Property Tax Calculator – Instant 2026 Estimate

Property Tax Calculator

Calculate property tax using assessed/taxable value and either a percent tax rate or a mill rate, then project future taxes, estimate escrow amounts, and export a detailed CSV.

Inputs

Mill rate methods often use: (mill rate × taxable value) ÷ 1,000. [web:179][web:183]

Escrow collections are often estimated as 1/12 of annual taxes each month (plus a cushion depending on the lender). [web:191]

Results

Year 1 total property tax

—

Monthly: — • Per payment: —

Values used (Year 1)

Market: —

Assessed: —

Taxable: —

Rate details (Year 1)

Rate %: —

Equivalent mills: —

Effective on market: —

Breakdown (Year 1)

Base tax: —

Levies: —

Effective on assessed: —

Escrow estimate (optional)

Monthly escrow: — • Cushion: —

Projection highlights

Total taxes over horizon: —

End-year annual tax: — • End-year market value: —

Year-by-year projection

| Year | Market value | Assessed value | Exemption | Taxable value | Rate % | Base tax | Levies | Annual tax | Monthly |

|---|

Market value scenarios (Year 1)

| Scenario | Market value | Assessed value | Taxable value | Annual tax |

|---|

Results appear after you click “Calculate.”

In This Article

Your property tax = assessed value × local tax rate, minus any exemptions. Use the calculator above to get your instant 2026 estimate — including annual tax, monthly cost, escrow breakdown, and a 10-year projection — in under 60 seconds.

What this tool calculates for you:

- Annual and monthly property tax payments

- Taxable value after exemptions

- Mill rate equivalent

- Escrow cushion estimate

- Year-by-year tax projection (up to 60 years)

- Downloadable CSV for your records

Who needs this right now: First-time homebuyers budgeting for a new home, current homeowners who just received a reassessment notice, and real estate investors running ROI calculations.

Property taxes in America have risen 18% over the past five years, according to Construction Coverage’s 2026 analysis. If you haven’t checked your assessed value recently, you may already be overpaying. Use our mortgage calculator alongside this tool to see your complete monthly housing cost.

How to Calculate Property Tax in 2026

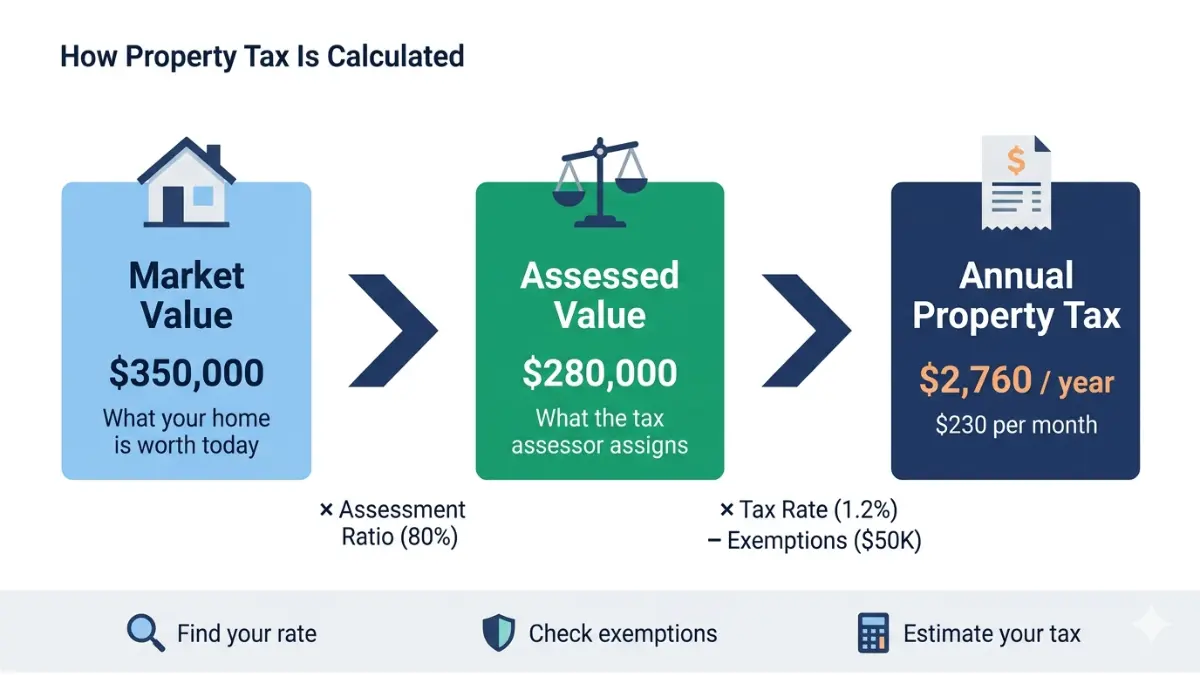

Understanding how your property tax bill is calculated puts you in control. The process uses three numbers: your property’s value, your local tax rate, and any exemptions you qualify for.

