Roth IRA Calculator 2026: See Your Tax-Free Growth

Roth IRA Calculator

Project Roth IRA growth with detailed year-by-year results, inflation-adjusted balances, scenario comparison, and an optional USD-based IRS contribution & income (MAGI) check.

Inputs

IRS limits/MAGI eligibility are USD-only. Use USD if you want the eligibility checker.

If you plan to raise contributions over time (raises/inflation), enter a %.

If entered, the tool caps annual contributions at this amount (simple estimate).

If you’re not using USD, turn off eligibility or switch currency to USD.

Results

Retirement projection

Current age: — → Retirement age: —

Horizon (years): —

Contribution check

Planned annual contribution: —

Used annual contribution (after caps): —

Eligibility status: —

Ending balance

Nominal (future): —

Inflation-adjusted (today’s $): —

Totals

Total contributions: —

Total growth: —

Income estimate (simple)

Monthly income (4% rule): —

Monthly income (today’s $): —

IRS limits shown (USD)

Under 50: —

Age 50+: —

Year-by-year schedule

| Year | Age | Contribution | Cumulative contrib | Start balance | Growth | End balance | End balance (today’s $) |

|---|

Return scenarios (ending balances)

| Return % | Ending balance | Ending balance (today’s $) | Monthly income (4%) |

|---|

Results appear after you click “Calculate.”

In This Article

A Roth IRA is one of the most powerful tax-free retirement tools available to Americans today. For 2026, the IRS increased the contribution limit to $7,500 (or $8,600 for those age 50+), giving you more room to build tax-free wealth.

Use the Roth IRA calculator above to instantly project your retirement balance, see your tax-free growth, and check your 2026 eligibility — all in under 60 seconds.

2026 Roth IRA Snapshot:

- ✅ Contribution limit: $7,500 (under age 50) | $8,600 (age 50+)

- ✅ Income limit (single): Full contribution below $153,000 MAGI

- ✅ Income limit (married jointly): Full contribution below $242,000 MAGI

- ✅ Contribution deadline: April 15, 2027

- ✅ Tax on withdrawals in retirement: $0

2026 Roth IRA Contribution Limits: What the IRS Just Changed

How Much Can You Contribute to a Roth IRA in 2026?

The IRS officially raised the IRA contribution limit to $7,500 for 2026, up from $7,000 in 2025. This $500 increase applies to both Traditional and Roth IRAs combined — you cannot contribute $7,500 to each separately.

For those aged 50 and older, the catch-up contribution also increased for the first time under SECURE 2.0, rising from $1,000 to $1,100. You can verify the official figures directly on the IRS 2026 retirement limits announcement.

| Age Group | 2025 Limit | 2026 Limit | Increase |

|---|---|---|---|

| Under 50 | $7,000 | $7,500 | +$500 |

| Age 50+ (catch-up) | $8,000 | $8,600 | +$600 |

| Ages 60–63 (SECURE 2.0 super catch-up) | $11,250 | $11,250 | Unchanged |

Key rule: You can contribute up to these limits only if you have earned income at least equal to your contribution. Investment income, rental income, and Social Security do not count as earned income for IRA purposes. For the full earned income rules, see the official IRS IRA contribution limits guide.

2026 Roth IRA Income Phase-Out Ranges: Are You Still Eligible?

Your ability to contribute to a Roth IRA depends on your Modified Adjusted Gross Income (MAGI). The IRS increased phase-out thresholds for 2026 across all filing statuses.

| Filing Status | Full Contribution | Phase-Out Range | No Contribution |

|---|---|---|---|

| Single / Head of Household | MAGI < $153,000 | $153K – $168K | Above $168K |

| Married Filing Jointly | MAGI < $242,000 | $242K – $252K | Above $252K |

| Married Filing Separately | MAGI < $0 | $0 – $10K | Above $10K |

If your income falls inside the phase-out range, you can still make a partial contribution. The calculation reduces your limit proportionally for every dollar above the lower threshold. Earners above the upper limit cannot contribute directly — but see the Backdoor Roth strategy in Section 5 below.

