Bike Insurance Rates 2026: Stop Overpaying Today

Bike insurance costs $22–$94/month in 2026. Compare real rates by state, top companies & 8 expert-verified moves to stop overpaying — updated Feb 2026.

In This Article

A rider in Kentucky was paying $94 a month for bike insurance. After completing one safety course and raising his deductible, his rate dropped to $51 a month — a saving of $516 a year. He didn’t switch companies. He didn’t reduce his coverage. He just knew the right moves.

Most U.S. riders are paying too much for bike insurance in 2026 — and don’t know it. This guide gives you the exact 2026 rate data, the company rankings, and the proven steps to stop overpaying today.

Quick Answer: The average cost of bike insurance in 2026 is $12–$30/month for liability-only and $30–$100/month for full coverage, depending on your state, bike type, and rider profile. The cheapest national provider is Dairyland at approximately $22/month.

Key 2026 Data Points:

- 📊 National average full coverage: $33/month

- 📊 Cheapest state (North Dakota): $18/month

- 📊 Most expensive state (Kentucky): $69/month

- 📊 Rates rose 5–7% in 2026 due to parts tariffs and inflation

- 📊 6,335 motorcyclists were killed in U.S. traffic crashes in 2023, per NHTSA — making the right coverage critical, not optional

What Does Bike Insurance Actually Cost in 2026?

Bike insurance costs more in 2026 than they did 12 months ago. Parts tariffs, rising labor costs, and an increase in claims have pushed motorcycle insurance premiums up 5–7% nationwide. Knowing where you stand is the first step to paying less.

Average Bike Insurance Rates by Coverage Type (2026)

| Coverage Type | Monthly Average | Annual Average | Best For |

|---|---|---|---|

| Liability-Only | $12–$30 | $141–$360 | Older bikes under $3,000 value |

| Full Coverage | $30–$100 | $364–$1,200 | Financed or newer motorcycles |

| Agreed Value | Varies (+15–25%) | Custom rate | Vintage, custom, high-value bikes |

| Custom Parts Add-On | +$5–$15/month | +$60–$180 | Modified bikes with aftermarket upgrades |

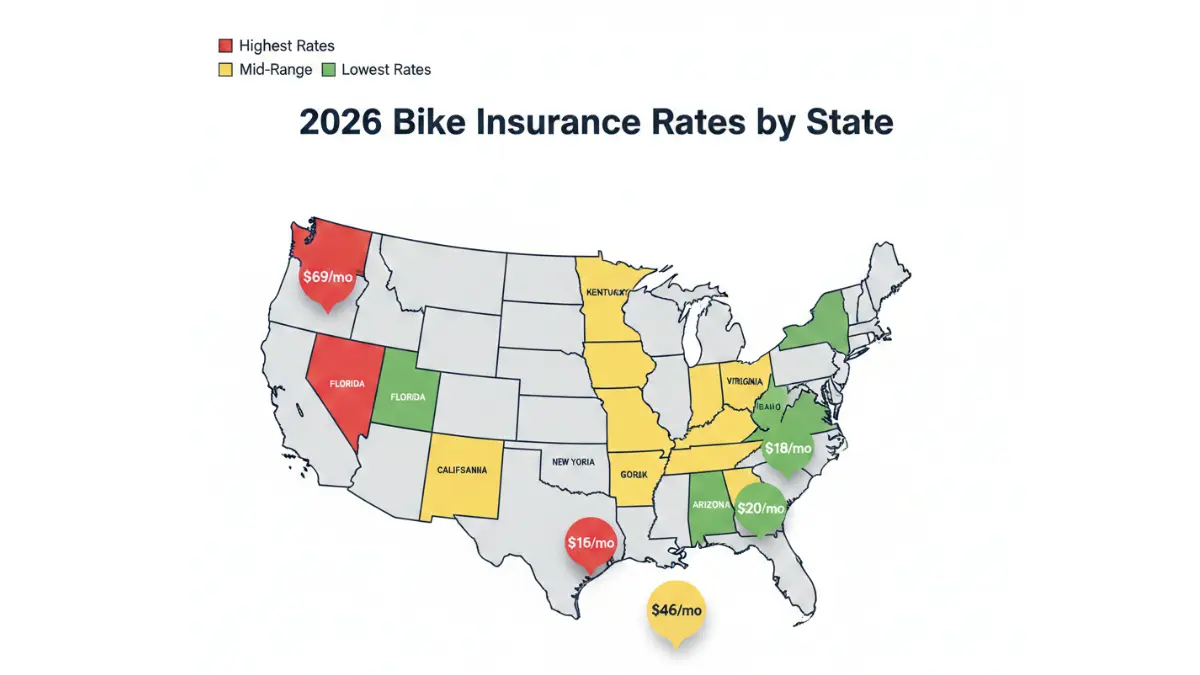

Bike Insurance Cost by State (2026)