The Core Property Tax Formula

Annual Property Tax = Assessed Value × Tax Rate

Monthly Property Tax = Annual Tax ÷ 12

Here is how those three key values differ:

| Term | What It Means | Example ($350,000 Home) |

|---|---|---|

| Market Value | What your home would sell for today | $350,000 |

| Assessed Value | What your tax assessor assigns (often 80–100% of market) | $280,000 (80% ratio) |

| Taxable Value | Assessed value minus any exemptions | $230,000 (after $50K homestead) |

Real example: A $350,000 home with an 80% assessment ratio, a $50,000 homestead exemption, and a 1.2% tax rate produces an annual property tax of $2,760 — or $230/month.

How to Use This Property Tax Calculator — Step by Step

- Enter your home’s market value (use a recent appraisal or Zillow estimate)

- Select your currency (USD, GBP, CAD, AUD, and 18 others supported)

- Choose your assessment method — ratio (e.g., 80%) or direct assessed value

- Add any exemptions — homestead, senior, veteran, or disability amount

- Enter your tax rate — as a percentage, mill rate, or known annual amount

- Set your projection horizon — see how your taxes grow over 10, 20, or 30 years

What Is a Mill Rate? (Most Calculators Skip This)

A mill rate is an alternative way localities express the property tax rate. One mill equals $1 of tax per $1,000 of assessed value.

Conversion formula: Mill Rate ÷ 10 = Tax Rate Percentage

Example: A mill rate of 24 on a $280,000 assessed value = $6,720/year in property taxes.

Many counties — especially in the Northeast — publish mill rates instead of percentages. This calculator accepts both formats so you never have to convert manually.

What Is Escrow for Property Taxes?

When you have a mortgage, your lender typically collects property taxes monthly through an escrow account — usually one-twelfth of your annual bill, plus a 1–2 month cushion.

According to IRS Publication 530, property taxes paid through escrow are deductible only in the year your lender actually disburses the funds to the tax authority — not when you deposit money into escrow.

Use our home affordability calculator to see how your escrow payment affects your total monthly housing budget.

