Buy Your First Home 2026: Save $15K+ (Complete First-Time Buyer Guide)

Buying your first home in 2026? Rates are 6.2%, inventory up 8.9%, and new programs expanding access. Learn to evaluate loan options, avoid $15K mistakes, and move from overwhelm to action.

In This Article

Buying your first home is one of the biggest financial decisions you’ll make—and 2026 offers the best conditions in years to make it happen.

Key advantages right now:

- Mortgage rates stabilized at 6.20% (down from 7%+ in 2023)

- Home inventory up 8.9% year-over-year

- New first-time buyer programs expanding access

- Less competition (only 21% of sales go to first-timers)

This guide teaches you how to evaluate options strategically, avoid $15,000-$40,000 mistakes, and move from overwhelm to confident action.

Why 2026 Is Your Best Year to Buy Your First Home

Market Conditions Favor First-Time Buyers

Interest Rates: According to Federal Reserve data, rates are at their lowest in 2+ years:

| Loan Type | Rate | APR | Monthly Payment ($300K) |

|---|---|---|---|

| 30-Year Conventional | 6.20% | 6.35% | ~$1,799 |

| 15-Year Conventional | 5.57% | 5.75% | ~$2,383 |

| FHA 30-Year | 5.97% | 6.70% | ~$1,946 |

| VA 30-Year | 5.79% | 6.14% | ~$1,737 |

| USDA 30-Year | 5.86% | 6.21% | ~$1,785 |

Bottom line: Every 0.5% rate difference saves $150-$200/month or $54,000-$72,000 over 30 years.

Housing Inventory Is Expanding

Realtor.com reports housing supply is up 8.9% year-over-year, meaning:

✅ More homes to choose from

✅ Less bidding war pressure

✅ Better negotiating position

✅ Fewer first-timers competing (21% market share, down from highs)

Down Payment Programs Expanding

New federal initiatives in 2026 make down payment assistance available to more buyers, especially those earning $45,000-$100,000 annually.

Use our home affordability calculator to see exactly how much house you can afford before shopping.

What Makes This Guide Different

Most guides jump straight to loan recommendations. We don’t.

This guide:

- ✅ Teaches evaluation framework FIRST

- ✅ Shows you demographic routing (not one-size-fits-all)

- ✅ Provides real cost comparisons

- ✅ Gives you 7-step implementation roadmap

- ✅ Includes complete FAQ capturing long-tail questions

How to Evaluate Your Options (Before You Fall in Love)

The 5 Core Features Every Buyer Should Evaluate

1. Down Payment Requirement

How much can you actually put down?

- FHA: 3.5% minimum

- Conventional: 3% minimum

- VA: 0% (military-only)

- USDA: 0% (rural-only)

More down = Lower monthly payment and faster equity building.

Test scenarios with our home affordability calculator

2. Monthly Payment Affordability

Not the lender’s maximum—your comfortable maximum.

Lenders approve based on debt-to-income (43-50% of gross income), but you shouldn’t stretch that far.

Healthy target: 25-30% of gross income toward housing.

Example: $60,000 annual income

- Maximum lender allows: ~$2,150/month (36% of gross)

- Comfortable target: ~$1,500-$1,500/month (30% of gross)

Difference between max and comfortable = $650/month breathing room for life.

3. Qualification Difficulty

How much friction between your finances and approval?

| Credit Score | Impact | Options |

|---|---|---|

| 740+ | Excellent | All loans available; best rates |

| 680-739 | Good | All loans; competitive rates |

| 620-679 | Fair | Conventional tougher; FHA better |

| 580-619 | Poor | FHA only; higher rates |

| <580 | Very Poor | Limited to special programs |

Check your credit score at AnnualCreditReport.com (free, federally mandated).

Our credit score guide explains what your score means for loan qualification.

4. Hidden Costs Clarity

Closing costs typically range 2-6% of loan amount.

On a $300,000 mortgage:

| Cost Category | Typical Range |

|---|---|

| Origination/processing fees | $1,200-$2,500 |

| Appraisal | $400-$600 |

| Title insurance | $500-$1,200 |

| Homeowners insurance (1 year) | $1,200-$2,000 |

| Property taxes (if collected at closing) | Variable |

| PMI/MIP (if applicable) | $2,000-$5,000 |

| Total range | $6,000-$18,000 |

Per HUD guidance, lenders must provide detailed Loan Estimate within 3 days of application.