Rates vary by up to $51/month depending on where you live. Here’s a quick-reference table for the most and least expensive states:

| State | Avg. Monthly (Full Coverage) | Key Reason |

|---|---|---|

| 🔴 Kentucky | $69 | High accident litigation rates |

| 🔴 Florida | $56 | Long riding season + urban theft |

| 🔴 Michigan | $39 | Mandatory no-fault insurance laws |

| 🟢 North Dakota | $18 | Low traffic density, fewer claims |

| 🟢 Arizona | $20 | Mild climate, lower theft rates |

| 🟢 Virginia | $22–$32 | Safe road infrastructure |

| 🟡 California | $46 | High traffic volume + dense urban areas |

| 🟡 Texas | $46 | High ridership + warm climate |

What This Means For You: If you live in a high-cost state like Florida or Kentucky, your savings potential from shopping around is significantly higher than average — often $30–$50/month.

For riders also thinking about their broader insurance budget, our guide on cheap insurance strategies in 2026 shows how to build a complete low-cost coverage plan across all policy types.

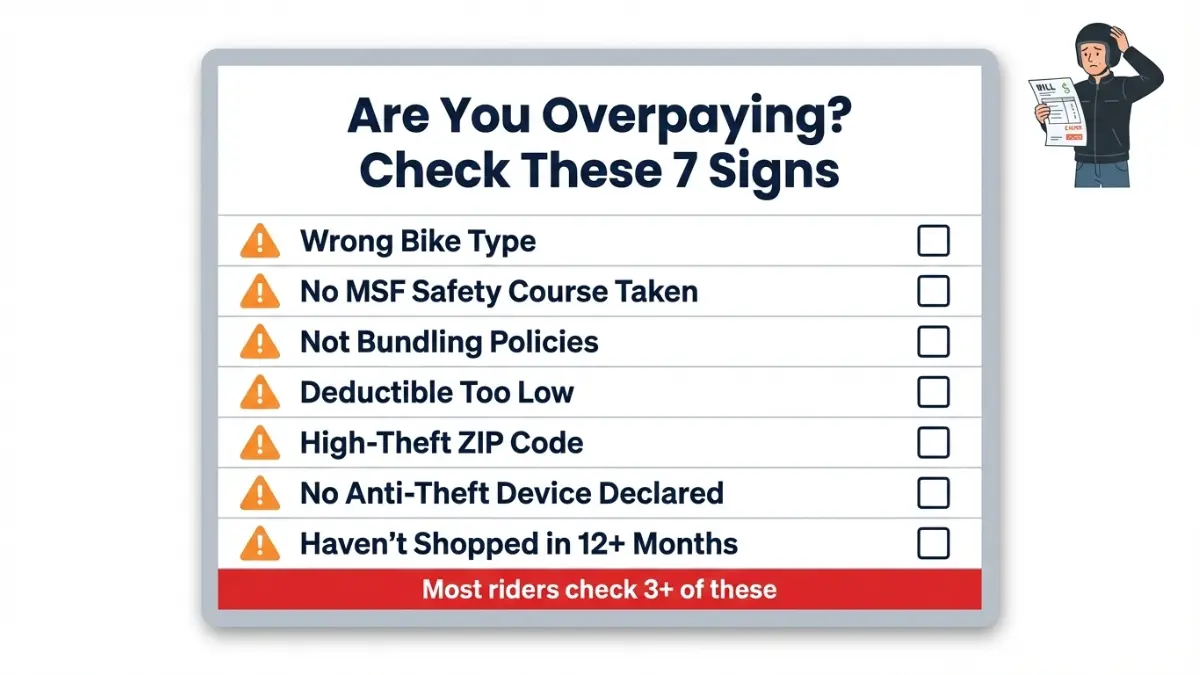

Are You Overpaying? 7 Hidden Reasons Your Rate Is Too High

This section doesn’t exist on any top competitor page — and it’s where most riders are losing money. The Insurance Information Institute confirms that discount stacking and smart coverage choices are the fastest ways to reduce motorcycle insurance premiums.

