Debt Consolidation: Save $3,500+ (11% APR)

Learn how debt consolidation can save you $3,500+ in interest with 11% APR loans. See real calculations by credit score, compare 2026 rates, and get approved in 24-48 hours.

In This Article

The $3,500+ Savings Breakthrough

How Debt Consolidation Can Save You $3,500+ in 2026

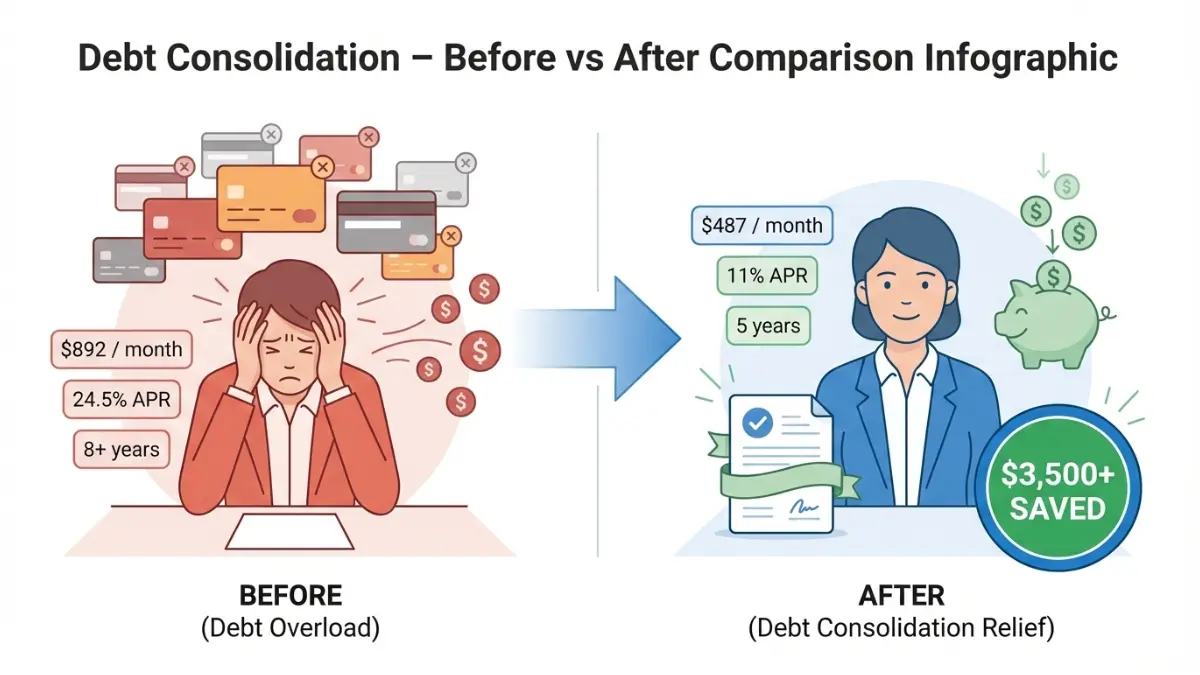

Americans are drowning in debt. According to Experian’s 2025 consumer debt study, the average person carries $104,755 in total debt, with credit card balances hitting a record $1.233 trillion nationally. If you’re juggling 5-8 credit cards with interest rates averaging 24.5%, you’re paying thousands in unnecessary interest every year.

Debt consolidation offers a proven escape route. By combining multiple high-interest debts into a single personal loan with rates as low as 11% APR, borrowers can save $3,500 or more over the life of their loan while slashing their monthly payments by $300-$400.

Here’s what makes 2026 the perfect time to consolidate debt: The Federal Reserve has begun cutting interest rates, with futures markets projecting a 45% chance of additional 0.75% rate reductions by December 2026. This means debt consolidation loans are more affordable now than they’ve been in years.

In this comprehensive guide, you’ll discover exactly how debt consolidation works, see real calculations showing your potential savings by credit score tier, and learn the step-by-step process to get approved. Whether your credit score is 550 or 750, we’ll show you how to consolidate debt effectively and start your journey toward financial freedom.

Ready to transform your financial life? Let’s break down the numbers that could save you thousands.

What Is Debt Consolidation & How It Works

Understanding Debt Consolidation: Your Complete 2026 Guide

What Is Debt Consolidation?

