9 Banks Still Paying Up to 5.00% APY in April 2026 — With Zero Monthly Fees

The national average savings rate is just 0.39%. These 9 FDIC-insured banks pay up to 5.00% APY with zero monthly fees — that’s $230 more per year on every $5,000. Rates and eligibility verified April 2026.

In This Article

The 9 Highest-paying Banks

The Bottom Line: Top 3 Banks Paying Maximum APY Right Now

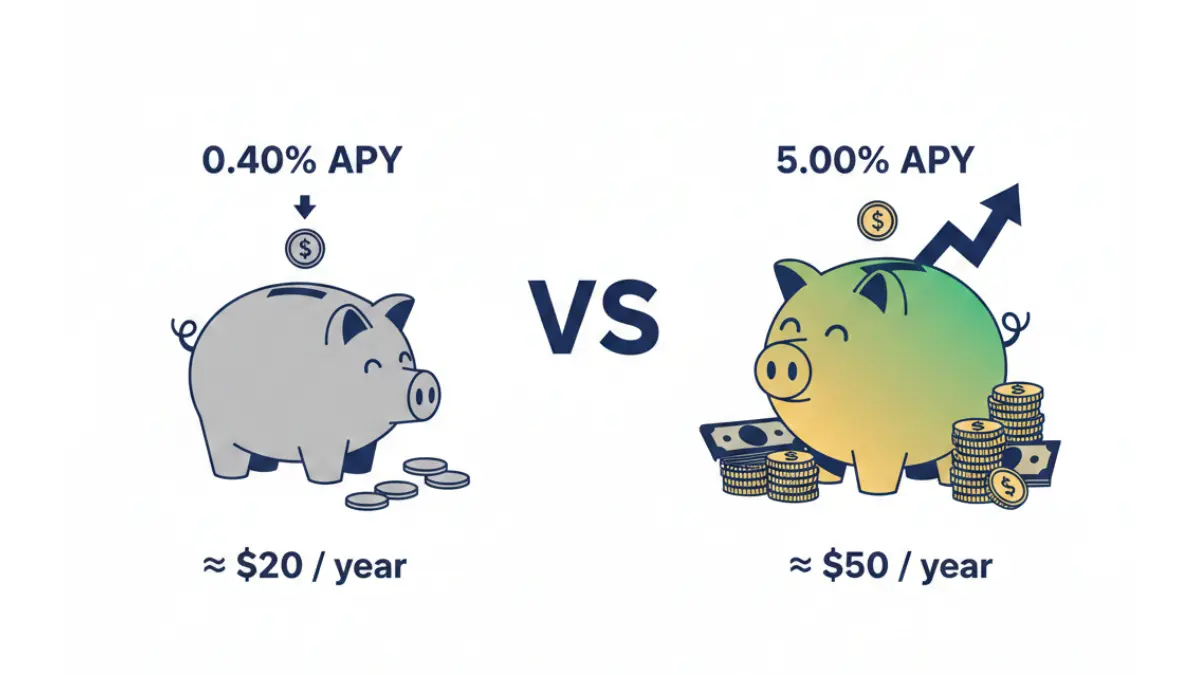

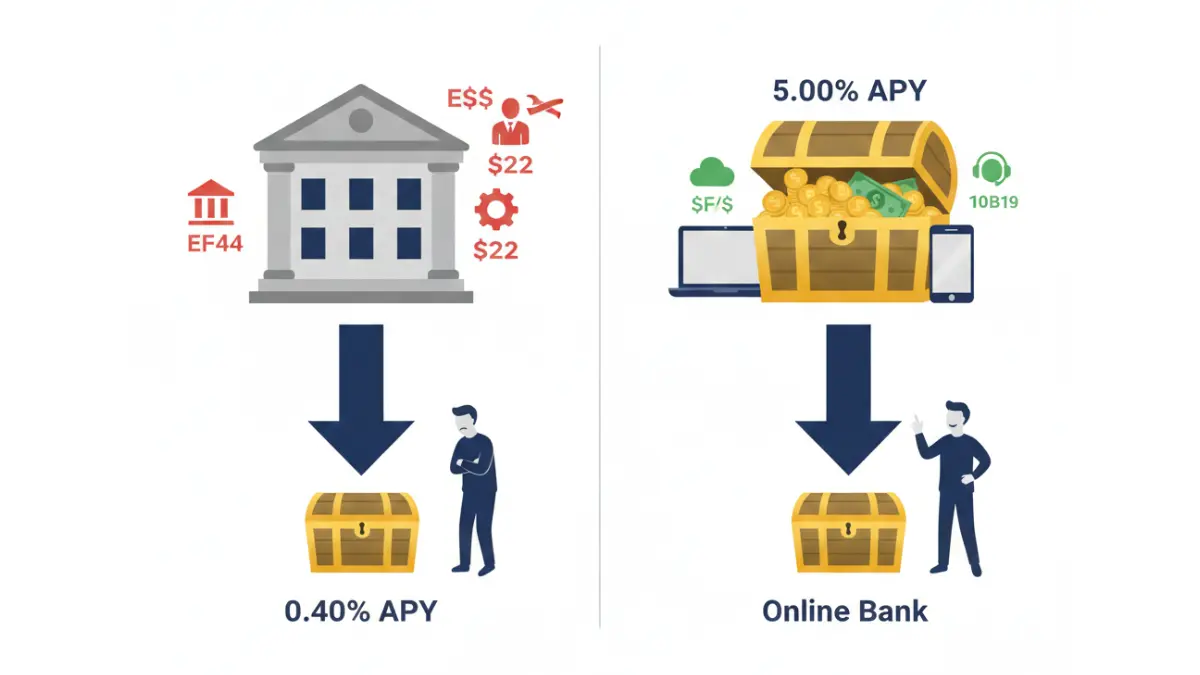

Your traditional bank is paying 0.40% APY while you could be earning 5.00% APY—that’s a difference of $230 per year on just $5,000. Most Americans are unknowingly leaving hundreds of dollars on the table because they’ve never switched to a high-yield savings account.

As of January 22, 2026, nine FDIC-insured banks offer competitive APY rates between 3.90% and 5.00% with zero monthly fees. The Federal Reserve’s current federal funds rate of 3.64% creates the environment where online banks can sustainably offer these yields while maintaining profitability.

Here’s what $5,000 actually earns you:

- Traditional bank (0.40% APY): $20/year

- High-yield bank (5.00% APY): $250/year

- Your gain by switching: $230/year (1,150% increase)

Every bank listed below meets three non-negotiable criteria: FDIC insurance up to $250,000, zero monthly maintenance fees, and transparent rate structures with no hidden charges.

Complete Rankings: 9 Best Banks with $0 Monthly Fees

| Rank | Bank Name | APY Rate | Min Deposit | Monthly Fee | Best For |

|---|---|---|---|---|---|

| 1 | Varo Bank | 5.00%* | $0 | $0 | Maximum rate on first $5K |

| 2 | Newtek Bank | 4.35% | $0 | $0 | Zero qualification requirements |

| 3 | Axos Bank (ONE) | 4.31% | $0 | $0 | Bundled checking + savings |

| 4 | Openbank | 4.20% | $500 | $0 | Digital-first with $500+ |

| 5 | My Banking Direct | 4.02% | $500 | $0 | Mobile-focused savers |

| 6 | Bread Savings | 4.00% | $100 | $0 | Eco-conscious banking |

| 7 | LendingClub LevelUp | 4.00% | $0 | $0 | Monthly deposit habits |

| 8 | CIT Bank Platinum | 3.75% | $5,000 | $0 | Large balance holders |

| 9 | EverBank | 3.90% | $0 | $0 | Regional ATM access |

Varo Bank: 5.00% APY available on balances up to $5,000 when you receive $1,000+ in direct deposits monthly. Balances above $5,000 earn 2.50% APY.

Why These Banks Dominate 2026