Property Tax Rates by State in 2026 — Full Data Table

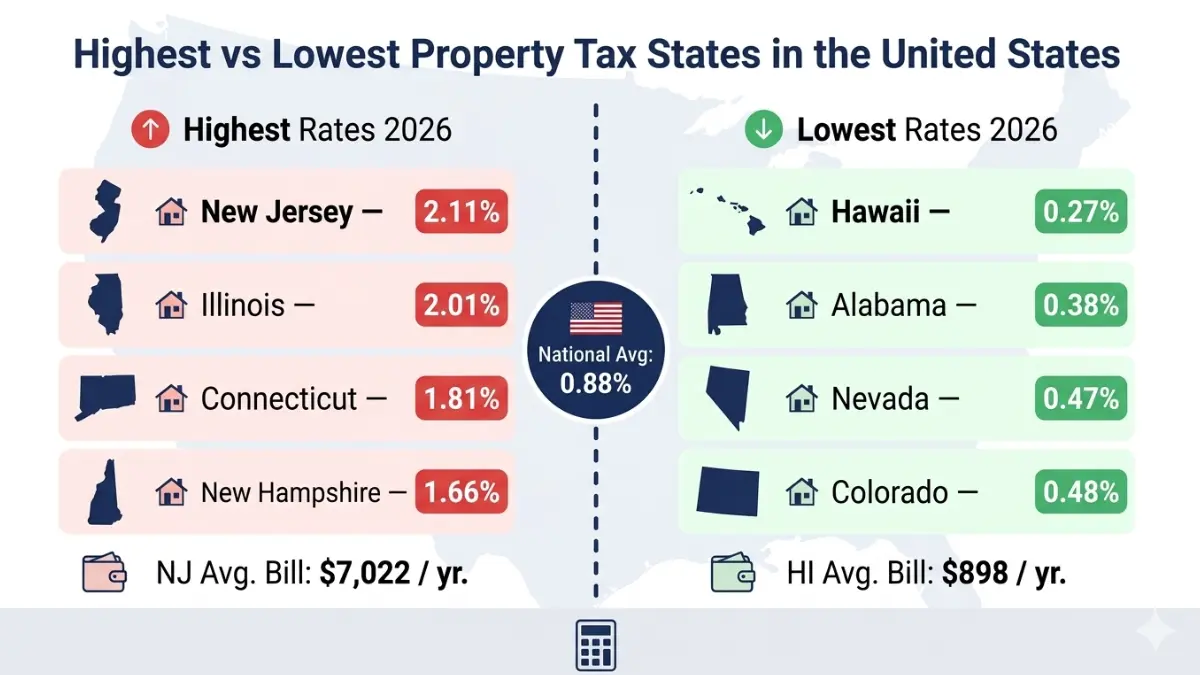

Property tax rates vary dramatically across the U.S. According to Tax Foundation data, property taxes are the single largest source of state and local revenue, funding schools, roads, fire departments, and emergency services nationwide.

The national average effective property tax rate in 2026 is 0.88% — but your actual rate could be anywhere from 0.27% to over 2%.

2026 State Property Tax Rates — Highest to Lowest (Key States)

| State | Effective Rate | Annual Tax on $332,700 Home | Rank |

|---|---|---|---|

| New Jersey | 2.11% | $7,022 | #1 Highest |

| Illinois | 2.01% | $6,694 | #2 |

| Connecticut | 1.81% | $6,024 | #3 |

| New Hampshire | 1.66% | $5,511 | #4 |

| Vermont | 1.59% | $5,291 | #5 |

| Texas | 1.58% | $5,257 | #6 |

| Wisconsin | 1.51% | $5,021 | #7 |

| Nebraska | 1.48% | $4,924 | #8 |

| National Average | 0.88% | $2,928 | — |

| Colorado | 0.48% | $1,597 | #47 |

| South Carolina | 0.48% | $1,597 | #47 |

| Alabama | 0.38% | $1,265 | #49 |

| Hawaii | 0.27% | $898 | #50 Lowest |

Data: PropertyShark 2026, WalletHub 2026, Tax Foundation 2025

Why Do Property Tax Rates Vary So Much?

Three core reasons drive the massive spread between states:

- School funding reliance — States like New Jersey fund nearly all public education through local property taxes, driving rates above 2%

- Assessment lag — Many states reassess properties every 3–5 years, creating gaps between rising home values and taxable values

- Local budget needs — Cities, counties, school districts, and fire districts all levy separate rates that stack on top of each other

Key insight from the Tax Foundation: Property values surged nearly 27% faster than inflation since 2020, yet effective tax rates have slightly declined because assessments haven’t fully caught up. Many homeowners will see their bills rise sharply at their next reassessment cycle.

Use our mortgage refinance calculator if you’re considering moving to a lower-tax state — the monthly savings can be substantial.

