Mortgage Pre-Approval 2026: 6-Step Expert Guide

Learn how to get mortgage pre-approval in 2026 with our expert 6-step guide. Includes credit score requirements, document checklists, lender comparisons, and real success stories.

In This Article

In 2026’s competitive housing market, 73% of successful homebuyers secured pre-approval letters before making offers. Whether you’re a first-time buyer or navigating complex income scenarios, mortgage pre-approval is your gateway to homeownership—and this expert guide shows you exactly how to get approved, even with credit challenges.

Understanding Mortgage Pre-Approval in 2026

Mortgage pre-approval is a lender’s conditional commitment to loan you a specific amount based on verified financial documentation. Unlike pre-qualification (which relies on self-reported estimates), pre-approval involves hard credit checks, income verification, and asset review—making it the gold standard for serious homebuyers.

Why Mortgage Pre-Approval Matters

1. Seller Credibility

In competitive markets, sellers prioritize buyers with pre-approval letters. A pre-approval proves you’re financially vetted and ready to close, giving your offer 40% more weight than unqualified bids.

2. Budget Clarity

Pre-approval reveals your exact borrowing power before you fall in love with unaffordable properties. You’ll know whether you can afford a $300,000 or $450,000 home—preventing wasted time and disappointment.

3. Rate Shopping Leverage

Applying with 3+ lenders within a 45-day window counts as a single credit inquiry under FICO scoring. This lets you compare rates and terms without tanking your credit score. According to Freddie Mac data, rate differences of 0.25% on a $300,000 loan cost borrowers $47/month—that’s $16,920 over 30 years.

4. Faster Closing

Pre-approval accelerates final mortgage approval because lenders already verified your financials. You can close in 30-35 days versus 45-60 days for unprepared buyers.

5. Negotiation Power

With pre-approval, you can waive financing contingencies in hot markets, making your offer more attractive to sellers competing against cash buyers.

Pre-Approval vs. Pre-Qualification: Key Differences

| Factor | Pre-Qualification | Mortgage Pre-Approval |

|---|---|---|

| Credit Check | Soft inquiry (no impact) | Hard inquiry (3-5 point drop) |

| Documentation | Self-reported estimates | Verified pay stubs, tax returns, bank statements |

| Accuracy | Rough estimate | Conditional commitment |

| Seller Appeal | Weak | Strong competitive advantage |

| Timeline | 15-30 minutes | 3-14 days |

| Validity | Not binding | 30-90 days, subject to conditions |

For homebuying guidance, explore our complete first-time homebuyer guide covering down payments, closing costs, and market timing strategies.

How to Get Pre-Approved for a Mortgage: 6 Expert Steps

Step 1: Check Your Credit Score & Credit Reports

Action Required: Pull free credit reports from all three bureaus at AnnualCreditReport.com before lenders do.

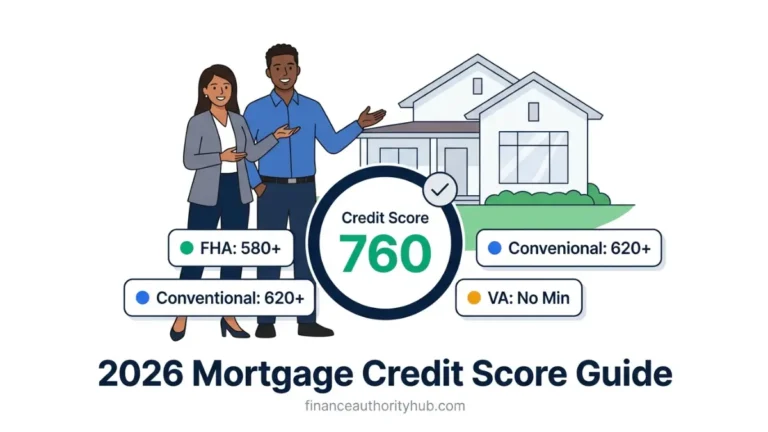

2026 Credit Score Minimums by Loan Type:

- Conventional loans: 620 minimum

- FHA loans: 580 (3.5% down) or 500 (10% down)

- VA loans: 620 typical (varies by lender)

- USDA loans: 640 typical

- Jumbo loans: 700+ preferred

Why This Matters: 34% of credit reports contain errors according to FTC research. One client raised their score from 615 to 642 by disputing $2,500 in erroneous medical debt—qualifying them for conventional financing instead of higher-rate FHA loans.

Credit Improvement Timeline:

- Immediate (24 hours): Dispute errors for rapid rescoring

- 30 days: Pay down credit card balances below 30% utilization

- 60-90 days: Consistent on-time payments rebuild history

Avoid new credit accounts, large purchases, or job changes during your mortgage pre-approval process. Need to improve your score first? See our complete credit score guide for actionable strategies.