Online banks eliminated physical branch networks—the most expensive component of traditional banking. This operational efficiency translates directly into rates that are 10-13 times higher than the FDIC’s reported 0.40% national average for savings accounts.

Each institution carries FDIC insurance protection up to $250,000 per depositor, meaning your money remains federally protected even in unlikely bank failure scenarios. No depositor has lost FDIC-insured funds since the FDIC’s creation in 1933.

The competitive advantage is clear: Online banks pass their cost savings directly to you through higher APY rates while maintaining identical safety standards to traditional brick-and-mortar institutions.

Top 3 Banks Detailed Breakdown

#1 Winner: Varo Bank – 5.00% APY (Maximum Earning Potential)

Varo Bank offers the highest verified consumer APY in January 2026: 5.00% on balances up to $5,000. This rate generates $256 annually on a $5,000 deposit—compared to just $22 from a traditional bank at 0.40% APY.

Qualification Requirements:

The 5.00% rate requires one monthly condition: receive at least $1,000 in direct deposits (employer paycheck, Social Security, pension) and maintain positive balances in both Varo checking and savings accounts by month-end. This is achievable for most employed individuals and creates a compelling reason to consolidate your banking relationship.

The Real Earnings:

For W-2 employees with direct deposit capability, Varo’s checking account (offering 0.25% APY) plus their savings account creates a comprehensive banking ecosystem. On a $5,000 balance meeting qualification requirements, you earn $256 in year-one interest. The second tier for balances exceeding $5,000 drops to 2.50% APY—still competitive with most alternatives.

FDIC Protection:

Varo Bank is FDIC-insured, protecting deposits up to $250,000 per person. The bank uses 256-bit encryption for all digital transactions, matching enterprise-grade security standards.

Unique Advantage:

Varo’s mobile app includes integrated tax-filing capabilities, allowing you to e-file federal returns through their interface and potentially receive refunds up to five days earlier when deposited directly into your Varo account. This positions Varo as more than a savings account—it’s a comprehensive financial management platform.

If you’re building an emergency fund strategy, Varo’s 5.00% rate maximizes growth on your safety net while maintaining instant accessibility.