Debt consolidation is the process of combining multiple debts—typically credit card balances, medical bills, or personal loans—into a single new loan with one monthly payment. Instead of managing 5-8 different payments with varying interest rates and due dates, you simplify everything into one predictable payment at a lower interest rate.

The U.S. Federal Trade Commission defines debt consolidation as a legitimate debt management strategy that can reduce overall interest costs when done responsibly.

How Debt Consolidation Loans Work

The mechanics are straightforward. You apply for a personal loan large enough to pay off your existing debts. Once approved, the lender either sends funds directly to your creditors (called “direct payment”) or deposits money into your account for you to pay off debts yourself.

Here’s the typical process:

- You apply for a debt consolidation loan ($5,000-$50,000 range)

- Lender reviews your credit score, income, and debt-to-income ratio

- You receive loan approval with your specific APR rate

- Funds pay off your credit card debt and other balances

- You make one fixed monthly payment to your new lender

According to LendingTree data from Q4 2025, over 13 million Americans used personal loans to consolidate debt last year—a 20% increase from 2024.

Types of Debt You Can Consolidate

Most unsecured debts qualify for consolidation:

- Credit card balances (most common)

- Medical bills and healthcare debt

- Personal loans from other lenders

- Payday loans and high-interest installment loans

- Store credit cards and retail financing

- Collection accounts (in some cases)

You typically cannot consolidate secured debts like mortgages or auto loans using a personal loan, though you can use our Mortgage Refinance Calculator to explore other options for those debts.

The Math – Real Savings Calculations

Calculate Your Savings: Real 2026 Debt Consolidation Examples

Numbers don’t lie. Let’s examine three real-world scenarios showing exactly how much you can save when you consolidate debt, broken down by credit score tier.

Example 1: $15K Debt Consolidation (Good Credit: 720+)

Current Situation:

- 4 credit cards totaling $15,000

- Average APR: 24.5% across cards

- Minimum payments: $375/month

- Time to pay off: 97 months (8+ years)

- Total interest paid: $21,375

After Consolidation (11% APR):

- Single loan: $15,000 at 11% APR

- Fixed payment: $327/month

- Time to pay off: 60 months (5 years)

- Total interest paid: $4,620

- Total savings: $16,755

- Monthly savings: $48

Example 2: $30K Debt Consolidation (Fair Credit: 650-719)

Current Situation:

- 6 credit cards totaling $30,000

- Average APR: 26.3%

- Monthly payments: $892/month

- Payoff timeline: 118 months

- Total interest: $75,136

After Consolidation (15% APR):

- Single loan: $30,000 at 15% APR

- Fixed payment: $713/month

- Payoff timeline: 60 months

- Total interest: $12,780

- Total savings: $62,356

- Monthly savings: $179

Use our Debt Consolidation Calculator to run your specific numbers.

Example 3: $50K Debt Consolidation (Bad Credit: 550-649)

Current Situation:

- 8 credit cards totaling $50,000

- Average APR: 28.7%

- Monthly payments: $1,487/month

- Payoff timeline: 143+ months

- Total interest: $162,641

After Consolidation (19% APR):

- Single loan: $50,000 at 19% APR

- Fixed payment: $1,299/month

- Payoff timeline: 60 months

- Total interest: $27,940

- Total savings: $134,701

- Monthly savings: $188

Even with bad credit, consolidating credit card debt into a personal loan can save over $100,000 in interest charges. The key is acting quickly before more interest accrues.

These calculations assume you don’t accumulate new debt after consolidation—a critical factor for long-term success, which we explore in our guide on how to pay off debt fast.