Step 2: Calculate Your Debt-to-Income (DTI) Ratio

Formula: (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Example Calculation:

- Monthly debts: $2,000 mortgage + $400 car + $200 student loan = $2,600

- Gross monthly income: $7,500

- DTI: ($2,600 ÷ $7,500) × 100 = 34.7%

Lender DTI Standards:

- 36% or below: Best rates and terms

- 43-45%: Acceptable for most conventional loans

- 50%: Maximum for FHA loans

How to Lower DTI Before Applying:

- Pay off small debts entirely (eliminates monthly payment from calculation)

- Increase income with side gigs or raises (verified income boosts capacity)

- Avoid new debt—no car loans or large credit card purchases

Student Loan DTI Strategy: If you’re on an income-driven repayment plan, lenders use your actual $150/month payment—not 1% of your $60,000 balance ($600). This can save you thousands in borrowing power.

Use our home affordability calculator to estimate your maximum purchase price based on income and debts.

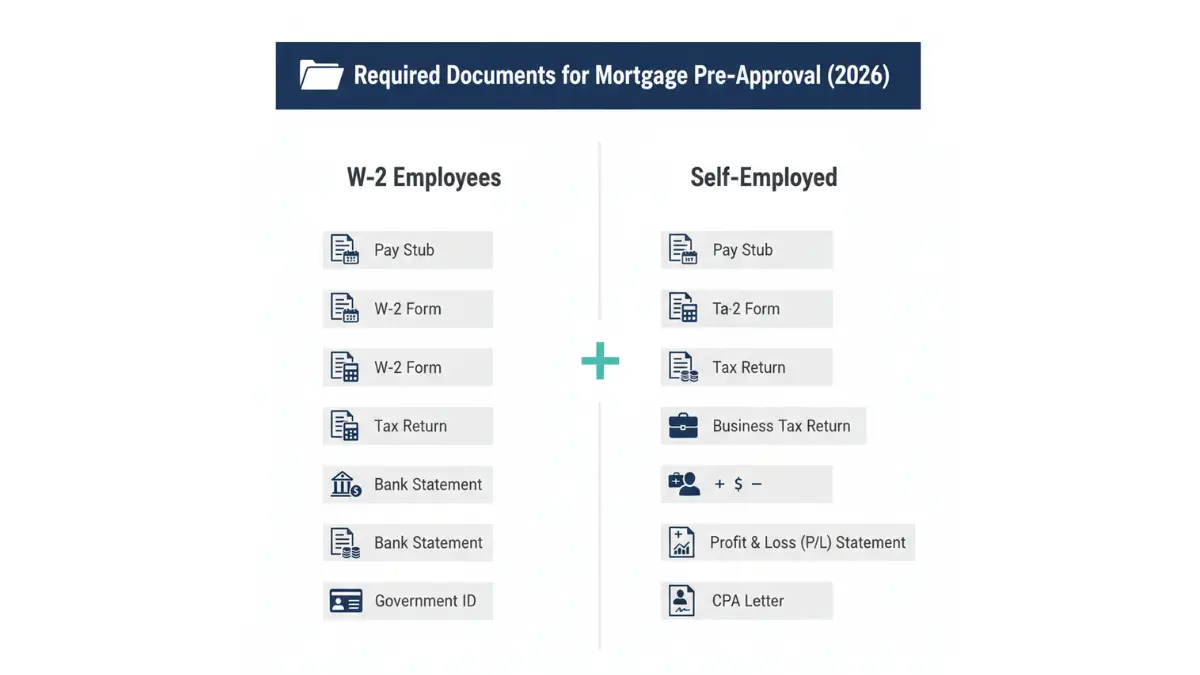

Step 3: Gather Required Financial Documentation

Mortgage pre-approval requires extensive documentation. Missing papers delay approval by 7-14 days.

Standard W-2 Employee Checklist:

- ✅ Pay stubs (most recent 30 days)

- ✅ W-2 forms (past 2 years)

- ✅ Federal tax returns (past 2 years, all schedules)

- ✅ Bank statements (all accounts, past 2 months)

- ✅ Investment/retirement account statements

- ✅ Government-issued photo ID

- ✅ Social Security card

- ✅ Gift letters (if receiving down payment assistance)

Self-Employed/1099 Additional Requirements:

- ✅ Business tax returns (2 years, all schedules)

- ✅ Profit & loss statements (year-to-date)

- ✅ Business bank statements (2 months)

- ✅ CPA letter confirming income and business status

Pro Tip: Lenders average your last 2 years of net income for self-employed borrowers. If 2024 was a weak year, waiting until 2026 tax filing might show a stronger 2-year average and increase approval amounts by $50,000-$85,000.

Step 4: Choose and Compare 3+ Mortgage Lenders

Why Multiple Lenders: Rates vary by 0.25%-0.75% between institutions. On a $300,000 loan, a 0.25% difference saves $47/month ($16,920 over 30 years).