#2 Runner-Up: Newtek Bank – 4.35% APY (Zero Requirements)

Newtek Bank’s personal high-yield savings account delivers 4.35% APY with absolutely no qualifying conditions—no minimum balance, no direct deposit requirement, no maintenance hurdles. This simplicity makes it ideal for savers prioritizing ease over maximum rate optimization.

The Earnings Comparison:

At 4.35% APY, your $5,000 earns $217 annually—$39 less than Varo’s top rate but without any strings attached. For savers who value straightforward banking, this $39 annual difference becomes negligible against the convenience of zero qualification requirements.

Account Opening Speed:

Newtek claims account opening takes as little as two minutes online with zero initial deposit required. This means you can open and fund the account with exactly the amount you want to save—no forced minimum deposits eating into funds allocated elsewhere in your monthly budget.

FDIC Insurance:

Like all banks in this guide, Newtek is FDIC-insured. Your savings account deposits receive federal protection up to the standard $250,000 limit per depositor.

Why It Ranks #2:

While 4.35% trails Varo’s 5.00%, the elimination of qualification requirements makes Newtek the optimal choice for most savers. If you don’t have direct deposit access or prefer not to maintain minimum deposit requirements, this becomes your best high-yield option.

#3 Third Place: Axos Bank (AXOS ONE) – 4.31% APY (Bundled Banking)

Axos Bank’s AXOS ONE bundle combines checking and savings in a single account structure, offering 4.31% APY on savings and 0.51% APY on checking. The rates become accessible through two different qualification paths, providing flexibility for different financial situations.

Dual Qualification Options:

You can earn the boosted 4.31% rate through either:

Path 1: Receive $1,500+ in monthly direct deposits while maintaining a $1,500+ average daily balance

Path 2: Deposit $5,000+ monthly while maintaining a $5,000+ average daily balance

This dual-path approach accommodates different income structures—whether you’re a salaried employee, freelancer, or retiree with pension deposits.

Bundled Benefits:

Axos includes both checking and savings in the AXOS ONE product, eliminating the need to manage separate accounts at different institutions. Early payday access (up to 2 days faster than traditional banks) becomes available for direct deposits, giving you quicker access to your paycheck.

Annual Earnings:

At 4.31% APY on $5,000, you’d earn $215 annually—competitive with Newtek and just $41 behind Varo’s top tier. For savers who prefer consolidated banking relationships, this minor rate difference often becomes worthwhile.

Integration Advantage:

The bundled checking and savings structure works particularly well when paired with automated savings calculator strategies—set up automatic transfers from checking to savings on payday to consistently build wealth without manual intervention.

Complete Bank Comparison & Decision Matrix

Banks 4-9: Detailed Feature Analysis

Openbank (4.20% APY) requires a $500 minimum deposit to open but maintains no balance requirements thereafter. As a Santander digital subsidiary, Openbank focuses on streamlined digital banking with a single product offering: their high-yield savings account. This simplicity appeals to savers who don’t need multiple account types or complex financial products.

The $500 minimum makes this accessible to most savers while filtering out accounts that would generate minimal interest (under $21 annually). For context, $500 at 4.20% APY earns $21 in year one—meaningful returns on a modest balance.

My Banking Direct (4.02% APY) positions itself as a mobile-first online bank with a $500 minimum deposit requirement. The bank’s aggressive marketing targets mobile-app-first customers who rarely access desktop banking interfaces. Daily interest compounding means earnings grow faster than monthly or annual compounding alternatives—a $10,000 balance earns approximately $3.30 more annually through daily versus monthly compounding.

Bread Savings (4.00% APY) markets itself as an eco-conscious online bank with a $100 minimum deposit. The bank allocates portions of profits toward environmental initiatives, appealing to sustainability-focused savers who want their banking choices to align with personal values. All accounts include unlimited transactions and transfers without the traditional 6-per-month savings account restrictions that existed under old Regulation D rules.

The $100 minimum makes this one of the most accessible options for savers just beginning their emergency fund journey—you can start with $100 and build through consistent monthly deposits.

LendingClub LevelUp (4.00% APY) requires regular monthly deposits to maximize benefits. The savings structure rewards consistency—customers who make monthly deposits earn the featured 4.00% rate. Those without monthly deposit habits see significantly lower rates (approximately 0.50% APY).

This account works best for savers committed to automated savings strategies, where paychecks automatically route a percentage to savings before you’re tempted to spend. Pair this with a 50/30/20 budget approach to ensure consistent monthly contributions.

CIT Bank Platinum Savings (3.75% APY) requires a $5,000 minimum balance to earn the featured APY. Balances below $5,000 earn dramatically lower rates (approximately 0.50% APY), making this account unsuitable for savers with smaller amounts. This creates a clear threshold: if you can’t maintain $5,000 consistently, choose a different bank.

For savers with $5,000+, CIT offers competitive rates plus excellent mobile banking tools including savings goal tracking, automated transfers, and spending insights. The bank’s longevity (established 1908) provides traditional banking stability with modern digital features.

