Loan to Value Calculator: Know Your LTV Instantly

Loan-to-Value (LTV) Calculator

Compute LTV and CLTV, show equity, target planning (max loan / paydown / down payment), and a sensitivity table. You can choose “lower of purchase or appraisal” value basis (often used by lenders) and optionally use ARV for rehab analysis.

Inputs

If Auto-calc loan is ON, this field is computed automatically (Buying mode).

Results

LTV

—

Value used: —

CLTV

—

Total debt: —

Debt breakdown

First loan: —

Second loan: —

Equity

Equity: —

Equity %: —

Target planning

Target LTV: — • Max first loan @ target: — • Paydown needed: —

Target CLTV: — • Max total debt @ target: — • Total paydown needed: —

Step-by-step math

Sensitivity (how LTV/CLTV changes)

| Value change | Loan change | Value | First loan | LTV | CLTV |

|---|

Note: Many mortgage discussions reference 80% LTV as a common benchmark (context varies by country, lender, and product). [web:263]

Results appear after you click “Calculate.”

In This Article

What Is a Loan to Value Calculator — and Why Does Your LTV Number Matter in 2026?

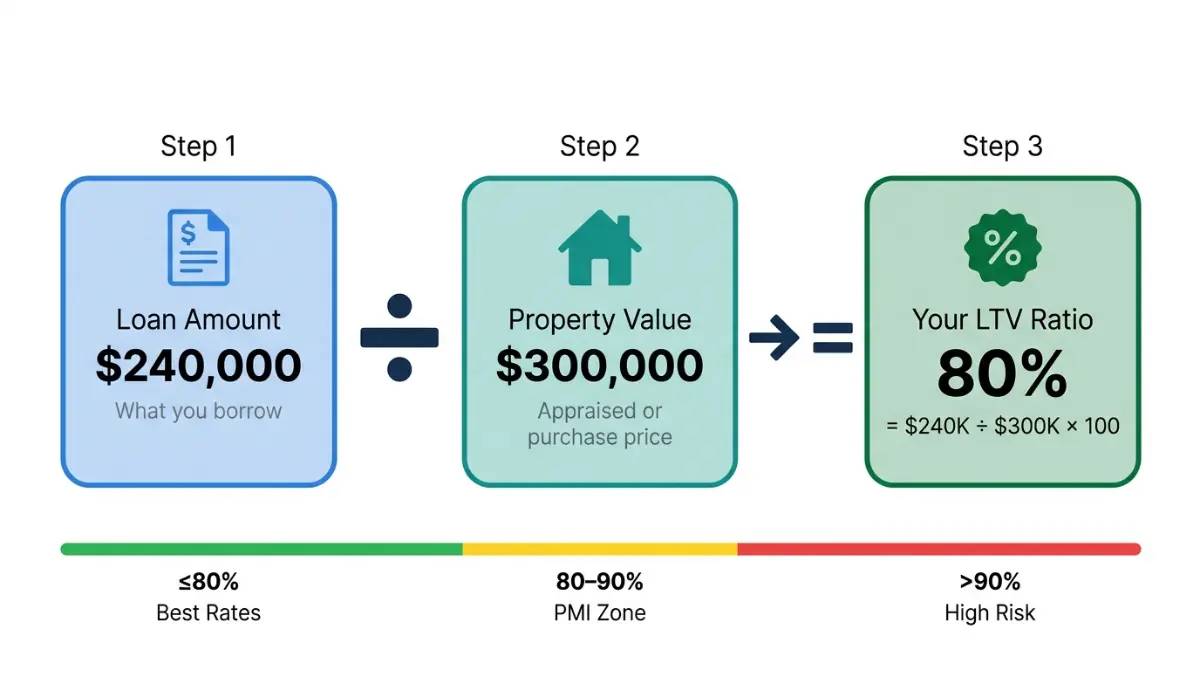

A loan to value calculator instantly tells you what percentage of your property’s value you’re borrowing. It divides your loan amount by the property’s appraised value and multiplies by 100. That single percentage — your LTV ratio — controls your mortgage approval, your interest rate, and whether you pay private mortgage insurance (PMI).