SECURE 2.0 Roth Catch-Up Mandate: New in 2026

Starting January 1, 2026, workers aged 50+ who earned more than $150,000 in wages in the prior year must make catch-up contributions as Roth (after-tax) in their 401(k). Pre-tax catch-up contributions are no longer allowed for these higher earners. This is a major SECURE 2.0 change that zero top competitors have explained properly — plan accordingly if this applies to you.

How to Use This Roth IRA Calculator: Step-by-Step

What the Calculator Inputs Mean

The Roth IRA calculator above is free, instant, and pre-loaded with 2026 IRS limits. Here is exactly what each field means:

- Current Age — Your age today. The earlier you start, the more compound growth works in your favor.

- Retirement Age — Most users target 65. Adjusting this shows how a few extra years dramatically affects your final balance.

- Annual Contribution — Enter up to $7,500 (or $8,600 if age 50+). Even contributing $3,000/year produces significant tax-free growth.

- Expected Rate of Return — Historically, a diversified stock portfolio averages 6–7% annually. Conservative investors can use 5%.

- Current Roth IRA Balance — Enter $0 if you’re starting fresh. Existing balances accelerate growth projections significantly.

3 Real-Life Scenarios: See the Tax-Free Growth in Action

These are real projection examples using 2026 limits and standard market assumptions — not hypothetical disclaimers.

| Scenario | Profile | Age | Annual Contribution | Rate of Return | Projected Balance at 65 |

|---|---|---|---|---|---|

| 🟢 Early Starter | Jamie, 28 | 28 | $7,500/yr | 7% | ~$2,100,000 |

| 🟡 Mid-Career | Marcus, 42 | 42 | $7,500/yr | 6.5% | ~$680,000 |

| 🔵 Catch-Up Saver | Sandra, 55 | 55 | $8,600/yr | 6% | ~$185,000 |

What This Means For You:

- Jamie’s $7,500/year grows to $2.1 million — entirely tax-free at withdrawal.

- Marcus starts at 42 and still builds nearly $700K without paying a dollar in retirement taxes.

- Sandra uses the over-50 catch-up and still accumulates $185K with just 10 years of contributions.

The core lesson: starting even 5 years earlier can add hundreds of thousands to your final tax-free balance. If you’re currently prioritizing debt payoff, use our debt consolidation calculator to identify exactly how much cash you can free up to start contributing to a Roth IRA now.

To see how compound interest powers every scenario above, explore our dedicated compound interest calculator for a deeper breakdown of growth over time.

What Your Results Actually Mean

Your calculator result is your projected tax-free retirement balance — meaning you will owe $0 in federal income tax on qualified withdrawals after age 59½, as long as the account has been open for at least 5 years. This is the Roth IRA’s most powerful advantage over every other retirement account.