Where to Apply:

- Banks (Wells Fargo, Chase, Bank of America): Relationship discounts for existing customers

- Credit Unions (Navy Federal, PenFed): Often 0.25%-0.5% lower rates for members

- Online Lenders (Rocket Mortgage, Better.com): Faster digital processes, 24-48 hour decisions

- Mortgage Brokers: Access to 20+ lenders at no cost to you

Comparison Factors Beyond Rate:

- APR (includes fees—more accurate than rate alone)

- Origination fees ($0-$1,500 varies wildly)

- Underwriting timeline (7-14 days standard, 3-5 days for some online lenders)

- Loan programs offered (conventional, FHA, VA, USDA, jumbo)

- Customer service quality (read reviews on ConsumerAffairs, Trustpilot)

45-Day Shopping Window: According to FICO methodology, multiple mortgage inquiries within 45 days count as ONE hard pull. Apply strategically within this window to protect your credit score.

Planning to refinance later? Check our mortgage refinance calculator to estimate future savings.

Step 5: Submit Applications & Complete Verification

Application Timeline:

- Online: 10-20 minutes per lender

- Phone: 15-30 minutes with loan officer

- In-person: Schedule branch appointment (30-45 minutes)

What Lenders Verify:

- Identity (government ID, Social Security number)

- Income (pay stubs, tax returns, W-2s)

- Employment (may call employer—give HR a heads up)

- Assets (bank statements, investment accounts for down payment)

- Credit (hard pull from Experian, TransUnion, Equifax)

- Debts (credit report shows all accounts)

Processing Timeline:

- Automated underwriting: Same day to 48 hours

- Manual underwriting: 7-10 business days

- Complex scenarios (self-employed, multiple income sources): 10-14 days

Hard Inquiry Impact: Your credit score drops 3-5 points per hard inquiry but recovers within 6-12 months. The 45-day window groups multiple mortgage inquiries, minimizing damage.

Step 6: Receive & Use Your Mortgage Pre-Approval Letter

What’s Included in Your Letter:

- Maximum loan amount approved (e.g., “$350,000”)

- Loan type (Conventional, FHA, VA, USDA, jumbo)

- Estimated interest rate (subject to rate lock)

- Expiration date (typically 30-90 days)

- Conditions (employment verification, no new debt, final appraisal)

How to Use Pre-Approval Strategically:

- Present to real estate agents (proves serious buying power)

- Attach to purchase offers (seller credibility)

- Request specific amounts (can ask for pre-approval at $325,000 for a $310,000 property, not your $380,000 maximum)

- Compare multiple letters (different lenders may approve different amounts)

Can You Be Denied After Pre-Approval? YES, if:

- You take on new debt (car loans, credit cards)

- Income changes (job loss, reduced hours, commission drops)

- Credit score drops significantly

- Property appraisal comes in below purchase price

- You make large unexplained deposits (raises money laundering flags)

Pre-Approval Validity: Most letters expire in 60-90 days. To refresh, lenders re-check your credit and income—ensure nothing has changed.

Compare mortgage options with our 15-year vs. 30-year mortgage analysis to choose the right loan term.

Real Success Story: First-Time Buyer Overcomes Credit Concerns

Sarah M., Age 28, Denver, CO

Profile:

- Income: $74,000/year (marketing coordinator)

- Credit score: 668 (limited 3-year history)

- Savings: $19,000

- Monthly debts: $385 student loans + $280 car = $665

Challenge: First-time buyer worried 668 score wasn’t competitive.

Pre-Approval Process:

- Applied with bank, credit union, online lender (within 14 days)

- All three approved within 7-10 days

- Credit union approved $298,000 (conventional, 5% down, 6.65% rate)

- Bank offered 6.95% (0.3% higher)

- Online lender approved $285,000 (stricter DTI interpretation)

Outcome: Chose credit union, purchased $282,000 townhome, closed in 33 days.

Key Lesson: Shopping multiple lenders revealed a $13,000 approval difference and 0.3% rate savings ($73/month, $26,280 over 30 years).

Critical Considerations for 2026 Mortgage Pre-Approval

2026 Interest Rate Environment

As of January 2026, average mortgage rates hover at 6.5%-7.25% depending on credit tier—higher than 2020-2021 but stabilizing from 2023-2024 peaks. According to Federal Reserve policy, rates are expected to remain steady through mid-2026, making this a strategic time for pre-approval.

Non-Traditional Borrower Scenarios

Self-Employed: Lenders average 2 years of net income. Provide comprehensive documentation including profit & loss statements and CPA letters to avoid delays.

Recent Job Change: Same-industry moves with salary increases are viewed positively. Provide offer letters and 30 days of pay stubs.