The core formula:

LTV = Loan Amount ÷ Property Value × 100

Real example: You’re buying a $300,000 home and borrowing $240,000. $240,000 ÷ $300,000 × 100 = 80% LTV

Why 2026 makes this more critical than ever: With 30-year mortgage rates still hovering above 6.5%, a difference of just 10 percentage points in your LTV can cost — or save — you $200–$350 per month. Before you set your home-buying budget, use our Mortgage Calculator to see exactly how your LTV affects your monthly payment.

💡 Key Takeaway: Your LTV ratio is the single most powerful number in your mortgage application. Every lender checks it before anything else.

How to Use This Loan to Value Ratio Calculator — Step by Step

Our loan to value ratio calculator goes far beyond what NerdWallet or Bankrate offer. Here’s how to get every number you need in under 60 seconds.

Buying a Home (Purchase Mode)

- Step 1: Select your currency and enter your purchase price

- Step 2: Enter the appraised value (our calculator automatically uses the lower of the two — exactly how lenders calculate LTV)

- Step 3: Enter your down payment amount or check “Auto-calc loan” to have the loan amount computed automatically

- Step 4: Hit Calculate — you instantly see your LTV %, CLTV %, equity amount, and how much paydown you need to hit your target LTV

Refinancing or Existing Mortgage (Refi Mode)

- Step 1: Enter your home’s current appraised or market value

- Step 2: Enter your remaining loan balance

- Step 3: Add any HELOC or second mortgage balance to calculate your combined LTV (CLTV)

ARV Mode — For Real Estate Investors

Toggle “Use After-Repair Value (ARV)” to calculate LTV based on a property’s projected post-renovation value. This is the standard method used by hard money lenders and fix-and-flip investors.

What our calculator shows you that competitors don’t:

- Your LTV and CLTV percentage simultaneously

- Exact dollar paydown needed to reach your target LTV (e.g., 80%)

- Down payment required to hit target LTV at purchase

- A sensitivity table showing how your LTV shifts as property values and loan amounts change

- Downloadable CSV export of all results

💡 What This Means For You: Most online LTV calculators show you one number. Ours shows you a complete financial picture — including your roadmap to 80% LTV.

Before running your numbers, check our Down Payment Calculator to model different down payment scenarios and their LTV impact.