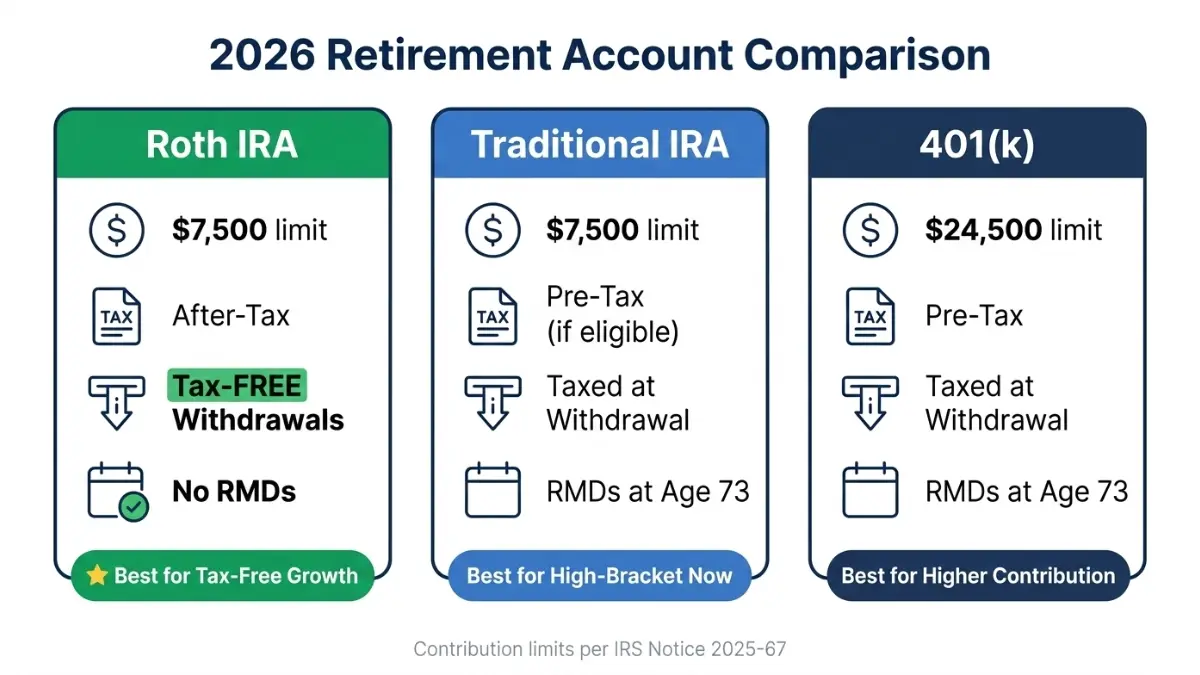

Roth IRA vs. Traditional IRA vs. 401(k): Which Wins in 2026?

The 2026 Tax Math: Roth IRA vs. Traditional IRA

The most common question on Google is: should I use a Roth IRA or a Traditional IRA? The answer depends on one variable — whether your tax rate is higher today or in retirement.

| Feature | Roth IRA | Traditional IRA | 401(k) |

|---|---|---|---|

| 2026 Contribution Limit | $7,500 | $7,500 | $24,500 |

| Tax on Contributions | After-tax | Pre-tax (if eligible) | Pre-tax |

| Tax on Withdrawals | Tax-FREE | Taxed as income | Taxed as income |

| Required Minimum Distributions | None | Yes, age 73 | Yes, age 73 |

| Income Limits | Yes | No | No |

| Early Withdrawal of Contributions | Penalty-free | 10% penalty | 10% penalty |

Choose Roth IRA if:

- You’re in a lower tax bracket now than you expect in retirement

- You want zero RMDs and full flexibility

- You’re under 40 and in early career earnings

Choose Traditional IRA if:

- You’re in a high bracket now and expect lower income in retirement

- You want to reduce taxable income this year

For a detailed side-by-side breakdown, read our comprehensive 401(k) vs IRA guide that covers every scenario by income level and age.

The Optimal Retirement Contribution Stacking Order

Most financial experts agree on this priority sequence for 2026:

- 401(k) up to employer match — This is free money. Always capture it first.

- Max your Roth IRA — $7,500 of tax-free growth is your next priority.

- Max your 401(k) — Contribute the remaining $17,000 to hit the $24,500 limit.

- Taxable brokerage — Invest additional savings here if you’ve maxed all tax-advantaged accounts.

Use our retirement calculator to model how following this stacking order accelerates your path to financial independence.