EverBank (3.90% APY) distinguishes itself with a national ATM network in Florida and California, providing physical cash access in specific geographic regions. For savers living in these states, EverBank offers a rare combination of high APY with regional ATM convenience without monthly fees.

No minimum deposit is required, making this accessible to all balance levels. The 3.90% APY trails top competitors by 0.10-1.10%, but the ATM access provides tangible value for those needing occasional cash withdrawals without fees.

“Which Bank Is RIGHT FOR YOU?” Decision Framework

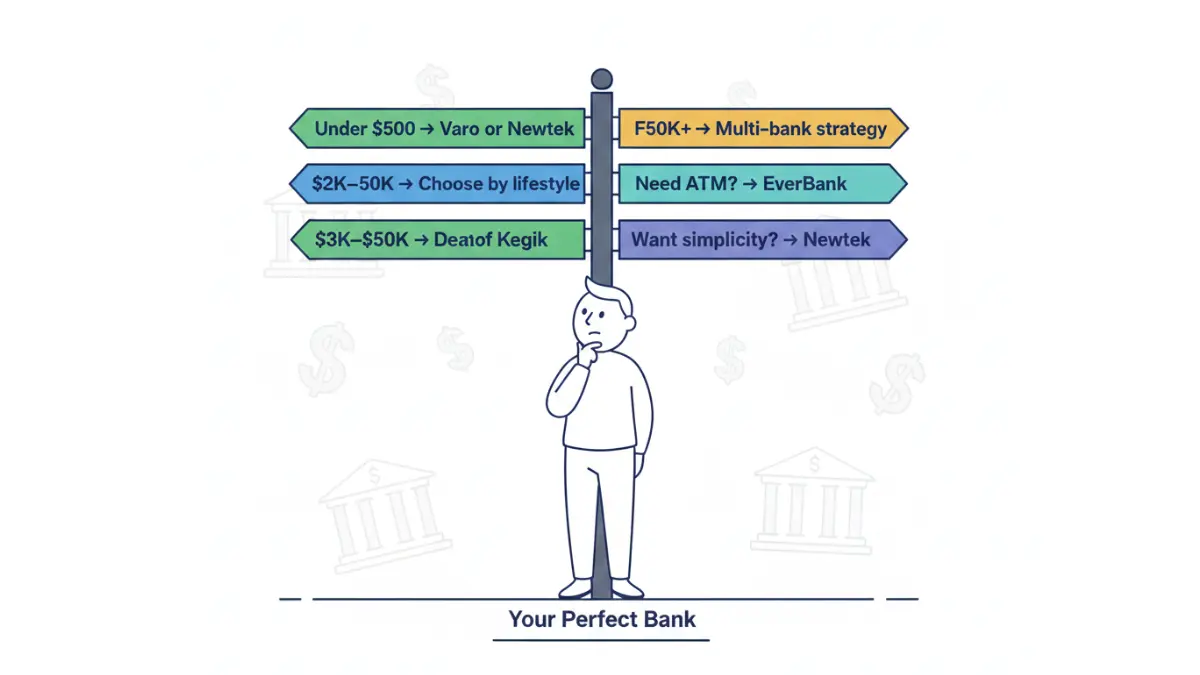

If you have less than $500 to deposit:

Choose Varo Bank (if you have direct deposit) or Newtek Bank (for absolute simplicity). Both have $0 minimums and deliver competitive rates regardless of balance size.

If you have $500-$4,999:

Newtek Bank wins here due to zero minimums and competitive 4.35% APY across all balance tiers. You avoid the complexity of qualification requirements while earning near-maximum rates.

If you have $5,000-$50,000:

Choose based on your lifestyle:

- Varo Bank (5.00%) if you have direct deposit and want maximum returns

- Axos Bank (4.31%) if you prefer bundled checking + savings convenience

- Newtek Bank (4.35%) if you want zero requirements and consistent rates

For this balance range, consider using our compound interest calculator to visualize how different APY rates impact your long-term wealth accumulation.

If you have $50,000+:

Axos Bank or Newtek Bank maintain consistent high rates across all balance tiers without the rate reductions that plague traditional banks (which often penalize large savers with lower rates on balances exceeding $100,000).

For balances exceeding $250,000, consider splitting across multiple banks to maximize FDIC insurance coverage beyond the $250,000-per-bank limit.

If you need physical ATM access:

EverBank is your only option in this list with regional ATM networks covering Florida and California. The 3.90% APY trade-off becomes worthwhile if you regularly need cash access without fees.

If you value ease over optimization:

Newtek Bank removes all qualification hurdles—no direct deposit required, no minimum balance, no bonus conditions. Just open the account, deposit funds, and earn 4.35% APY automatically.

If you want the maximum interest rate:

Varo Bank delivers 5.00% APY—the highest consumer rate available in January 2026. The $1,000 monthly direct deposit requirement is manageable for most employed individuals.