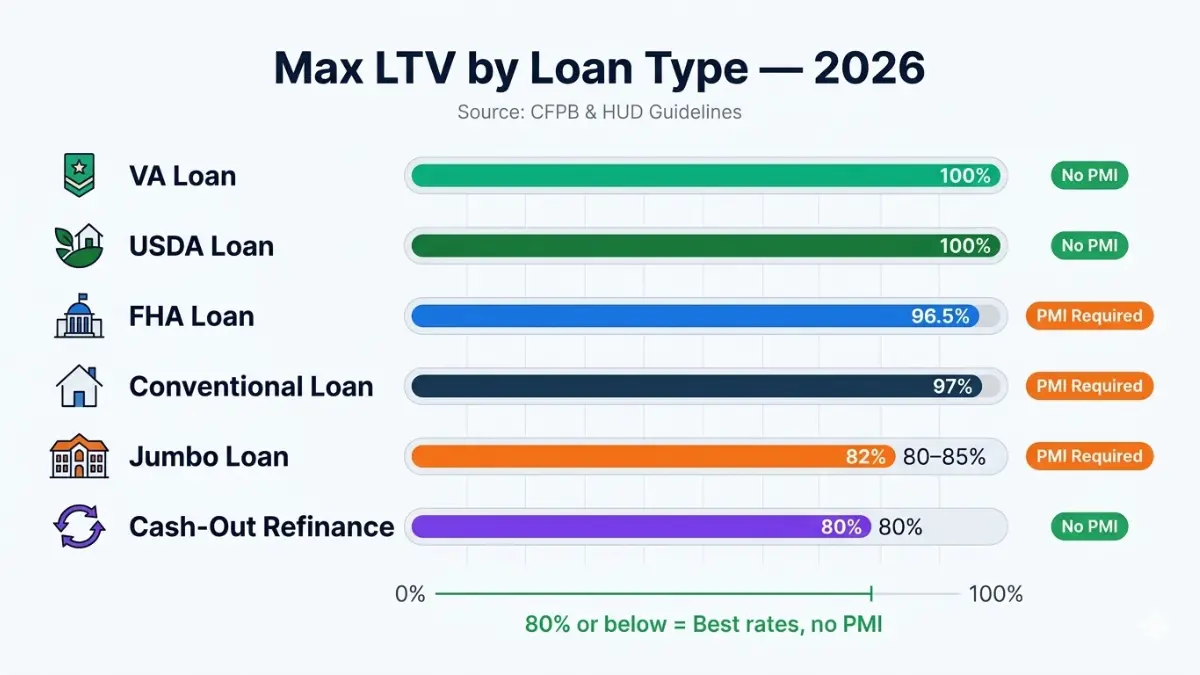

LTV Ratio Requirements by Loan Type — 2026 Lender Standards

This is the table no competitor publishes in one place. Every loan type has a different maximum LTV — and the differences are significant.

Master LTV Reference Table (2026)

| Loan Type | Max LTV | Min Down Payment | PMI Required? | Key 2026 Notes |

|---|---|---|---|---|

| Conventional | 97% | 3% | Yes (if LTV > 80%) | PMI removed at 80% LTV; conforming limit $766,550 |

| FHA Loan | 96.5% | 3.5% | Yes (MIP) | Credit score 580+ required for 96.5% LTV |

| VA Loan | 100% | 0% | No | Veterans/active military only; no PMI ever |

| USDA Loan | 100% | 0% | No | Rural properties only; income limits apply |

| Jumbo Loan | 80–85% | 15–20% | Varies by lender | Loan amounts above $766,550 (2026 limit) |

| Cash-Out Refinance | 80% | N/A | Varies | Maximum cash-out tied to 80% LTV cap |

| HELOC | 85% CLTV | N/A | No | Combined with first mortgage balance |

| Investment Property | 75–80% | 20–25% | No | Stricter limits; higher rates at same LTV |

Source: Consumer Financial Protection Bureau — Mortgage Key Terms

The 80% LTV Threshold — The Number That Saves You Thousands

80% LTV is the most important number in conventional mortgage lending. Cross above it, and you pay PMI. Stay at or below it, and you qualify for better rates with no insurance surcharge.

2026 real cost comparison on a $300,000 loan:

| LTV | Approx. Rate | Monthly P&I | Monthly PMI | Total Monthly Cost |

|---|---|---|---|---|

| 97% LTV (3% down) | ~7.10% | $2,011 | ~$125–$200 | ~$2,136–$2,211 |

| 90% LTV (10% down) | ~6.85% | $1,968 | ~$75–$125 | ~$2,043–$2,093 |

| 80% LTV (20% down) | ~6.50% | $1,896 | $0 | $1,896 |

Dropping from 97% to 80% LTV saves approximately $240–$315/month — that’s $2,880–$3,780 per year, or up to $113,400 over a 30-year mortgage.

Use our Home Affordability Calculator to find your price range based on the down payment that gets you to 80% LTV.