5. Flexibility for Life Changes

Can you refinance later? What are the costs?

Questions to ask:

- Can I refinance if rates drop? (Most conventional loans: Yes)

- What’s the prepayment penalty? (Most loans: Zero)

- What if my financial situation changes? (DTI went up, income dropped, credit declined?)

Learn how to refinance before you lock your initial terms.

Red Flags: What to Avoid

🚩 Lenders pushing maximum approval amount (“You qualify for $450K, so you should look at that range”)

🚩 Unclear fee discussions (Good lenders provide itemized Loan Estimates within 3 days)

🚩 Credit requirements above 680 for FHA (Other lenders accept 580+)

🚩 Rates that seem “too good to be true” (Shop 3-5 lenders within 14 days; shopping doesn’t hurt your credit)

Quality Signals: Identifying Trustworthy Lenders

✅ Verify NMLS licensing (Nationwide Mortgage Licensing System)

✅ Review FDIC standards for regulation compliance

✅ Read third-party reviews (Bankrate, NerdWallet, Google—look for patterns, not single complaints)

✅ Ask about their process, timeline, and contingency plans

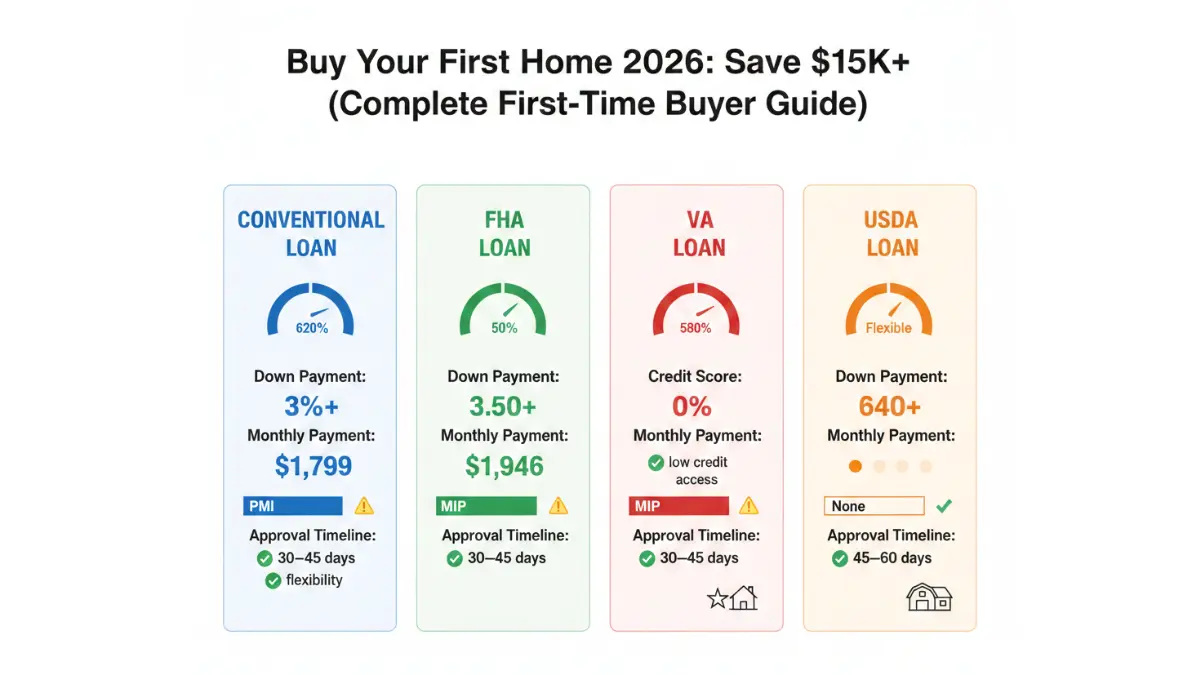

The Best First-Time Home Buyer Loans for 2026

Conventional 30-Year Fixed-Rate Loan

Best For: Creditworthy, stable buyers with no special circumstances

Key Features:

- Minimum 3% down payment

- Fixed rate for 30 years

- PMI required if <20% down (drops when you reach 80% LTV)

- Debt-to-income cap: 43% (up to 49% with compensating factors)

Current Pricing (Jan 26, 2026):

| Item | Value |

|---|---|

| Rate | 6.10% |

| APR | ~6.35% |

| Monthly on $300K | ~$1,799 |

| With $60K down (20%) | No PMI |

| Total interest (30 years) | ~$348,820 |

Real Outcome: Buyer with $60,000 down (20%) on $300,000 home eliminates PMI entirely. Total cost: ~$648,820. Refinance-friendly if rates drop.