Low Credit (580-620): FHA loans accept 580 minimums with 3.5% down. Expect higher rates (7.0%-7.5% range) and mandatory mortgage insurance.

Student Loan Debt: Use income-driven repayment plans to lower DTI calculations. Document your actual payment, not the 1% standard calculation.

Security & Privacy Protections

Mortgage pre-approval requires sensitive financial data. Ensure lenders use:

- Bank-level encryption (256-bit SSL)

- Secure document upload portals (not email)

- CFPB compliance for consumer protection

- Equal Credit Opportunity Act adherence (no discrimination)

According to Consumer Financial Protection Bureau guidelines, you have rights to dispute inaccurate denials and request adverse action explanations.

Building financial stability? Our emergency fund calculator helps you plan 3-6 months of expenses before homebuying.

Frequently Asked Questions About Mortgage Pre-Approval

1. How long does mortgage pre-approval take?

Automated decisions: 24-48 hours for W-2 employees. Manual underwriting: 7-14 days for self-employed or complex income. Apply with multiple lenders simultaneously to compare within 45 days.

2. Does mortgage pre-approval hurt your credit score?

Yes, minimally—each hard inquiry drops scores 3-5 points temporarily. Multiple mortgage inquiries within 45 days count as ONE inquiry. Avoid non-mortgage credit during this window.

3. Can you get pre-approved with a 620 credit score?

Yes—620 is the conventional loan minimum. FHA accepts 580 (3.5% down) or 500 (10% down). Lower scores mean 0.5%-1.5% higher interest rates and stricter DTI requirements.

4. What’s the difference between pre-qualification and pre-approval?

Pre-qualification is an estimate based on self-reported information (soft credit check, no verification). Pre-approval verifies income, assets, and credit with documentation—it’s a conditional lender commitment.

5. How long is mortgage pre-approval valid?

Typically 60-90 days due to changing financial circumstances and rate volatility. Refresh requires updated credit check and income verification—ensure nothing has changed.

6. Can you get denied after pre-approval?

Yes—if you take on new debt, lose income, credit score drops, or property appraisal fails. Avoid major financial changes between pre-approval and closing. Lenders re-verify everything before final approval.

7. Should you get pre-approved by multiple lenders?

Absolutely. Rates vary 0.25%-0.75% between lenders. On $300,000, that’s $47-$141/month difference ($16,920-$50,760 over 30 years). Apply with 3-5 within 45 days to minimize credit impact.

8. What documents do you need for mortgage pre-approval?

W-2 employees: 30 days pay stubs, 2 years W-2s and tax returns, 2 months bank statements, government ID. Self-employed: Add business tax returns, profit & loss statements, business bank statements, CPA letter.

9. What credit score do first-time homebuyers need?

Same minimums: 620 conventional, 580 FHA. First-time buyer programs offer down payment assistance and lower requirements. Check state housing finance agencies for local grants.

10. How does self-employment affect pre-approval?

Lenders average your last 2 years of net business income from tax returns. Higher documentation burden (business returns, P&L statements, CPA letter). Timeline: 10-14 days manual underwriting.

11. Can you use gift money for down payment?

Yes—gifts from family are allowed. Required: gift letter (no repayment expectation), proof donor has funds (bank statements), transfer documentation (wire receipt). Lenders verify legitimacy.

12. What’s a good debt-to-income ratio for approval?

36% or below gets best rates. 43-45% is acceptable for conventional. FHA allows 50%. Calculate: (monthly debts + mortgage) ÷ gross monthly income × 100.

Need to reduce debt before buying? Our debt payoff strategies guide provides proven methods to eliminate balances faster.

Important Financial Disclaimer

⚠️ IMPORTANT LEGAL DISCLAIMER

The information provided in this article is for educational and informational purposes only and does not constitute professional financial, legal, or mortgage advice. financeauthorityhub.com and its authors are not licensed mortgage brokers or financial advisors.

Before making any financial decisions, consult with a qualified mortgage professional or financial advisor licensed in your jurisdiction.

Key Disclaimers:

✅ No Guaranteed Approval: Pre-approval estimates do not guarantee final loan approval; lender decisions depend on full financial review, property appraisal, and unchanged circumstances

✅ Market Conditions Change: Interest rates, lending standards, and program requirements are subject to change; information accurate as of January 2026

✅ Individual Results Vary: Credit scores, income, debt, and employment history affect outcomes; examples represent individual experiences, not guaranteed results

✅ Verify Current Information: Always confirm rates, requirements, and program details directly with lenders before applying

✅ No Liability: financeauthorityhub.com assumes no liability for user reliance on this content or resulting financial decisions

✅ Data Accuracy: All statistics verified from authoritative sources as of publication; users should independently verify critical information

All mortgage products carry risk. Borrowers are responsible for repayment regardless of property value changes or income fluctuations.

See our complete Terms of Service and Privacy Policy for legal disclosures.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.