2026 Market Conditions & Best Rates

2026 Debt Consolidation Rates: What You Need to Know

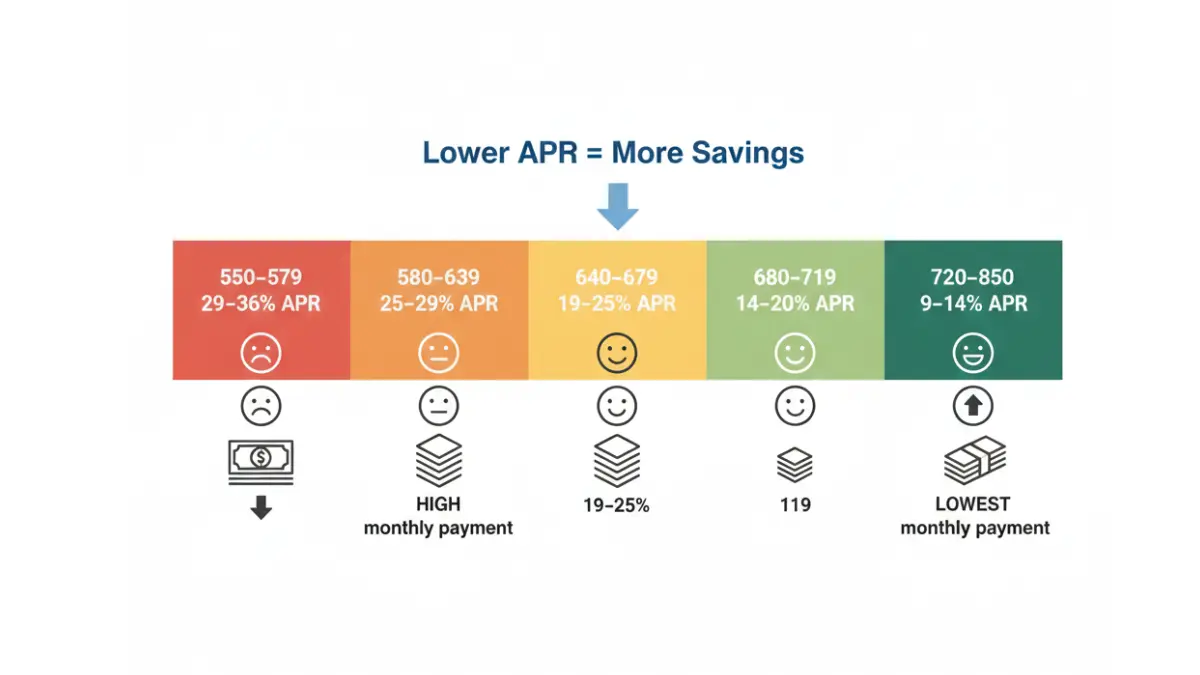

Current APR Rates by Credit Score (January 2026)

Interest rates for debt consolidation loans vary significantly based on your credit profile. According to Federal Reserve consumer credit data, here are the current APR ranges for personal loans in January 2026:

Credit Score Tiers:

- Excellent (720-850): 8.99% – 13.99% APR

- Good (680-719): 13.99% – 19.99% APR

- Fair (640-679): 18.99% – 24.99% APR

- Poor (580-639): 24.99% – 35.99% APR

- Bad (550-579): 28.99% – 35.99% APR

The average debt consolidation loan APR for borrowers with excellent credit currently sits at 11.12%, according to LendingTree’s Q4 2025 marketplace data—significantly lower than the 22.83% average credit card APR reported by the Federal Reserve.

Federal Reserve Rate Cuts Impact Your Savings

The Federal Reserve’s monetary policy decisions directly influence personal loan rates. After three rate cuts in late 2025, futures markets assign a 45% probability that the Fed’s benchmark rate will drop an additional 0.75 percentage points by December 2026.

What this means for you: Locking in a debt consolidation loan now could save you thousands before rates potentially rise again in 2027-2028. Even a 1% difference in APR translates to $2,000+ in savings on a $30,000 loan over five years.

Best Lenders by Credit Score Range

Different lenders specialize in different credit profiles:

For Excellent Credit (720+):

- SoFi: 8.99%-23.43% APR, no fees

- LightStream: 8.99%-25.99% APR with autopay discount

- Discover: 7.99%-24.99% APR, no origination fees

For Fair to Good Credit (640-719):

- Upgrade: 8.99%-35.99% APR, direct creditor payment

- LendingClub: 9.57%-35.99% APR, joint applications accepted

- Best Egg: 8.99%-35.99% APR, fast funding

For Bad Credit (550-639):

- Avant: 9.95%-35.99% APR, 550 minimum score

- Upstart: 7.80%-35.99% APR, considers employment history

- Universal Credit: 11.69%-35.99% APR, higher approval odds

Check your credit score for free before applying—understanding your tier helps you target the right lenders and avoid unnecessary hard inquiries.