Quality Signal: Fannie Mae and Freddie Mac back most conventional loans, ensuring standardized underwriting. Fannie Mae 2026 conforming loan limits: $806,500 in most areas.

Pros:

- Simplest, most familiar

- Good rates for strong credit

- PMI can drop

- No income limits or special eligibility

Cons:

- Requires 620+ FICO

- Higher down payment typical for best rates

- PMI adds cost if <20% down

Processing Time: 30-45 days typical

FHA 30-Year Fixed-Rate Loan

Best For: First-time buyers, lower credit scores (580-619), minimal down payment

FHA loans remove barriers that exclude first-time buyers.

Key Features:

- Minimum 3.5% down payment

- Accepts credit scores as low as 580 FICO

- Mortgage Insurance Premium (MIP): 1.75% upfront + 0.80% annual

- MIP mandatory for life of loan if <10% down; 11 years if ≥10%

- Debt-to-income cap: 43% (up to 50% with compensating factors)

Current Pricing (Jan 26, 2026):

| Item | Value |

|---|---|

| Rate | 5.97% |

| APR | ~6.70% |

| Monthly on $300K | ~$1,946 |

| With $10.5K down (3.5%) | Includes MIP |

| Total interest (30 years) | ~$401,440 |

| Total MIP cost | ~$25,000-$30,000 |

Real Outcome: Buyer with $30,000 down (10%) on $300,000. MIP drops after 11 years, saving $80-$120/month long-term.

Quality Signal: HUD officially administers FHA loans. All lenders meet strict federal standards. Credit flexibility is intentional—government-backed to expand homeownership.

Pros:

- Accessible to lower credit (580+)

- Minimal down payment (3.5%)

- Rates often competitive

- Larger DTI allowance (50%)

Cons:

- Mandatory MIP for life (if <10% down)

- MIP doesn’t disappear automatically

- Requires primary residence

Processing Time: 30-45 days typical

VA Loan

Best For: Military, veterans, National Guard members, surviving spouses

If you’re military-connected, a VA loan is likely your best financial choice.

Key Features:

- Zero down payment required

- No mortgage insurance (VA Funding Fee 2.3% for first-time use, waivable with disability rating)

- Flexible credit score (no official minimum; lenders typically require 580+)

- Debt-to-income: 41% typical (up to 60%+ with compensating factors)

- Unlimited loan limits if you have full entitlement

Current Pricing (Jan 26, 2026):

| Item | Value |

|---|---|

| Rate | 5.79% |

| APR | ~6.14% |

| Monthly on $300K | ~$1,737 |

| Down payment required | $0 |

| Mortgage insurance | $0/month |

| Total interest (30 years) | ~$325,320 |

Real Outcome: Full entitlement buyer saves $30,000-$50,000 vs. FHA or conventional (zero down + lower rates + no insurance).

Quality Signal: VA.gov officially backs all VA loans. Federal guarantee protects lenders, enabling zero-down mortgages. Verification is strict.

Pros:

- Zero down payment

- Best rates in market

- No PMI ever

- Flexible credit

- Excellent long-term value

Cons:

- Eligibility limited to military-connected

- Funding Fee is upfront cost (can roll into loan)

Processing Time: 30-45 days typical

Verify your VA eligibility

USDA Rural Development Loan

Best For: Rural/suburban buyers, zero down payment, low-to-moderate income

If your first home is outside major metro areas, USDA RD loans offer zero-down financing plus subsidies.

Key Features:

- Zero down payment required

- Property must be in USDA-eligible area (check map)

- No PMI-equivalent; USDA Funding Fee (~1%) included

- Income limits: up to 115% of area median income

- Debt-to-income: 41% typical (up to 43% with compensating factors)

Current Pricing (Jan 26, 2026):

| Item | Value |

|---|---|

| Rate | 5.86% |

| APR | ~6.21% |

| Monthly on $300K | ~$1,785 |

| Down payment required | $0 |

| USDA fee | ~1% (~$3,000) |

| Total interest (30 years) | ~$341,400 |

Real Outcome: Rural buyer earning $50,000 with zero savings qualifies for full loan without down payment. Saves $30,000 in down payment + no PMI.