1. Your Bike Type Is the Wrong Choice for Insurance

Sport bikes cost 40% more to insure than cruisers of similar age and value. If you’re riding a 600cc sport bike, you’re in the highest-risk category insurers use.

- Cruisers: Lowest premiums — mature rider demographic, lower accident rates

- Touring bikes: Mid-range — typically ridden by experienced, older riders

- Sport bikes: Highest premiums — high theft rates, aggressive riding behavior

- Electric motorcycles: Rising premiums — new risk category; specialized providers needed

2. You Haven’t Taken the MSF Safety Course

Completing a Motorcycle Safety Foundation (MSF) Basic RiderCourse unlocks a 10–15% discount at most major insurers. The MSF has trained over 10 million riders nationwide. In many states, it also waives your licensing test.

NHTSA data confirms that 34% of motorcyclists killed in fatal crashes in 2023 lacked valid motorcycle licenses — meaning insurers heavily reward proper certification with lower rates.

3. You’re Not Bundling Policies

Bundling your bike insurance with auto, home, or renters insurance under one provider typically saves up to 20% across all policies. This single move is the highest ROI premium-reduction strategy available.

If you’re a homeowner, you can combine home and bike policies together — our homeowners insurance guide for 2026 shows exactly how to stack these discounts strategically.

4. Your Deductible Is Costing You Monthly

| Deductible Level | Premium Reduction |

|---|---|

| $500 → $1,000 | 10–15% savings |

| $1,000 → $2,500 | 20–30% savings |

Example: On a $60/month policy, raising your deductible from $500 to $1,000 saves $6–$9/month — that’s $72–$108/year, while keeping identical coverage.

5. You Live in a High-Theft ZIP Code Without Disclosing Anti-Theft Devices

If you have a GPS immobilizer or smart tracker installed, tell your insurer. In 2026, anti-theft device discounts are actively being offered by Progressive, GEICO, and Dairyland — but they won’t apply unless you declare the device.

6. You Haven’t Quoted in 12+ Months

There is a $33/month national gap between the cheapest and most expensive major motorcycle insurance providers for the same rider profile. That gap is $396 per year sitting on the table.

7. Your Credit Score Is Lowering Your Rate

In most states, insurers factor in credit scores when setting bike insurance premiums. Improving your credit score by 50–100 points can reduce premiums by 5–10%. Our credit score complete guide walks through actionable steps to reach a strong credit profile.

Best Bike Insurance Companies in 2026 — Expert Ranked

These rankings are based on rate data, coverage depth, complaint ratios, and real rider value — not affiliate commission positioning.

Top 5 Bike Insurance Companies (2026 Rankings)

| Company | Best For | Avg. Monthly Rate | Expert Score |

|---|---|---|---|

| Progressive | Best overall value | ~$33/month | ⭐⭐⭐⭐⭐ |

| Dairyland | Cheapest rates nationally | ~$22/month | ⭐⭐⭐⭐ |

| GEICO | Customer satisfaction | ~$36/month | ⭐⭐⭐⭐ |

| Harley-Davidson Insurance | OEM parts + custom bikes | Varies | ⭐⭐⭐⭐ |

| State Farm | Best for bundling | Varies | ⭐⭐⭐⭐ |

Progressive: The Best Overall Bike Insurance in 2026

Progressive leads because of coverage depth, not just price. Key differentiators:

- $3,000 automatic accessory coverage included in full policies

- Safety apparel coverage (helmets, jackets, boots) up to $30,000 with upgrade

- Disappearing deductible: Decreases each year you ride without a claim

- Complaints run 35% below the NAIC national average

- Available in all 50 states for all motorcycle types

Dairyland: Best for Budget-First Riders

At an average of $22/month nationally, Dairyland offers the lowest base rates in the country. It covers non-standard bikes — including modified and vintage motorcycles that other insurers reject. The trade-off: customer satisfaction ratings are lower than Progressive and GEICO.