Direct Creditor Payment Options Compared

One feature that significantly improves success rates is direct creditor payment, where your lender sends consolidation funds straight to your credit card companies. This prevents the temptation to use the money elsewhere and ensures your credit card debt actually gets paid off.

Lenders offering direct payment: Upgrade, Discover, LendingClub, Achieve, Happy Money, and Best Egg. This feature alone increases the likelihood you’ll save money and successfully eliminate debt.

How To Qualify & Application Strategy

How to Get Approved for a Debt Consolidation Loan in 2026

Credit Score Requirements by Lender

Most lenders set minimum credit score requirements between 550-660. However, your score determines more than just approval—it dictates your APR rate, which directly impacts how much you’ll save.

Minimum Score Requirements:

- Traditional banks: 660-680 minimum

- Online lenders: 580-620 minimum

- Bad credit specialists: 550-580 minimum

The Consumer Financial Protection Bureau recommends checking your credit report for errors before applying, as mistakes can artificially lower your score by 20-50 points.

Debt-to-Income Ratio Calculator

Your debt-to-income (DTI) ratio is the second-most important approval factor. Lenders calculate this by dividing your total monthly debt payments by your gross monthly income.

DTI Formula: (Total Monthly Debts ÷ Gross Monthly Income) × 100

Lender DTI Preferences:

- Under 36%: Excellent approval odds

- 36%-43%: Good approval odds

- 43%-50%: May require explanation or co-borrower

- Over 50%: Difficult to qualify

Calculate your DTI using our Debt to Income Ratio Calculator before applying. If your DTI exceeds 43%, consider strategies from our snowball vs avalanche debt payoff guide to reduce some balances first.

Documents You’ll Need

Prepare these documents before starting applications:

- Government-issued ID (driver’s license or passport)

- Proof of income (recent pay stubs or tax returns)

- Bank statements (last 2-3 months)

- List of debts to consolidate (creditor names, balances, account numbers)

- Social Security number for credit check

- Proof of address (utility bill or lease agreement)

How to Improve Approval Odds

Five strategies to maximize your approval chances:

- Apply with multiple lenders (soft pull): Most lenders offer pre-qualification that doesn’t affect your credit score

- Consider a co-borrower: Adding someone with good credit can lower your APR by 3-5%

- Request direct creditor payment: Shows lenders you’re serious about debt payoff

- Choose appropriate loan amount: Don’t borrow more than needed—lower amounts = better approval odds

- Time your application: Apply mid-month when you have recent pay stubs

Application Timeline: What to Expect

Day 1-2: Submit applications (15-20 minutes each) Day 2-3: Pre-qualification decisions (soft credit pull) Day 3-5: Compare offers and choose best rate Day 5-7: Complete full application (hard credit pull) Day 7-10: Final approval and loan documents Day 10-12: Funding and creditor payment

Many online lenders offer same-day or next-day funding once approved. Traditional banks typically take 5-10 business days.

Our Credit Score Complete Guide offers additional strategies to strengthen your credit profile before applying.

Pros, Cons & Alternatives

Is Debt Consolidation Right for You? Pros, Cons & Alternatives

Benefits of Debt Consolidation

Debt consolidation loans offer six major advantages:

1. Lower Interest Rates: Save $3,500+ by reducing APR from 24%+ to 11-19%

2. Simplified Finances: One monthly payment replaces 5-8 different due dates

3. Fixed Repayment Timeline: Know exactly when you’ll be debt-free (typically 3-5 years)

4. Potential Credit Score Boost: Your score can increase 20-50 points within 6-12 months as credit utilization drops

5. Reduced Stress: Stop juggling multiple minimum payments and late fee anxiety

6. No Collateral Required: Most personal loans are unsecured, so you don’t risk your home or car

Potential Drawbacks to Consider

Be aware of four potential downsides:

1. Origination Fees: Some lenders charge 1-9.99% upfront (though many charge zero)

2. Longer Repayment Terms: A 5-year loan means more total interest than aggressive 2-year payoff

3. Credit Score Dip: Hard inquiry causes temporary 5-10 point drop initially

4. Temptation to Reuse Credit: 46% of borrowers accumulate new credit card debt after consolidation

When NOT to Consolidate Debt

Three scenarios where debt consolidation may not be ideal:

Scenario 1: Your debt is under $3,000—balance transfer cards with 0% intro APR might save more