Quality Signal: USDA Rural Development officially administers program. All loans meet federal standards. Property eligibility strictly verified.

Pros:

- Zero down

- Rural property access

- No PMI

- Competitive rates

- Income flexibility

Cons:

- Geographic limitation (rural/suburban only)

- Income caps apply

- Primary residence only

Down Payment Assistance + Conventional Combo

Best For: All first-time buyers, especially $45K-$100K income

This isn’t a single loan type—it’s a strategy combining grants + conventional financing.

How It Works:

- Apply for state/federal down payment assistance ($5K-$25K grants)

- Use grant for down payment or closing costs

- Finance remainder conventionally

- Result: Your own down payment stays in reserves

Real Example:

| Scenario | Without Assistance | With Assistance |

|---|---|---|

| Annual income | $60,000 | $60,000 |

| Savings | $15,000 | $15,000 |

| Down payment | $15,000 (5%) | $10,000 (3.3%) |

| Emergency reserves | $0 | $5,000 |

| Monthly payment | Same | Same |

| Financial cushion | None | Better |

Pros:

- Grants are free money (don’t repay)

- Preserves emergency reserves

- Access conventional benefits

- Programs often available regionally

Cons:

- Eligibility varies by state/income

- Extra application effort

- Some programs have wait times

Which Loan Is Right for YOU?

Loan Comparison Matrix

| Feature | Conventional | FHA | VA | USDA RD |

|---|---|---|---|---|

| Down Payment | 3% min | 3.5% min | 0% | 0% |

| Credit Score | 620+ | 580+ | Flexible | 640+ typical |

| Monthly ($300K) | $1,799 | $1,946 | $1,737 | $1,785 |

| Mortgage Insurance | PMI (drops at 80%) | MIP (lifetime if <10%) | None | None |