Fee Comparison: Why Zero Fees Matter

All nine banks offer $0 monthly maintenance fees, but fee structures extend beyond monthly charges. Here’s what separates these banks from traditional alternatives:

Overdraft Fees:

Most online banks have eliminated overdraft fees entirely. Traditional banks charge $25-$35 per overdraft incident—these fees can quickly erase months of interest earnings.

ATM Fees:

Except for EverBank’s regional network, most online banks either reimburse ATM fees or partner with fee-free networks like Allpoint (giving you access to 55,000+ fee-free ATMs nationwide).

Wire Transfer Fees:

Online banks typically charge $0-$10 for outgoing domestic wire transfers, versus $15-$30 at traditional banks. For large transfers (home down payments, tuition payments), this saves significant money.

Excessive Withdrawal Penalties:

The Federal Reserve suspended Regulation D enforcement in 2020, eliminating the old 6-withdrawals-per-month limit on savings accounts. Modern banks allow unlimited transfers without penalty—use your savings account as flexibly as needed.

Inactive Account Fees:

Most online banks don’t charge dormancy fees even if you maintain minimal activity. Traditional banks often charge $5-$15 monthly after 6-12 months of inactivity.

If you’re simultaneously paying off credit card debt, these fee savings become even more crucial—every dollar saved on banking fees accelerates your debt payoff timeline.

The Economics Behind High Rates

Why Online Banks Pay 10x More Than Traditional Banks

Traditional banks with thousands of physical branches maintain expensive real estate leases, large employee payrolls, and 24/7 facility management operations. JPMorgan Chase operates 4,700+ branches nationwide—each location represents ongoing rent, utilities, staffing, security, and maintenance costs that must be funded through banking operations.

Online-only banks like Varo, Newtek, and Axos operate entirely through digital channels with no branch infrastructure. This operational efficiency creates a mathematical advantage: lower overhead costs allow banks to offer higher APY rates while maintaining profitability.

The cost comparison:

- Traditional bank: 0.01%-0.40% APY (must fund extensive branch network)

- Online bank: 4.00%-5.00% APY (minimal overhead, maximum customer value)

This isn’t a temporary promotional strategy—it’s a sustainable business model built on operational efficiency.

Tax Implications You Must Understand

Federal Reserve Policy Impact on Your Rates

The Federal Reserve’s current federal funds rate target sits at 3.50%-3.75% as of January 2026. This is the interest rate at which banks lend reserve balances overnight to each other. While high-yield savings account rates don’t directly track the Fed rate one-to-one, they move proportionally in the same direction.

Historical Context:

In mid-2023, the Fed raised rates to 5.25%-5.50%, and high-yield savings account rates exceeded 5.30% across the market. As the Fed cut rates through late 2023 and 2024, HYSA rates declined proportionally. The current 5.00% maximum (Varo Bank) represents slight stabilization from December 2025 levels (4.95%), suggesting market equilibrium.

Why This Matters Now:

The Fed’s next meeting occurs February 18, 2026. According to recent Fed meeting minutes, further rate cuts remain possible if inflation continues moderating toward the 2% target. If the Fed cuts rates by 0.25%-0.50%, high-yield savings account rates will decline within 2-4 weeks.

Strategic Implication:

Opening a high-yield account today at 4.00%+ makes financial sense versus waiting. Rates can only decline or stabilize from current levels—they’re unlikely to rise significantly while the Fed maintains a rate-cutting posture. Lock in today’s competitive rates before they fall.

Understanding this rate environment becomes even more critical when you’re managing multiple financial priorities like debt consolidation strategies or retirement planning—higher savings rates provide flexibility across your entire financial plan.

FDIC Insurance: Your Safety Net

Every bank in this guide carries FDIC insurance protection, meaning your deposits are protected up to $250,000 per depositor, per insured bank, per ownership category.

This isn’t marketing language—it’s a government-backed guarantee. If a bank fails (which is extremely rare), the FDIC reimburses depositors. Since the FDIC’s creation in 1933, no depositor has lost insured funds in a bank failure.

Coverage Limits Explained:

Individual Accounts: $250,000 per person per bank

Joint Accounts: $500,000 per couple per bank ($250,000 per person)

Trust Accounts: Up to $250,000 per beneficiary

Retirement Accounts (IRA): $250,000 per person per bank

Strategic Coverage for Large Balances:

For balances exceeding $250,000, open accounts at multiple FDIC-insured banks. A married couple could deposit $500,000 at each institution ($250,000 per spouse) with full insurance protection. Use the FDIC’s Electronic Deposit Insurance Estimator to calculate your exact coverage across multiple accounts and ownership structures.

Maximize Your Earnings

Step-by-Step Account Opening Process

Before Opening:

Visit the bank’s official website and screenshot the current APY rate you see displayed. Rates change frequently—documentation protects you if there’s any dispute about the rate you were promised.