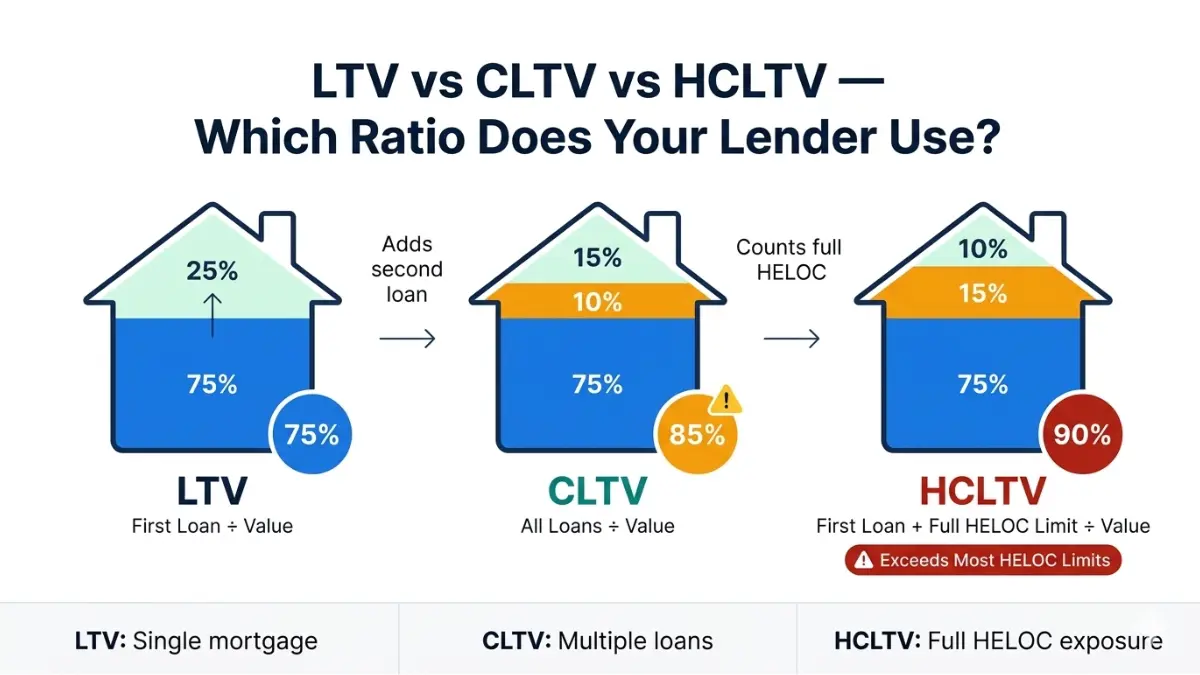

LTV vs. CLTV vs. HCLTV — What’s the Difference and Which One Does Your Lender Use?

Most homeowners track only their LTV. But lenders use three different ratios depending on your situation — and confusing them could derail a HELOC application or a refinance.

LTV (Loan to Value)

What it measures: Your first mortgage only, against property value. When lenders use it: All purchase mortgages, single-loan refinances. Formula: First Loan ÷ Property Value × 100

CLTV (Combined Loan to Value)

What it measures: All secured loans combined — first mortgage + HELOC + second mortgage. When lenders use it: Any application where a second lien exists on the property. Formula: (First Loan + Second Loan) ÷ Property Value × 100

HCLTV (High Combined Loan to Value)

What it measures: First mortgage + the full credit limit of your HELOC, not just what you’ve drawn. When lenders use it: HELOC applications specifically — even undrawn HELOC balance counts. Formula: (First Loan + Full HELOC Limit) ÷ Property Value × 100

Side-by-Side Comparison

| Metric | Formula | Includes Undrawn HELOC? | When It Applies |

|---|---|---|---|

| LTV | First loan ÷ value | No | All purchase mortgages |

| CLTV | All loans ÷ value | Drawn amount only | Second mortgage or HELOC exists |

| HCLTV | First loan + full HELOC limit ÷ value | Yes — full limit | HELOC applications |

Real example that shows why this matters:

You have a $400,000 home with a $300,000 first mortgage and a $60,000 HELOC with $40,000 drawn.