| Annual Insurance | $75-$150/mo | $150-$200/mo | $0 | $0 |

| Approval Time | 30-45 days | 30-45 days | 30-45 days | 45-60 days |

| Best For | Good credit | Lower credit | Military | Rural buyers |

| Total Interest (30Y) | $348,820 | $401,440 | $325,320 | $341,400 |

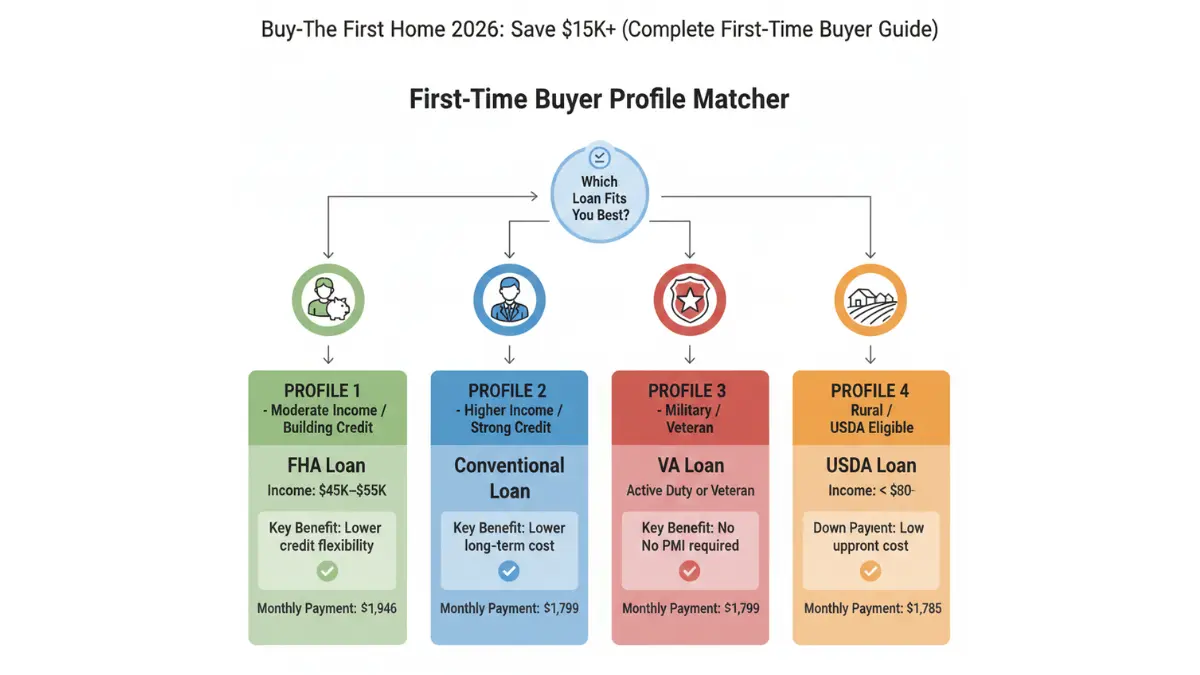

Demographics: Which Loan Matches YOUR Profile?

Profile 1: Modest Income, Lower Credit

You earn: $45K-$65K annually

Credit score: 600

Savings: $15,000

✅ Answer: FHA loan

- 3.5% down ($10,500)

- DTI allowance of 50% = approvable despite modest income

- Alternative: If property is rural, USDA saves MIP costs

Profile 2: Strong Income & Credit

You earn: $85K-$120K annually

Credit score: 680+

Savings: $30K-$50K

✅ Answer: Conventional 30-year

- Put 10-20% down → eliminate/minimize PMI

- Strong credit unlocks best rates

- Monthly: $1,750-$1,850 on $300K

- Refinance-friendly if rates drop

Profile 3: Military/Veteran

Status: Military, veteran, or National Guard

✅ Answer: VA loan (full stop)

- Zero down + best rates + no PMI ever

- Even if you have cash, don’t put it down

- Deploy that money to investments or reserves

- Verify eligibility at VA.gov

Profile 4: Rural Buyer

Location: Outside major metro areas

Income: <$80K

✅ Answer: USDA Rural Development loan

- Zero down + rates better than FHA + no MIP

- Property location beats credit score concerns

- Check USDA eligibility first—property must be USDA-designated

Cost-Benefit Analysis ($300K Home)

Scenario: $300,000 home, $30,000 down (10%), 30-year term, January 2026 rates

| Loan Type | Monthly | Total Interest | Total Cost | Winner |

|---|---|---|---|---|

| Conventional | $1,799 | $348,820 | $678,820 | ⭐ Lowest cost |

| FHA | $1,946 | $401,440 | $731,440 | +$52,620 vs Conv |

| VA | $1,737 | $325,320 | $655,320 | ⭐⭐ If eligible |

| USDA RD | $1,785 | $341,400 | $671,400 | 2nd lowest |

Verdict:

- Conventional wins on cost (if you have 620+ credit)

- FHA costs $50K+ more but opens doors for credit-challenged buyers

- VA beats everyone if you’re eligible

- USDA competitive with conventional for rural buyers

⚠️ The “best” choice isn’t cheapest—it’s what you can qualify for AND afford comfortably.

From Decision to Homeowner: 7-Step Implementation Roadmap

According to Freddie Mac’s timeline, the entire process typically spans 60-120 days.

Step 1: Self-Assessment & Financial Readiness

Timeline: 1-2 weeks

What to do:

- Check credit score at AnnualCreditReport.com (free, federally mandated)

- Calculate debt-to-income ratio (total monthly debt ÷ gross income)

- Use our home affordability calculator to test scenarios

- Target: 25-30% of gross income toward housing

Common mistake: Jumping straight to house hunting without knowing budget

Time expectation: 30-60 minutes to gather documents; 1-2 weeks if improving credit

Step 2: Choose Your Loan Type

Timeline: 1 week

What to do:

- Review Section 4 (demographic routing) above

- Determine which loan type matches your situation

- Conventional? FHA? VA? USDA? Down payment assistance combo?