Step 1 – Gather Required Documents

- Government-issued photo ID (driver’s license, passport, or state ID)

- Social Security Number (for identity verification and tax reporting)

- Proof of current address (utility bill, lease agreement, or bank statement from last 60 days)

- Contact phone number and email address

- Existing bank account details (for funding via ACH transfer)

Step 2 – Complete Online Application

All nine banks in this guide offer 100% online account opening. The process typically takes 5-15 minutes and most banks provide instant account number assignment upon approval. You’ll create login credentials and security questions during this step.

Step 3 – Verify Your Identity

Banks perform automated identity verification (KYC—Know Your Customer compliance) as required by federal law. According to the Consumer Financial Protection Bureau’s account opening guidelines, banks must verify your identity before activation.

Some institutions require additional verification via text message or email confirmation codes. Rarely, banks may call to confirm identity for accounts they couldn’t automatically verify.

Step 4 – Make Your Initial Deposit

Funding options include:

- ACH transfer from your existing checking account (1-3 business days, $0 fee)

- Wire transfer from another bank (same-day, typically $15-30 fee)

- Mobile check deposit via app where available (1-2 business days)

Initial deposit requirements range from $0 to $5,000 depending on the bank you’ve selected.

Step 5 – Establish Automatic Deposits (If Qualifying for Bonus Rates)

For Varo: Set up direct deposit of at least $1,000/month from your employer through your HR/payroll department

For Axos: Schedule automatic transfers of $1,500-$5,000 monthly to maintain boosted rates

For Others: No requirement, but maintain a positive balance to avoid potential inactivity fees

Use our budget calculator to determine how much you can comfortably save each month without straining your cash flow.

Real-World Earnings Scenarios

Understanding compound interest transforms how savers approach their finances. Here’s the actual financial impact across different timeframes:

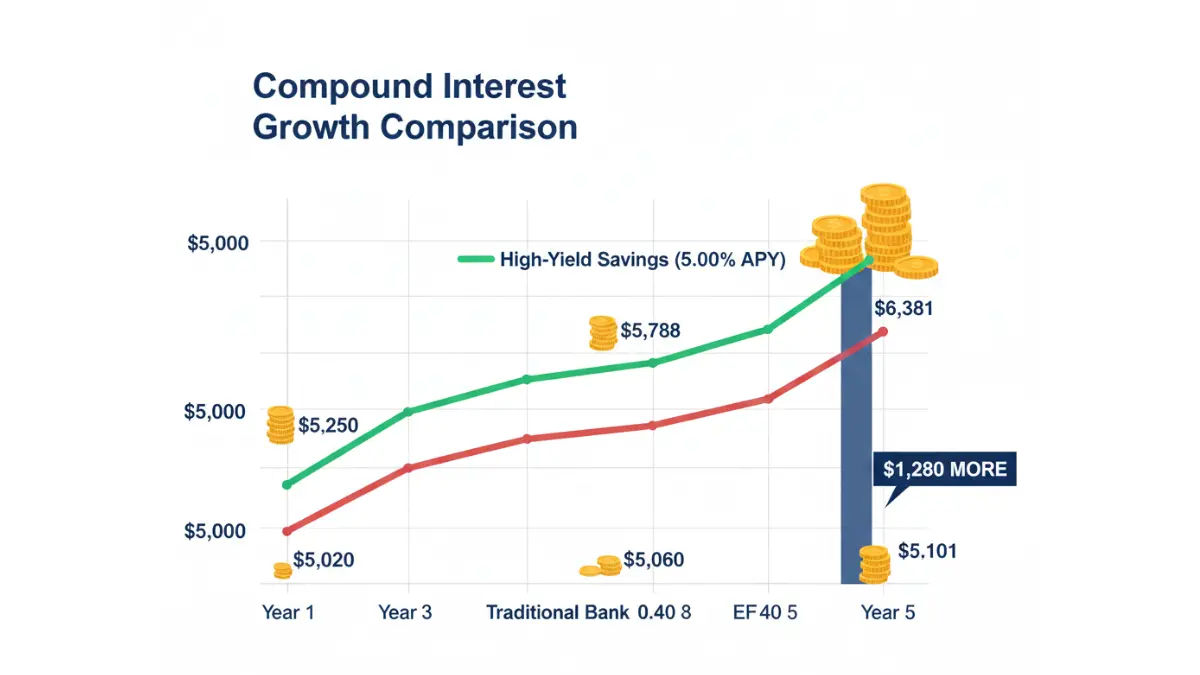

Scenario 1: $5,000 Deposit at 5.00% APY (Varo Bank)

- Year 1: $5,250 (earned $250)

- Year 2: $5,513 (earned $263—interest compounds on interest)

- Year 5: $6,381 (earned $1,381 total)

Scenario 2: $5,000 Deposit at 0.40% APY (Traditional Bank)

- Year 1: $5,020 (earned $20)

- Year 2: $5,040 (earned $20 more)

- Year 5: $5,101 (earned $101 total)

The 5-Year Difference: The high-yield account has $1,280 more than the traditional bank account. That’s real money you could allocate toward paying off debt faster, building an emergency fund, or investing for retirement.