- LTV = $300,000 ÷ $400,000 = 75% ✅

- CLTV = ($300,000 + $40,000) ÷ $400,000 = 85% ⚠️

- HCLTV = ($300,000 + $60,000) ÷ $400,000 = 90% ❌ (exceeds most HELOC limits)

💡 Key Takeaway: Your LTV looks excellent at 75% — but your HCLTV is 90%, which many lenders will decline. Always calculate all three before applying for a HELOC. Fannie Mae’s CLTV guidelines set the standard most lenders follow.

If you’re carrying significant debt across multiple obligations, our Debt-to-Income Ratio Calculator helps you model lender approval odds alongside your CLTV.

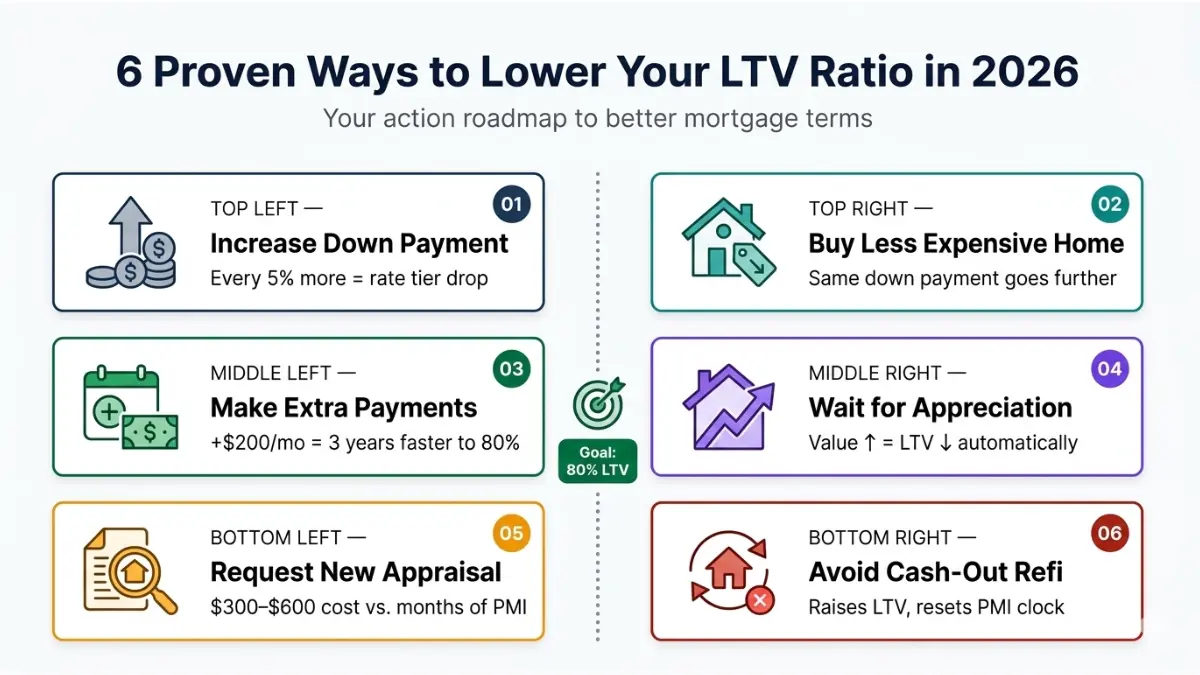

How to Lower Your Loan to Value Ratio — 6 Proven Strategies for 2026

A high LTV isn’t permanent. These six strategies give you a concrete action plan to reduce your loan to value ratio and unlock better mortgage terms.

Strategy 1 — Increase Your Down Payment Before Purchase

This is the most direct lever. Every additional 5% down on a $300,000 home reduces your loan by $15,000 and drops your LTV by 5 percentage points.

- Going from 10% to 20% down eliminates PMI entirely

- Going from 5% to 10% down typically drops your rate by 0.15–0.25%

- Use our Down Payment Calculator to find your exact target savings amount

Strategy 2 — Choose a Less Expensive Property

A $50,000 down payment on a $250,000 home gives you 80% LTV. The same $50,000 on a $350,000 home gives you only 85.7% LTV — you still pay PMI.