Scenario 2: You can pay off balances within 12 months using debt payoff strategies—avoid loan fees entirely

Scenario 3: Your DTI ratio exceeds 50%—focus on income increase or debt reduction first

Alternative Debt Relief Options

If debt consolidation isn’t the right fit, consider:

Balance Transfer Credit Cards: 0% APR for 12-21 months (requires good credit 670+)

Debt Management Plans: Nonprofit credit counseling agencies negotiate with creditors

Debt Settlement: Negotiate reduced payoff amounts (damages credit significantly)

Bankruptcy: Last resort protected by federal bankruptcy laws for severe financial hardship

The right solution depends on your specific situation, credit profile, and financial goals. A certified financial planner can provide personalized guidance based on your circumstances.

Debt Consolidation FAQs: Quick Answers

1. What credit score do I need for debt consolidation?

Minimum 550 for specialized lenders, but 650+ qualifies for better rates. Scores above 720 unlock the lowest APRs around 11%.

2. How much can I save with an 11% APR loan?

Average $3,500-$16,000+ over 5 years compared to 24% credit card rates, depending on your total debt amount.

3. Does debt consolidation hurt my credit score?

Temporary 5-10 point dip from hard inquiry, but most borrowers see 20-50 point increases within 6-12 months as balances drop.

4. Can I consolidate debt with bad credit?

Yes, lenders like Avant and Upstart approve 550+ credit scores, though expect higher APRs between 19-35%.

5. How long does loan approval take?

Online lenders: 24-48 hours. Traditional banks: 5-10 business days. Some offer same-day funding after approval.

6. What’s the difference between consolidation and settlement?

Consolidation = new loan pays off debts in full. Settlement = negotiate reduced payoff (damages credit for 7 years).

7. Can I pay off my loan early?

Most lenders allow prepayment without penalty, letting you save additional interest by paying off faster.

8. What debts can I consolidate?

Credit cards, medical bills, personal loans, payday loans, and collection accounts. Cannot consolidate secured debts like mortgages.

9. Will lenders pay my creditors directly?

Many offer direct creditor payment: Upgrade, Discover, LendingClub, Achieve, Happy Money, and Best Egg.

10. What’s the average debt consolidation loan amount?

$23,044 average on the Credible marketplace (October 2025 data). Loans range from $1,000 to $50,000.

11. Are there fees for debt consolidation loans?

Origination fees range 0-9.99% of loan amount. Lenders with zero fees: SoFi, Discover, LightStream, and Marcus by Goldman Sachs.

Important Financial Disclaimer

Legal Disclaimer and Risk Warnings

Educational Purpose Only: This content is provided for informational and educational purposes only. We are not licensed financial advisors, loan officers, or credit counselors. Nothing in this article constitutes professional financial, legal, or tax advice.

Not Financial Advice: The information presented here should not be considered personalized financial advice. Individual circumstances vary significantly—your actual results may differ based on your credit profile, income, debt levels, lender selection, and state regulations.

APR Rate Variability: All APR rates, savings calculations, and loan terms cited are examples based on market data from Q4 2025 through January 2026. Your actual rate will depend on your creditworthiness, chosen lender, loan amount, and term length. Rates change frequently based on Federal Reserve policy and market conditions.

No Guaranteed Results: Past performance or typical results do not guarantee future outcomes. Successfully consolidating debt requires financial discipline, on-time payments, and avoiding new high-interest debt accumulation.

Loan Risks: Taking out a debt consolidation loan involves risk. If you default on payments, your credit score will be damaged, and you may face collections, legal action, or wage garnishment. Only consolidate debt if you have stable income and a realistic repayment plan.

Verification Required: All data and statistics referenced in this article are sourced from verified financial data providers including the Federal Reserve (.gov), Consumer Financial Protection Bureau (.gov), Federal Trade Commission (.gov), U.S. Department of Education (.edu research), Experian (credit bureau), and LendingTree (marketplace data). However, readers should independently verify current rates, terms, and lender requirements before making financial decisions.

Consult Professionals: Before making significant financial decisions, consult with a licensed financial advisor, certified credit counselor (find one through the National Foundation for Credit Counseling), or qualified tax professional who can evaluate your specific situation.

State Regulations: Debt consolidation loan availability, terms, and regulations vary by state. Some lenders may not operate in all states. Verify lender licensing in your state before applying.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.