Scenario 3: $10,000 Deposit at 4.35% APY (Newtek Bank)

- Year 1: $10,435 (earned $435)

- Year 2: $10,889 (earned $454—compounding effect accelerates)

- Year 3: $11,362 (earned $473)

- 5-Year Total: $12,396 (earned $2,396 in interest)

For comparison, that same $10,000 at 0.40% APY earns just $202 over 5 years—a difference of $2,194 by simply choosing a high-yield account.

Tax Implications You Must Understand

Interest earned in savings accounts is taxable ordinary income, unlike retirement account interest which may be tax-deferred. High-yield savings account interest is subject to federal income tax in the year earned.

How Banks Report Your Interest:

At year-end, your bank sends you Form 1099-INT reporting total interest earned. The IRS receives an identical copy simultaneously. You must report this interest on your federal tax return.

IRS Reporting Threshold:

According to IRS Publication 550 on investment income, if your interest income reaches $10 or more, the bank must send Form 1099-INT. In practice, banks typically send this form when interest exceeds even $1 to ensure comprehensive reporting.

Tax Rate Impact by Bracket:

Your interest is taxed at your ordinary income tax rate (not the preferential capital gains rate). Here’s what that means:

| Tax Bracket | Interest Earned | Federal Tax Owed | After-Tax Earnings |

|---|---|---|---|

| 12% | $250 | $30 | $220 |

| 22% | $250 | $55 | $195 |

| 24% | $250 | $60 | $190 |

| 32% | $250 | $80 | $170 |

Even after taxes, earning $190-$220 (net) dramatically beats the $20 pre-tax earnings from traditional banks. Plus, state income taxes may apply depending on your residence.

Tax Planning Strategy:

If your high-yield savings account earnings approach $1,000+ annually, set aside approximately 25-30% for federal and state taxes. Don’t treat interest as “free money”—account for tax liability in your overall budget planning to avoid surprises at tax time.

For high earners in the 32%+ tax bracket with substantial savings, consult a tax professional about tax-equivalent yields and whether tax-advantaged alternatives (municipal bonds, retirement accounts) make more sense for portions of your savings.

Frequently Asked Questions

11 Critical Questions About High-Yield Savings Accounts

1: Can I Really Earn 5% on Savings in 2026?

Yes. Varo Bank currently offers 5.00% APY on balances up to $5,000 when you receive $1,000+ in monthly direct deposits (verified January 22, 2026). Even without direct deposit, Newtek Bank pays 4.35% APY with zero requirements. These rates are real, verified, and available to any U.S. resident with a Social Security Number.

2: What’s the Difference Between APY and APR?

APY (Annual Percentage Yield) includes compound interest effects throughout the year—it’s what you earn on savings accounts. APR (Annual Percentage Rate) shows the annual rate without compounding effects—it’s what you pay on loans. For savings accounts, always compare APY to APY. For loans, compare APR to APR.

3: Are These Banks Really FDIC Insured?

Yes, all nine banks are FDIC-insured member institutions. This means your deposits up to $250,000 per person are protected by federal insurance. Even if a bank fails, your money is safe and will be made available within 2 business days.

4: Will These $0 Monthly Fees Stay Forever?

Most online banks guarantee zero monthly fees as a core competitive feature. However, fees can technically change with advance notice. Review your account terms annually. If a bank adds fees, the abundance of no-fee alternatives means you can easily switch to a competitor without losing money.

5: How Quickly Can I Access My Money?

ACH transfers to external linked bank accounts take 1-3 business days (standard timeline). Same-bank transfers (if you have checking and savings at the same institution) are often instant. Wire transfers offer same-day delivery but typically cost $15-30.

For emergency access needs, maintain 1-2 months of expenses in a traditional checking account and use your high-yield savings account for the bulk of your emergency fund.

6: What Happens If Interest Rates Fall Further?

High-yield savings account rates are variable and can change weekly in response to Federal Reserve policy. If the Fed cuts rates at their February 18, 2026 meeting, HYSA rates will likely decline within 2-4 weeks. This is normal market behavior.

Opening now at 4.00%+ is strategically smarter than waiting, since rates can only decline or stabilize from current levels—they’re unlikely to rise significantly while the Fed maintains rate cuts.

7: Can I Earn Interest on Checking Accounts Too?

Yes, some online banks offer interest-bearing checking accounts. Varo checking earns 0.25% APY. However, savings accounts consistently offer 10-20x higher rates. Use high-yield savings accounts for long-term savings and checking accounts for daily spending management.

8: Is There a Maximum Deposit Limit?

FDIC insurance covers $250,000 per person per bank. You can deposit more, but only $250,000 is federally insured. For larger sums, open accounts at multiple FDIC-insured banks to maximize protection.

For married couples: Each spouse qualifies for $250,000 separate insurance at each bank. A joint account provides $500,000 protection ($250,000 per person).

9: Do I Need a Checking Account to Open Savings?

Most online banks offer both checking and savings but allow savings-only accounts. You’ll link an external checking account (from another bank) to fund and manage your high-yield savings account via ACH transfers.

10: Will the APY Drop After I Open My Account?