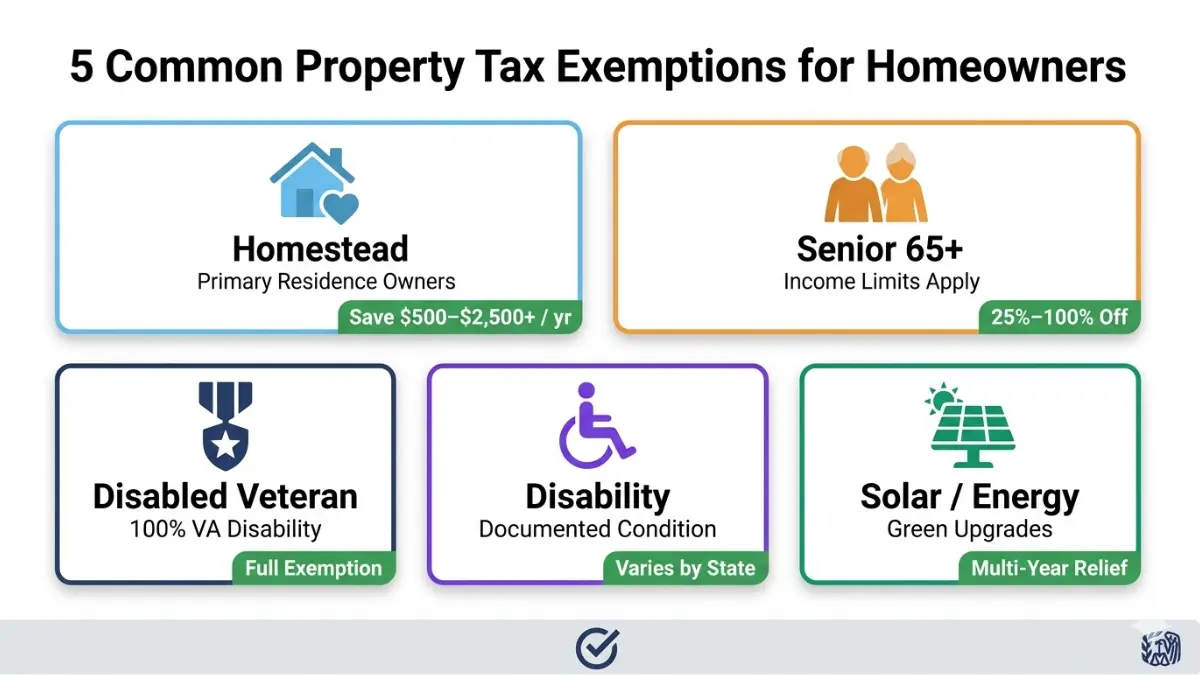

Property Tax Exemptions That Can Lower Your 2026 Bill

Most homeowners leave money on the table simply because they don’t know what exemptions they qualify for. Many exemptions are not automatic — you must actively apply for them.

5 Key Property Tax Exemptions in 2026

| Exemption | Who Qualifies | Typical Annual Savings |

|---|---|---|

| Homestead | Primary residence owners | $500 – $2,500+ |

| Senior Citizen | Age 65+, with income limits | 25% – 100% reduction |

| Disabled Veteran | Veterans with 100% VA disability rating | Full exemption in many states |

| Disability | Documented permanent disability | Varies by state |

| Solar / Energy | Solar panels, green upgrades | Partial to full exemption |

How to Apply for a Homestead Exemption (3 Steps)

- Confirm you qualify — the property must be your primary residence as of January 1 of the tax year

- Contact your county assessor’s office (most accept online applications now)

- Submit proof of residency — driver’s license, utility bill, or voter registration

Most states require annual renewal, while others grant it permanently once approved. Missing the deadline — often March or April — means you forfeit savings for the entire year.

What Competitors Miss: Most Homeowners Don’t Apply

According to the National Taxpayers Union Foundation, only 5% of homeowners ever challenge or appeal their property tax assessments — even though appeal success rates run between 40% and 60% in many ZIP codes.

Additionally, many eligible homeowners never file for senior or veteran exemptions because they assume it happens automatically. It does not.

“Proactive exemption filing is one of the highest-return financial moves a homeowner can make,” says Laura M. Bennett, CFP, Senior Financial Advisor at FinanceAuthorityHub.com. “A single homestead exemption application can save a family $1,000+ per year — every year — for as long as they own the home.”

If your financial situation has changed recently, pair this with our debt-to-income ratio calculator to see how property tax savings affect your overall debt picture.

How to Lower Your Property Tax Bill in 2026

Property taxes rose an average of 18% nationally over five years. Here’s how to fight back — legally.

5 Ways to Reduce Your Property Tax Without Filing a Formal Appeal

- Check for unclaimed exemptions — homestead, senior, veteran, disability; most need an active application

- Review your property record card — errors in square footage, bedroom count, or lot size inflate your bill; request a correction at your county assessor’s office

- Check your property classification — incorrectly labeled as commercial or multi-family properties pay higher rates; file a classification review

- Claim energy/solar credits — many states offer multi-year tax reductions for qualifying upgrades

- Apply for income-based deferral programs — qualifying low-income homeowners can defer taxes until the property sells

How to File a Property Tax Appeal — Step by Step

⚠️ Critical Warning: Most appeal deadlines fall between January and March. Act immediately if you received your 2026 assessment notice.