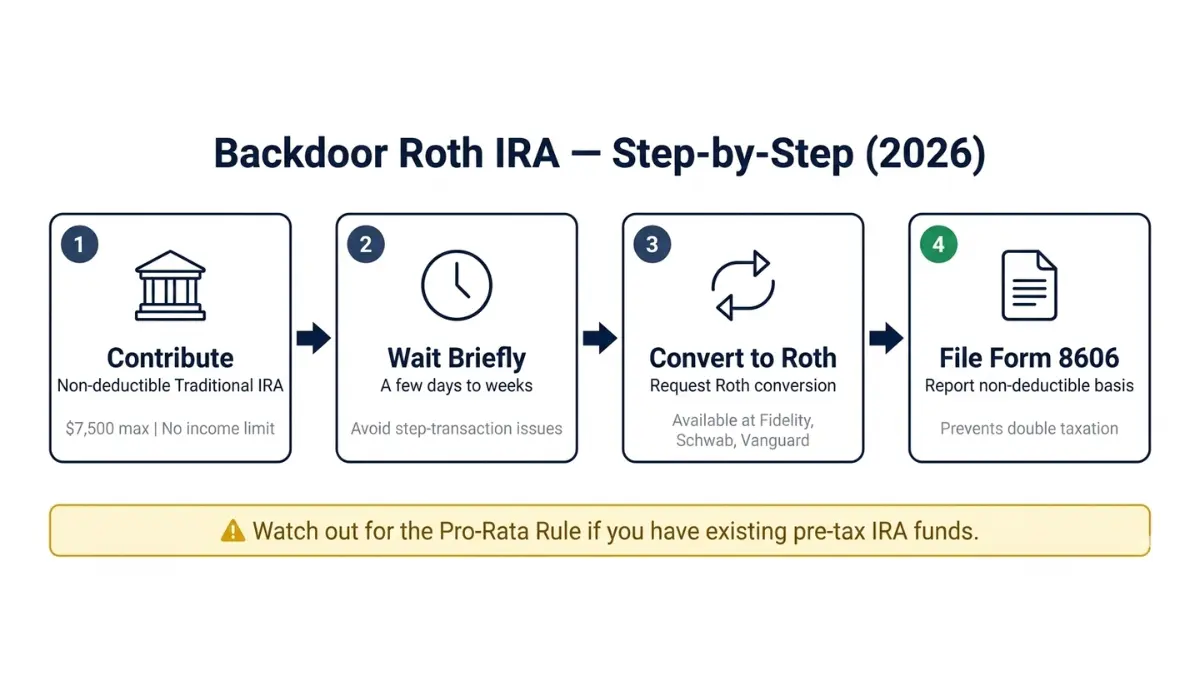

Earn Too Much? The Backdoor Roth IRA Strategy for 2026

What Is a Backdoor Roth IRA?

If your income exceeds $168,000 (single) or $252,000 (married filing jointly), you cannot contribute directly to a Roth IRA. The Backdoor Roth IRA is a completely legal strategy that bypasses this income restriction. According to Vanguard’s 2026 Roth IRA income limits guide, this strategy involves contributing to a Traditional IRA first, then converting it to a Roth.

How to Execute a Backdoor Roth IRA (4 Steps)

- Contribute to a Traditional IRA — Make a non-deductible contribution (no income limits apply to non-deductible Traditional IRA contributions).

- Wait briefly — Most advisors recommend waiting a few days to weeks to avoid “step transaction” scrutiny.

- Convert to Roth IRA — Request a Roth conversion from your brokerage. This is a standard transaction at Fidelity, Schwab, and Vanguard.

- Report on Form 8606 — File IRS Form 8606 with your tax return to document the non-deductible basis. This prevents you from being taxed twice.

⚠️ The Pro-Rata Rule: The Trap Most People Fall Into

If you have any existing pre-tax Traditional IRA money, the pro-rata rule will partially tax your Backdoor Roth conversion. The IRS treats all your Traditional IRA balances as one pool.

Example: You have $50,000 in a pre-tax Traditional IRA and convert a new $7,500 non-deductible contribution. Only 13% of the conversion is tax-free. The remaining 87% is taxable. Solution: Roll your pre-tax Traditional IRA into your employer’s 401(k) first, then execute the Backdoor Roth. If you’re planning major financial moves alongside this strategy, our investment calculator can help model the tax-adjusted returns.

The Saver’s Credit: The Hidden Tax Benefit Most Americans Miss

Lower-income earners who contribute to a Roth IRA may qualify for the Saver’s Credit — a direct dollar-for-dollar reduction in your federal tax bill. This is separate from any deduction and can be worth up to $1,000 for single filers or $2,000 for married couples. Learn about qualification rules at IRS Topic 610 on the Retirement Savings Contributions Credit.

| Filing Status | Income Limit (2026) | Maximum Credit |

|---|---|---|

| Married Filing Jointly | $80,500 MAGI | $2,000 |

| Head of Household | $60,375 MAGI | $1,000 |

| Single | $40,250 MAGI | $1,000 |

Important: The Saver’s Credit is only available through tax year 2026. Starting in 2027, SECURE 2.0 replaces it with the Saver’s Match — a direct government deposit into your retirement account instead of a tax credit. If you’re eligible for the Saver’s Credit this year, this is your last opportunity to claim it in its current form.