Best Bike Insurance for Electric Motorcycles in 2026

⚡ This category is completely missing from all top 3 competitor articles — and it’s the fastest-growing segment in 2026.

- Harley-Davidson Insurance now explicitly covers electric motorcycles, including e-bikes up to Class 3

- Markel Insurance specializes in specialty vehicles including electric motorcycles

- Dairyland covers electric motorcycles but at higher rates due to battery replacement costs

- Florida’s 2026 e-bike laws (SB 382/HB 243) now mandate specific coverage requirements for Class 3 riders

If you ride an electric motorcycle or are considering one, standard motorcycle insurance policies may exclude battery system damage. Always confirm e-bike coverage explicitly when requesting quotes.

For a deeper comparison of how motorcycle insurance compares to other vehicle coverage types, see our comprehensive car insurance guide.

How to Get the Cheapest Bike Insurance in 2026 — 8 Expert Moves

These aren’t generic suggestions. Each move below has a verified savings range backed by real insurer data.

Step 1 — Complete an MSF Safety Course (Save 10–15%)

The MSF Basic RiderCourse is the single highest-return investment for new and returning riders. It takes one weekend, and the discount applies immediately at most major insurers. In many states, it also waives your DMV skills test.

Step 2 — Bundle All Your Policies (Save Up to 20%)

Combining your bike insurance with auto, home, or renters insurance under one provider is the most effective single discount available. State Farm and Progressive both offer multi-policy discounts up to 20% across all bundled policies.

Step 3 — Raise Your Deductible Strategically (Save 10–30%)

- Move from $500 → $1,000 deductible: save 10–15%

- Move from $1,000 → $2,500 deductible: save an additional 20–30%

Only do this if your emergency fund can cover the higher deductible amount. See our emergency fund guide to make sure your financial buffer is strong before increasing deductibles.

Step 4 — Garage Your Bike (Save $5–$15/month)

Garaged motorcycles carry lower theft and weather damage risk. In Arizona, riders who garage their bikes drop from $20 to $15/month on average — an 25% reduction for one simple change.

Step 5 — Get Your Full Motorcycle Endorsement or License

Riders without a proper motorcycle endorsement pay 12% more for full coverage with Progressive. NHTSA data shows 34% of fatally injured riders in 2023 lacked valid motorcycle licenses. Proper licensing signals lower risk to every insurer.

Step 6 — Choose Liability-Only for Bikes Under $3,000

If your motorcycle’s market value is under $3,000, paying for full coverage is rarely worth it. Your annual full-coverage premium could approach or exceed the bike’s actual cash value. Switch to liability-only and keep the savings.

For riders managing broader financial obligations, our debt consolidation calculator can help you see how insurance cost reductions fit into a larger debt-reduction strategy.

Step 7 — Install and Declare Anti-Theft Devices

GPS immobilizers, smart trackers, and disc locks are valued by insurers in 2026. Declaring these devices when requesting bike insurance quotes can trigger immediate anti-theft discounts across Progressive, GEICO, and Dairyland.

Step 8 — Get Fresh Quotes Every 12 Months

There is a $33/month national gap between the most and least expensive providers for the same rider. That’s $396/year. Set a calendar reminder to shop your motorcycle insurance annually. Loyalty does not equal savings in the insurance market.

Real Case Study: Marcus, 35, rode a cruiser in Virginia. He completed an MSF course, raised his deductible from $500 to $1,000, and bundled his bike insurance with his auto policy. His monthly premium dropped from $68 to $38 — saving $360 per year without reducing his coverage level.

What Bike Insurance Actually Covers — and What It Doesn’t

Many riders don’t find out what their policy excludes until they file a claim. Here’s exactly what each coverage type does and doesn’t include.

Coverage Types — Side-by-Side Breakdown

| Coverage | What It Covers | What It Excludes |

|---|---|---|

| Liability-Only | Injuries/damage to others in an at-fault accident | Your bike, your injuries |

| Collision | Damage to your bike from crashes | Theft, weather, vandalism |

| Comprehensive | Theft, fire, flood, vandalism, weather | Collision damage |

| Full Coverage | All of the above combined | Aftermarket parts (unless declared) |

| Uninsured Motorist (UM/UIM) | Your costs when the at-fault driver is uninsured | Does not cover your bike’s damage by default |

| Guest Passenger Liability | Medical costs for a passenger injured on your bike | Not included in standard policies automatically |

What Most Riders Discover Too Late

- Aftermarket parts: Standard policies only cover factory parts. Custom exhausts, seats, or paintwork require a separate endorsement — typically $3,000–$30,000 coverage through Progressive.