Buying slightly below your maximum budget can eliminate PMI entirely — a decision worth thousands annually.

Strategy 3 — Make Extra Principal Payments

Adding $200/month to a $240,000 mortgage at 6.5% over 30 years:

- Reduces your loan term by approximately 4.5 years

- Drops you below 80% LTV roughly 3 years faster

- Saves approximately $38,000–$45,000 in total interest

Use our Amortization Calculator to model exactly how extra payments accelerate your LTV reduction.

Strategy 4 — Wait for Property Appreciation

If your home value rises from $300,000 to $340,000 while your loan stays at $240,000:

- Your LTV drops from 80% to 70.6% without a single extra payment

- You may qualify to remove PMI through a formal re-appraisal request

In 2026, national median home values remain elevated. Check current property value trends via the Federal Housing Finance Agency House Price Index before requesting a new appraisal.

Strategy 5 — Request a New Appraisal

If your area has appreciated since purchase, a formal appraisal will reset your LTV calculation using the current market value.

- PMI removal: Lenders are required under the Homeowners Protection Act to cancel PMI when LTV reaches 78% based on original value — but you can request removal at 80% with a new appraisal showing higher value

- Cost of appraisal: typically $300–$600 — often paid back in one month of eliminated PMI

Strategy 6 — Avoid Unnecessary Cash-Out Refinancing

Cash-out refinancing increases your loan balance, raises your LTV, and can reset your PMI clock. Before pursuing this option, use our Mortgage Refinance Calculator to model the full cost impact — including how your LTV changes post-refi.

💡 What This Means For You: Our calculator’s Target LTV planning feature shows you the exact dollar amount you need to pay down to hit 80% LTV — updated in real time as you adjust inputs. No competitor’s calculator does this.

LTV Standards Across the USA, UK, Canada, and Australia — What Lenders Expect in 2026

The loan to value calculator concept is universal — but LTV benchmarks, insurance requirements, and terminology differ by country. Here’s what Tier 1 market lenders expect right now.

United States

- 80% LTV: The gold standard for conventional loans — no PMI, best rates

- Conforming loan limit (2026): $766,550 for single-family homes in most areas

- VA and USDA loans: 100% LTV available with no PMI — exclusively for eligible veterans and rural borrowers

- FHA loans: 96.5% LTV permitted — most accessible for first-time buyers with lower credit scores

- Full guidelines available via HUD’s official FHA resource center

United Kingdom

- LTV terminology is identical; lenders use the same formula

- 90–95% LTV mortgages are widely available through high street banks

- The UK government’s Mortgage Guarantee Scheme supports 95% LTV purchases for qualifying buyers

- 85% LTV typically accesses the best fixed-rate deals from major lenders

- Higher LTVs (90–95%) carry significantly higher rates in 2026 given Bank of England base rate environment

Canada

- Canada Mortgage and Housing Corporation (CMHC) mortgage insurance is mandatory for any purchase with LTV above 80%

- Maximum insured purchase price increased to $1.5 million in late 2024, still applicable in 2026

- CMHC insurance premium ranges from 0.6% to 4.0% of the loan amount depending on LTV tier

- First-time buyer incentive programs available through CMHC’s official portal

Australia

- LVR (Loan to Value Ratio) is the standard term used by Australian lenders

- Lenders Mortgage Insurance (LMI) is triggered when LVR exceeds 80% — typically costing $15,000–$25,000 on an $800,000 property

- The First Home Guarantee scheme allows eligible buyers to purchase with as little as 5% deposit without paying LMI

- Most major banks (Commonwealth, Westpac, ANZ, NAB) apply LMI above 80% LVR

Expert Insight — Laura M. Bennett, CFP®, FinanceAuthorityHub.com:

“In 2026, with mortgage rates still elevated, the difference between a 90% and 80% LTV isn’t just an insurance line item — it’s often $250–$350 per month in combined rate and PMI costs. Homebuyers who understand their LTV before they start shopping have a genuine negotiating and financial advantage over those who don’t.”