Rates are variable and can decrease anytime, but banks cannot retroactively reduce rates already earned on your existing balance without advance notice. Banks typically email rate change notifications 10-30 days before implementing changes, though they’re not legally required to provide advance notice.

Lock in today’s competitive rates by opening now rather than waiting for rates to potentially decline further.

11: What If I Need the Money in an Emergency?

High-yield savings accounts allow unlimited withdrawals (the old 6-per-month Regulation D limit was suspended in 2020). Money transfers to external checking accounts in 1-3 business days via standard ACH.

For true financial emergencies requiring same-day cash access, maintain 1-3 months of expenses in an instant-access checking account and use your high-yield savings account for months 4-6+ of your emergency fund strategy.

⚠️ Critical Disclaimer & Regulatory Compliance

THIS IS NOT FINANCIAL ADVICE: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, endorsements, or guarantees of returns. The author is not a certified financial advisor, investment professional, or licensed securities dealer. Before making financial decisions, consult with a qualified financial advisor licensed in your state.

INTEREST RATES ARE VARIABLE: APY rates presented are current as of January 22, 2026, but are subject to change at any time without notice. Banks can raise or lower rates daily based on Federal Reserve policy, competitive pressures, and business needs. Always verify current APY rates directly with the bank before opening an account or making financial decisions.

NO GUARANTEED RETURNS: While high-yield savings accounts are generally safe and FDIC-insured, APY rates are not guaranteed and will fluctuate with market conditions. Rates may decrease significantly if the Federal Reserve lowers the federal funds rate. Past performance does not guarantee future results.

FDIC INSURANCE LIMITS: FDIC insurance protects deposits up to $250,000 per depositor, per insured bank, per ownership category. Deposits exceeding this amount at a single institution may not be fully insured against bank failure. Verify bank FDIC membership status independently at FDIC.gov’s BankFind tool.

TAX IMPLICATIONS: Interest earned on savings accounts is taxable as ordinary income in the year earned. Consult a qualified tax professional about reporting requirements for your specific situation. The IRS requires banks to report interest income via Form 1099-INT when interest exceeds $10 annually. See IRS Publication 550 for complete interest income reporting requirements.

DATA ACCURACY WARNING: All rates, fees, and account details presented are accurate as of January 22, 2026. However, banks update terms, rates, and fees frequently without notice. The user assumes full responsibility for verifying current terms, rates, minimums, and fees directly from official bank websites before opening accounts or making deposits.

AFFILIATE RELATIONSHIP DISCLOSURE: This website may earn referral commissions if you click links and open accounts with featured banks. However, these business relationships do not affect the accuracy of our research, the objectivity of our recommendations, or the selection criteria for banks included in this guide.

CYBERSECURITY RISKS: Online banking carries inherent risks including cybersecurity threats, phishing attempts, identity theft, and unauthorized account access. Use strong unique passwords, enable two-factor authentication on all accounts, monitor account activity daily, and avoid accessing bank accounts on public WiFi networks.

INVESTMENT RISK WARNING: Savings accounts are designed for capital preservation and liquidity, not wealth accumulation. While earning 4.00%-5.00% APY provides better returns than traditional banks, it may not outpace inflation over long time horizons. For long-term wealth building beyond 3-5 years, consult a financial advisor about diversified investment strategies including stocks, bonds, and retirement accounts.

NO GUARANTEES: We make no guarantees regarding account approval, APY rate availability, account opening timeframes, fund transfer speeds, or any other banking outcomes. Individual experiences may vary based on credit history, identity verification, funding sources, and bank-specific policies.

CONSULT PROFESSIONALS: This guide does not replace personalized advice from certified financial planners (CFP), registered investment advisors (RIA), certified public accountants (CPA), or licensed attorneys. For advice specific to your financial situation, goals, risk tolerance, and tax circumstances, consult appropriate licensed professionals.

External links provided for reference purposes only. We do not control the content, accuracy, or availability of third-party websites and are not responsible for their policies, practices, or performance.

Final Thoughts: Take Action Today

The nine banks featured in this guide represent the most competitive, transparent, and customer-friendly high-yield savings options available to American savers in January 2026. Whether you prioritize maximum interest rate (Varo at 5.00%), zero-requirement simplicity (Newtek at 4.35%), or bundled banking convenience (Axos at 4.31%), the opportunity to earn 10-13 times the national savings rate is within immediate reach.

Your traditional bank is counting on your inertia. They profit when you accept 0.40% APY instead of demanding the 4.00%-5.00% rates you deserve. Every month you delay switching costs you real money—approximately $19 per month on a $5,000 balance, or $228 annually in lost earnings.

Take action this week. In a financial environment where the Federal Reserve may cut rates again on February 18, 2026, opening a high-yield account now locks in current competitive rates before they decline. Your future self will thank you for the disciplined decision to maximize savings interest while rates remain historically strong.

Start with our emergency fund calculator to determine your optimal savings target, then open an account at Varo, Newtek, or Axos to begin earning what your money deserves.

The banks are ready. Your money is ready. Are you?

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.