- Get your assessment notice — check it carefully for your property’s listed square footage, bedroom count, and lot size

- Compare comparable sales (“comps”) — find 3–5 similar homes in your neighborhood that sold recently for less than your assessed value; your county assessor’s website lists these

- File your appeal form — most counties accept online submissions; look for “informal review” or “assessment appeal” on your county assessor’s website

- Attend your hearing — present your comp data clearly; hearings are typically 10–15 minutes

- Receive your result — if successful, your assessed value drops and your bill decreases, sometimes retroactively

What Happens If You Win Your Appeal

- Your assessed value is reduced and your annual tax bill drops

- Some jurisdictions apply the reduction retroactively — you may receive a refund or tax credit

- The lower assessment typically holds until your next full reassessment cycle (1–5 years)

What Happens If You Lose

- Your assessment stays the same — no penalty for filing

- You can escalate to a state Board of Assessment Appeals or Tax Court

- For properties over $1 million, hiring a property tax consultant (who typically charges 30–50% of first-year savings on contingency) is often worth it

“Taxpayers shouldn’t be afraid to appeal,” says Daniel Moreau, CPA/CFP, at FinanceAuthorityHub.com. “The worst case is the status quo. The best case is hundreds or thousands of dollars in annual savings — and those savings compound for years.”

For broader financial planning, use our retirement calculator to see how reducing recurring expenses like property taxes accelerates your long-term savings.

Frequently Asked Questions About Property Tax Calculator

1. How does a property tax calculator work?

It multiplies your home’s assessed value by your local tax rate, then subtracts any exemptions to produce your annual and monthly tax estimate. Our tool also supports mill rate inputs and generates multi-year projections.

2. What is the difference between assessed value and market value?

Market value is what your home would sell for today. Assessed value is what your local tax assessor assigns for tax purposes — typically 60–100% of market value depending on your state’s assessment ratio.

3. How is a mill rate different from a tax rate percentage?

A mill rate is expressed as dollars per $1,000 of assessed value. Divide any mill rate by 10 to get the equivalent tax rate percentage. For example, 15 mills = 1.5%.

4. What is the average property tax in the U.S. in 2026?

The average U.S. household pays approximately $3,119 per year in real estate property taxes, according to the U.S. Census Bureau. The national average effective rate is 0.88% of home value.

5. Which state has the highest property taxes in 2026?

New Jersey has the highest effective property tax rate at 2.11%, according to PropertyShark’s 2026 state rankings. The median New Jersey homeowner pays over $9,500 per year.

6. Which state has the lowest property taxes in 2026?

Hawaii has the lowest effective rate at 0.27%, though actual tax bills can still be high due to Hawaii’s elevated home values.

7. How do I calculate my property tax manually?

Multiply your assessed value by your local tax rate percentage. For example: $250,000 assessed value × 1.2% = $3,000/year. Subtract any applicable exemption amounts from the assessed value first.

8. Can I lower my property tax bill legally?

Yes. File for all eligible exemptions (homestead, senior, veteran), review your property record card for errors, and file a formal appeal if comparables suggest you are over-assessed. Success rates on appeals run 40–60% in many areas.

9. What is a homestead exemption and how do I get it?

A homestead exemption reduces your home’s taxable value because it is your primary residence. You must apply at your county assessor’s office — it is not automatic. Deadlines typically fall in spring. Savings range from $500 to $2,500+ per year depending on your state.

10. Are property taxes included in a mortgage payment?

Yes, for most mortgage holders. Lenders collect roughly one-twelfth of your annual property tax each month through an escrow account and pay it directly to your local government. The IRS confirms you can only deduct the amount actually paid to the tax authority — not your monthly escrow deposits.

11. How often are properties reassessed for tax purposes?

It varies widely by state. Some states reassess annually, others every 3–5 years. California’s Proposition 13 reassesses only when a property changes hands. Understanding your state’s reassessment schedule helps you anticipate future tax increases and time an appeal correctly.

Related Tools & Guides

Planning your full homeownership cost? These tools work alongside your property tax estimate:

- Mortgage Calculator — full monthly payment including principal and interest

- Closing Cost Calculator — upfront costs when buying a home

- Down Payment Calculator — how much to save before buying

- Capital Gains Tax Calculator — taxes owed when selling your property

- 2026 Tax Brackets Guide — how property tax deductions interact with your income tax

⚠️ Disclaimer: This property tax calculator and the content on this page are for educational and informational purposes only. All results are estimates based on inputs you provide and do not constitute financial, tax, or legal advice. Property tax laws, rates, and exemption rules vary significantly by state, county, and municipality and are subject to change. Consult a licensed CPA, tax professional, or your local county assessor’s office for advice specific to your situation. FinanceAuthorityHub.com is not responsible for decisions made based on calculator outputs.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.