Common mistake: Choosing based on lowest rate alone without understanding total costs and qualification difficulty

Time expectation: 1-2 hours research; 1 week to decide

Step 3: Improve Your Position or Proceed to Preapproval

Timeline: 2-6 months OR immediate

If credit score <620 OR DTI >43%:

Pay down high-interest debt using our strategy

Use debt consolidation calculator to lower DTI

If 620+ credit AND DTI 35-40%:

Skip this step, move to preapproval

Common mistake: Applying for credit cards or car financing during this phase (hard inquiries hurt credit 12 months; new debt increases DTI instantly)

Time expectation: 2-6 months if improving; skip if ready

Step 4: Get Preapproved by 3-5 Lenders

Timeline: 1-2 weeks

What to do:

- Apply with multiple lenders within 14-day window

- Multiple inquiries in 2 weeks = one credit hit (not five)

- Compare rate quotes AND terms

- Per Bankrate’s preapproval guide, this is your ticket to credibility with sellers

What preapproval means:

- Conditional approval

- Rate locked temporarily

- Your financial situation can’t change materially before closing

Common mistake: Accepting first preapproval without shopping (rates vary 0.5-1.0% across lenders = $100-$300+/month difference)

Time expectation: 1-3 days per lender; 1-2 weeks to collect and compare

Step 5: House Hunt & Make an Offer

Timeline: 2-8 weeks (variable)

What to do:

- With preapproval in hand, you’re ready to search

- Per Redfin’s 2026 timeline, house hunting typically takes 2-8 weeks

- Once you find the home, make offer quickly

- Include: earnest money (1-3% of purchase price), contingencies (financing, inspection, appraisal), closing timeline

Common mistake: Falling in love before running the math (budget limit exists for a reason)

Time expectation: 2-8 weeks searching; 1-3 days to negotiate

Step 6: Closing Process—Inspection, Appraisal, Underwriting

Timeline: 30-45 days

What happens:

- Lender orders appraisal (7-14 days)

- You conduct home inspection (48-72 hours + 2-3 days for results)

- Your lender finalizes application and conducts underwriting

- Lender issues “Clear to Close”

- Federal law: receive Closing Disclosure at least 3 business days before closing

Common mistake: Skipping home inspection to speed up (can miss $5K-$50K+ in foundation, roof, HVAC, plumbing issues)

Time expectation: 30-45 days total (longer if issues require renegotiation)

Step 7: Final Walkthrough, Wire Funds, Sign Documents, Get Keys

Timeline: 1-2 days

What happens:

- 48 hours before closing: final walkthrough (verify repairs completed, condition unchanged)

- Closing day: wire down payment funds

- Sign 50+ pages of closing documents (review carefully—legal binding)

- Recording happens same day or next day

- Once recorded, you own home and get keys

Common mistake: Scheduling move for closing morning (recording delays push possession to afternoon/next day)

Time expectation: 1-3 hours walkthrough + 1-2 hours closing; recording within 24 hours

Trust & Security: Protecting Your Data

How Your Financial Data Is Protected

Per CFPB guidance, mortgage lenders must comply with Gramm-Leach-Bliley Act (GLBA) standards:

✅ All digital transmission uses HTTPS encryption (look for padlock icon)

✅ Multi-factor authentication available

✅ Data cannot be shared with third parties without your written consent

At closing: Title company uses bank-level encryption for wire transfer instructions

⚠️ Critical: Verify wire instructions independently—don’t click email links. Call title company’s phone number directly.

Regulatory Oversight & Lender Legitimacy

| Standard | Authority | Details |

|---|---|---|

| Bank deposits insured | FDIC | Up to $250,000 per depositor |

| Loan officer licensed | NMLS | Nationwide Mortgage Licensing System |

| Fair lending | CFPB | No discrimination (race, color, religion, origin, sex, marital status, age, public assistance) |

Before committing: Verify your loan officer’s NMLS registration and complaint history

Transparent Pricing & No Hidden Fees

Federal law requires:

✅ Loan Estimate within 3 days of application

✅ Closing Disclosure 3 days before closing

All fees must be itemized:

- Origination

- Appraisal

- Title insurance

- Homeowners insurance

- Property taxes

- HOA fees (if applicable)

⚠️ If fees increased between estimates: Ask why and negotiate

Realistic Expectations

This guide enables better decisions. It doesn’t guarantee outcomes.

Your behavior determines long-term success:

✅ Make payments on time

✅ Refinance when rates drop

✅ Avoid excessive post-purchase spending

The tool enables success. You drive it.

Frequently Asked Questions

1. What’s the first step to buying my first home?

Check your credit score at AnnualCreditReport.com, calculate your debt-to-income ratio, and use our home affordability calculator to determine your realistic budget.

