 7.61% |

| 🇦🇺 Australia | Medicare Levy + Income Tax | 2% Medicare levy | Add 2% to flat rate or progressive bracket total |

UK Workers: Use the HMRC income tax estimator to get your exact tax code breakdown, then enter those numbers into our progressive bracket mode.

Canadian Workers: The CRA Payroll Deductions Online Calculator gives province-specific rates — plug those directly into our tool.

Australian Workers: Enter your bracket rates from the ATO Tax Withheld Calculator into our progressive mode for AUD-accurate results.

Frequently Asked Questions about Paycheck Calculator

1. What is a paycheck calculator?

A paycheck calculator estimates your net take-home pay after federal taxes, FICA, state taxes, and deductions are subtracted from your gross salary or hourly wages.

2. How is net pay calculated?

Net pay = Gross Pay − Federal Income Tax − FICA (7.65%) − State Tax − Pre-Tax Deductions − Post-Tax Deductions.

3. What is the difference between gross pay and net pay?

Gross pay is what you earn before deductions. Net pay is what you actually receive. For most Americans, net pay is 62–72% of gross pay.

4. How much federal tax is taken from a paycheck in 2026?

It depends on your bracket. Most middle-income workers (single, $40K–$90K) see an effective federal rate of 12–22% after the standard deduction is applied.

5. What are FICA taxes on a paycheck?

FICA = Social Security (6.2%) + Medicare (1.45%) = 7.65% total, deducted automatically from every paycheck. Your employer matches the same amount.

6. What is the Social Security wage base in 2026?

The 2026 Social Security wage base is $184,500. Once your earnings exceed this, Social Security deductions stop for the rest of the year.

7. How do pre-tax deductions lower my taxes?

Pre-tax deductions like 401(k) contributions and health insurance premiums reduce your taxable income before any tax is calculated — lowering your federal, state, and sometimes FICA tax bills simultaneously.

8. How is overtime pay calculated on a paycheck?

Overtime is paid at 1.5× your regular rate for hours over 40 per week (federal FLSA standard). It’s taxed identically to regular wages — there is no special “overtime tax rate.”

9. Can I use this paycheck calculator for hourly workers?

Yes. Switch to hourly mode, enter your rate, regular hours per week, overtime hours, and overtime multiplier (default 1.5×). The calculator computes weekly, per-paycheck, and annual net pay.

10. Why was my bonus taxed more than my regular paycheck?

Bonuses use the supplemental wage rate of 22% federal flat withholding — regardless of your bracket. You don’t owe more tax overall; you’ll reconcile at filing. To reduce the sting, ask payroll to spread the bonus across paychecks.

11. What is the standard deduction in 2026?

The 2026 standard deduction is $16,100 for single filers and $32,200 for married filing jointly — increased from 2025 levels under the One Big Beautiful Bill. This directly lowers your federal taxable income before brackets are applied. See our full 2026 tax brackets guide for complete details.

Disclaimer: This paycheck calculator and the information in this article are for educational and informational purposes only. Results are estimates based on 2026 IRS tables and standard withholding assumptions. They do not constitute financial, tax, or legal advice, and may not reflect your exact paycheck due to employer-specific payroll configurations, local taxes, mid-year changes, or individual tax situations. Always verify your withholdings with a qualified CPA or tax professional and consult the IRS official tax resources for authoritative guidance.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.