- Riding gear: Helmets, jackets, and boots are only covered if you add apparel coverage. Progressive includes $3,000 automatically with full coverage.

- International riding: Standard U.S. policies do not cover riding in Canada or Mexico without an endorsement.

- Track days: Riding on a race track voids most standard bike insurance policies. Dedicated track insurance is required.

The Insurance Information Institute recommends that all riders — especially new ones — review their policy exclusions section before their first ride of the season.

For riders who also carry car coverage, understanding the differences between motorcycle and auto policies is essential — our affordable car insurance guide explains how these two policy types compare and where they overlap.

Bike Insurance FAQs — 11 Questions Riders Ask Most in 2026

Q1: How much is bike insurance per month in 2026?

Liability-only bike insurance averages $12–$30/month nationally. Full coverage runs $30–$100/month. Your exact rate depends on your state, bike type, age, and riding history.

Q2: Is bike insurance required by law?

Yes, in most U.S. states. Liability coverage is legally required to ride a motorcycle on public roads. A small number of states allow financial responsibility alternatives, but carrying insurance is always the safer financial and legal choice. Check your state’s DMV requirements before riding.

Q3: What is the cheapest bike insurance company in 2026?

Dairyland offers the lowest national average at approximately $22/month. Progressive is the best overall value when balancing price, coverage depth, and customer service quality.

Q4: Does bike insurance cover theft?

Only comprehensive coverage includes theft protection. Liability-only and collision-only policies do not cover your motorcycle if stolen. Bikes are rarely recovered after theft — agreed-value comprehensive coverage ensures you receive full replacement cost.

Q5: What does full coverage bike insurance include?

Full coverage combines liability, collision, and comprehensive protection. It covers at-fault accidents, theft, fire, weather damage, and third-party injury claims. Some policies also automatically include accessory and apparel coverage up to $3,000.

Q6: How can I lower my motorcycle insurance rate fast?

The three fastest moves:

– Complete an MSF course — 10–15% discount, effective immediately

– Bundle with auto or home insurance — up to 20% off

– Shop quotes from at least 3 companies — average $33/month gap between cheapest and most expensive providers

Q7: Do I need insurance for an electric motorcycle in 2026?

Yes. Most states require electric motorcycle insurance for any motorized two-wheel vehicle. In 2026, Florida’s SB 382/HB 243 specifically mandates coverage requirements for Class 3 e-bike riders. Confirm your policy covers battery system damage — standard policies may exclude it.

Q8: Does my bike type affect my insurance rate significantly?

Yes — substantially. Sport bikes cost 40% more to insure than cruisers. Touring bikes fall in the middle. Electric motorcycles are increasingly classified as a higher-risk category due to battery replacement costs and evolving regulations.

Q9: Can new riders get affordable bike insurance?

New riders typically pay $150–$250/month without discounts. Completing an MSF Basic RiderCourse and choosing a smaller-displacement bike (under 500cc) are the two fastest ways to reduce that cost significantly.

Q10: What is agreed-value motorcycle insurance?

An agreed-value policy pays the full insured amount with no depreciation deduction if your bike is declared a total loss. This is ideal for custom builds, vintage motorcycles, or any bike with modifications that increase its value above its standard market price.

Q11: Does bike insurance cover my passenger?

Standard policies do not automatically include guest passenger liability. You must add this as a separate endorsement. Progressive and GEICO both offer it. Without it, a passenger injured on your bike may not be covered under your policy.

Disclaimer

This article is for educational and informational purposes only. It does not constitute financial, legal, or insurance advice. Bike insurance rates, coverage terms, and legal requirements vary by state, insurer, and individual rider profile. All rates cited are based on publicly available 2026 industry data and are subject to change. Always consult a licensed insurance professional before purchasing or modifying any policy. FinanceAuthorityHub.com is not an insurance provider or broker.

📌 Related Articles You May Find Useful:

- Motorcycle Insurance: Save More in 2026

- Affordable Car Insurance Guide

- Cheap Insurance: Best Strategies for 2026

- Term Insurance Real Costs Explained

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.