Expert Insight — Daniel Moreau, CPA/CFP, FinanceAuthorityHub.com:

“The smartest first-time buyers I counsel run an LTV calculation before they even set a price range. It tells you exactly what down payment you need — and exposes how much PMI will cost if you fall short. Knowledge here translates directly to money saved.”

If you’re planning your broader home purchase finances, our Closing Cost Calculator and Mortgage Pre-Approval guide are your next essential resources.

Frequently Asked Questions — Loan to Value Calculator

1. What is a loan to value calculator?

A loan to value calculator computes the percentage of a property’s value you’re financing through a loan. Enter your loan amount and property value, and it instantly shows your LTV ratio — the key metric lenders use to determine rates, PMI requirements, and loan approval.

2. What is a good LTV ratio?

80% or below is considered a good LTV ratio by most U.S. lenders. It eliminates PMI on conventional loans and qualifies you for the most competitive mortgage rates. Below 70% is excellent and may unlock premium rate tiers.

3. How do I calculate LTV manually?

Divide your loan amount by the property’s appraised value, then multiply by 100. Example: $240,000 loan ÷ $300,000 property value × 100 = 80% LTV. Lenders use the lower of purchase price or appraised value.

4. What LTV is needed to avoid PMI?

80% or below on a conventional loan. Once your LTV naturally drops to 78% based on your original amortization schedule, lenders are legally required to cancel PMI automatically under the Homeowners Protection Act.

5. What is the difference between LTV and CLTV?

LTV measures only your first mortgage against property value. CLTV (Combined Loan to Value) includes all secured loans — your first mortgage plus any HELOC or second mortgage. Lenders always check CLTV when you have multiple loans on a property.

6. What LTV is needed to refinance?

Most lenders require 80% LTV or below for a standard rate-and-term refinance to get the best terms. Cash-out refinances are typically capped at 80% LTV. FHA streamline refinances may allow higher LTVs with different qualification criteria.

7. Can I get a mortgage with 90% LTV?

Yes. FHA loans allow up to 96.5% LTV; conventional loans allow up to 97%. VA and USDA loans permit 100% LTV. Higher LTVs require PMI or government mortgage insurance, and typically carry higher interest rates.

8. Does a higher property value lower my LTV?

Yes — automatically. If your home appreciates from $300,000 to $350,000 while your loan balance stays at $240,000, your LTV drops from 80% to 68.6%. You can request a formal appraisal to capture this improvement for PMI removal.

9. How does LTV affect my mortgage interest rate?

Higher LTV signals greater lender risk, which results in higher interest rates. In 2026, dropping from 90% to 80% LTV on a $300,000 loan can reduce your rate by 0.25–0.50%, saving approximately $150–$300 per month.

10. What is ARV in LTV calculations?

ARV (After-Repair Value) is used by real estate investors to calculate LTV based on a property’s projected value after renovations — rather than its current condition value. Hard money lenders typically cap LTV at 75% of ARV for fix-and-flip projects.

11. How often should I recalculate my LTV?

At minimum, annually — and immediately before any refinance application, HELOC request, or PMI removal attempt. Property values and loan balances both change continuously. Use our loan to value calculator any time market conditions shift or you make extra principal payments.

Disclaimer

This loan to value calculator and all accompanying content on FinanceAuthorityHub.com are provided for educational and informational purposes only. Results are mathematical estimates and do not constitute financial advice, mortgage approval, a commitment to lend, or a guarantee of loan terms. LTV requirements, PMI thresholds, and loan limits vary by lender, loan type, credit profile, and jurisdiction. Mortgage rates and lending standards are subject to change. Always consult a licensed mortgage professional or qualified financial advisor before making borrowing or real estate decisions. FinanceAuthorityHub.com is not a lender, broker, or financial institution.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.