2. Can I get a mortgage with bad credit (below 620)?

Yes. FHA loans accept credit scores as low as 580 FICO. Expect higher interest rates (0.5-2.0% premium) and manual underwriting. Dispute credit report errors and pay down high-interest debt before applying.

3. How much down payment do I really need?

Conventional: 3% minimum. FHA: 3.5%. VA and USDA: 0%. Larger down payments reduce/eliminate mortgage insurance. Use our mortgage calculator to compare $10K vs. $30K down ($130-$170/month difference on $300K).

4. What’s the difference between FHA, VA, USDA, and conventional loans?

FHA: 3.5% down, accepts lower credit, mandatory mortgage insurance. VA: 0% down, best rates, military-only. USDA: 0% down, rural-only, no insurance. Conventional: 3% down, 620+ credit, PMI drops at 80% LTV.

5. How long does the home buying process take?

Total timeline: 60-120 days typically. Breakdown: preapproval 1-2 weeks, house hunting 2-8 weeks, closing 30-45 days. Longer timelines result from credit issues, inspection complications, or appraisal challenges.

6. What are closing costs, and how much should I budget?

Closing costs = 2-6% of loan amount. On $300,000, expect $6,000-$18,000. Includes origination fees, appraisal, title insurance, homeowners insurance, property taxes, and PMI/MIP if applicable. All itemized in your Closing Disclosure.

7. Can I use my 401(k) or IRA for down payment?

IRA: Withdraw up to $35,000 penalty-free (lifetime aggregate) if you’re a first-time buyer. 401(k): Can borrow against balance but risky—loan becomes due if you leave the job. Consult a tax advisor before accessing retirement savings.

8. What if I get denied for a mortgage?

Understand why: low credit? High DTI? Low income? Each has a fix. Improve credit (3-6 months), reduce debt, or increase income. Reapply in 3-6 months or try a different loan type (FHA often approves where conventional denies).

9. Is now a good time to buy (2026)?

Yes. Rates are stable (~6.2%), inventory is up 8.9% year-over-year, and fewer first-timers are competing. Market conditions favoring first-timers typically persist 1-2 years. If you’re ready, delaying costs more (rent increases, higher prices).

10. What’s PMI, and can I remove it?

PMI protects the lender on conventional loans with <20% down (costs ~$75-$200/month on $300K). Per CFPB guidance, request cancellation at 80% LTV. It automatically disappears at 78% LTV or 15 years.

11. Should I get preapproval or prequalification?

Prequalification: Fast (same-day), soft credit check, not binding—for quick estimates. Preapproval: Takes 1-3 days, hard credit pull (one inquiry), binds lender to rate/amount. Get preapproved before house hunting—sellers take you seriously.

Important Disclaimer

The information provided on financeauthorityhub.com is for educational and informational purposes only and does not constitute professional financial, legal, investment, or tax advice.

financeauthorityhub.com and its authors are not licensed financial advisors, mortgage brokers, or real estate professionals.

Before making any financial decisions, consult with:

✅ Qualified financial advisor

✅ Licensed mortgage lender

✅ Tax professional

✅ Attorney licensed in your jurisdiction

Key Disclaimers

Past performance ≠ future results. Historical rates and market conditions may change. Data accurate at publication (January 2026) becomes outdated as markets evolve.

All financial products carry risk, including loss of principal. Homeownership involves financial obligation, property market risk, and personal liability.

We don’t guarantee outcomes. Loan terms, rates, and payments vary by borrower, lender, market conditions, and loan type. Individual results differ.

Market changes continuously. Information verified at publication may become outdated. Rates fluctuate daily. Program eligibility changes seasonally.

financeauthorityhub.com assumes no liability for your reliance on this content or resulting financial decisions. You’re solely responsible for evaluating applicability to your specific circumstances.

All data verified from authoritative sources (Federal Reserve, HUD, VA.gov, USDA RD, Fannie Mae, etc.). However, independently verify critical information before decisions, as source data may have updated after publication.

Third-party links: External links to government agencies, lenders, calculators, and resources are provided for informational purposes. financeauthorityhub.com doesn’t endorse or guarantee accuracy of third-party content.

See financeauthorityhub.com Terms of Service and Privacy Policy for complete legal disclosures.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.