Also worth knowing: if you’re enrolled in an HSA alongside your Roth IRA, read our guide on how HSA accounts compare to 401(k) tax advantages in 2026 — the combination is one of the most powerful tax-minimization strategies available.

Roth IRA Calculator 2026 — Frequently Asked Questions

1. What is the Roth IRA contribution limit for 2026?

The Roth IRA contribution limit for 2026 is $7,500 for those under age 50, and $8,600 for those age 50 and older (including the $1,100 catch-up contribution). This applies to all your IRAs combined.

2. How much will a Roth IRA grow in 20 years?

At 7% average annual return, contributing $7,500/year for 20 years results in approximately $327,000 in tax-free growth. Starting at age 25 with the same contribution, you’d reach over $1.5 million by age 65.

3. Can I contribute to a Roth IRA if my income is too high?

Yes — through the Backdoor Roth IRA strategy. You contribute to a non-deductible Traditional IRA first, then convert those funds to a Roth IRA. This is legal, widely used, and available at all major brokerages.

4. What is the difference between a Roth IRA and a Traditional IRA?

Roth IRA contributions are made with after-tax dollars — you pay tax now and owe nothing in retirement. Traditional IRA contributions may be tax-deductible now, but all withdrawals in retirement are taxed as ordinary income. Roth IRAs also have no RMDs.

5. What is MAGI and how does it affect Roth IRA eligibility?

MAGI (Modified Adjusted Gross Income) is your AGI from Form 1040 with certain deductions added back. It determines whether you can make a full, partial, or no Roth IRA contribution. For 2026, single filers with MAGI above $168,000 cannot contribute directly.

6. Can I withdraw from my Roth IRA early without penalty?

You can withdraw your contributions (not earnings) at any time, tax-free and penalty-free. Withdrawing earnings before age 59½ and before the 5-year rule is met results in a 10% penalty plus income tax, with certain exceptions (first home purchase, disability, etc.).

7. What happens if I contribute too much to my Roth IRA?

The IRS imposes a 6% excise tax on excess contributions for each year the excess remains in the account. Remove excess contributions by the tax filing deadline (April 15, 2027 for 2026 contributions) to avoid the penalty.

8. Is a Roth IRA better than a 401(k)?

Neither is universally better. The optimal strategy is both — max your 401(k) to capture employer match first, then fund your Roth IRA for tax-free growth. The 401(k) gives you a higher contribution limit ($24,500 vs $7,500), but the Roth IRA offers tax-free withdrawals and no RMDs. For a full comparison, read our 401(k) explained guide.

9. When is the deadline to contribute to a Roth IRA for 2026?

You have until April 15, 2027 to make 2026 Roth IRA contributions. This gives you flexibility to wait until you know your final MAGI before deciding how much you can contribute.

10. What is the Backdoor Roth IRA and is it legal?

Completely legal and widely recommended by CFPs. It involves contributing to a non-deductible Traditional IRA, then converting to a Roth. The IRS has never prohibited this strategy. Watch out for the pro-rata rule if you have existing pre-tax IRA funds.

11. How does compound interest work inside a Roth IRA?

Every dollar inside your Roth IRA grows tax-deferred and is withdrawn tax-free. Compound interest means you earn returns on your returns — and because there are no RMDs, your Roth IRA can compound for your entire lifetime. A $7,500 annual contribution at 7% over 35 years grows to approximately $1.1 million entirely tax-free.

Also explore: If you’re building a complete retirement plan, pair your Roth IRA strategy with our retirement savings by age benchmarks guide to see exactly where you should be at every decade.

📋 Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or investment advice. Roth IRA contribution limits, income thresholds, and tax rules are subject to change by the IRS. All projections shown are estimates based on assumed rates of return and are not guaranteed. Consult a qualified financial advisor or CPA before making retirement contribution decisions. Verified against IRS Notice 2025-67, published November 2025.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.