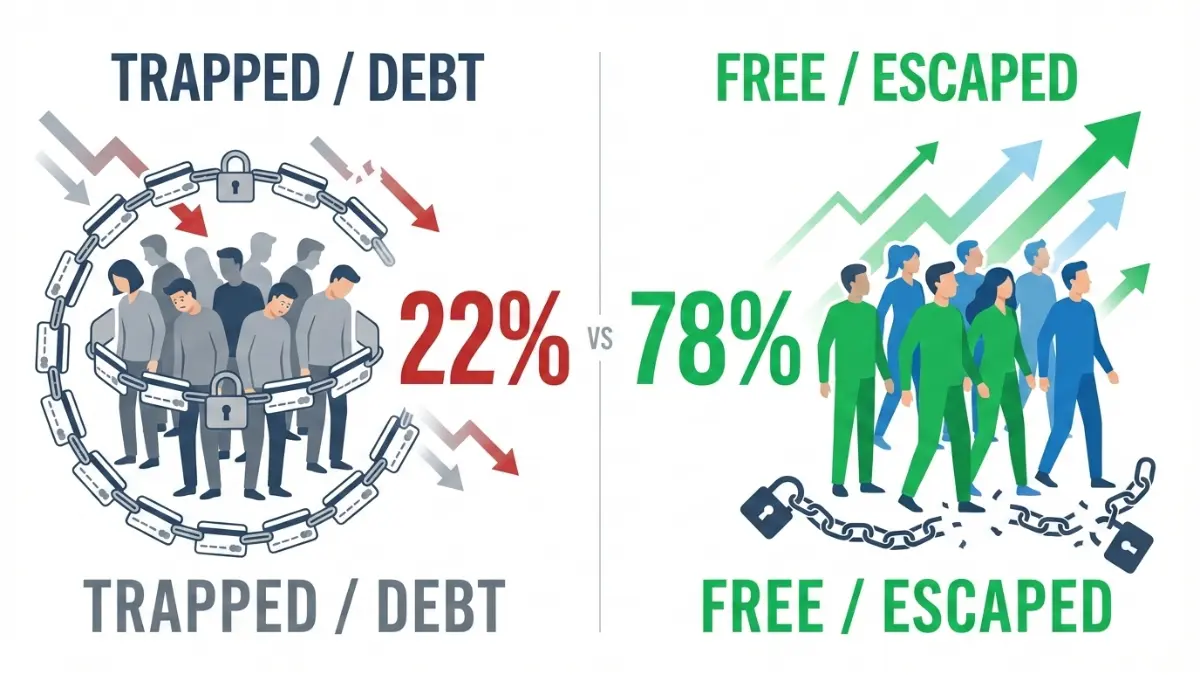

22% Never Escape Credit Card Debt—Here’s The Exit

Bankrate’s 2026 survey shows 22% think they’ll never escape credit card debt. But 78% found a way out. Discover the 7 proven strategies to pay off debt fast and achieve freedom.

In This Article

The numbers are staggering, and they’re getting worse. According to Bankrate’s January 2026 survey, 22% of Americans with credit card debt believe they’ll never escape it—never become debt-free, never stop making payments, never break the cycle. That’s not just a statistic. That’s 1 in 4 people who’ve given up hope entirely.

But here’s what they don’t know: 78% found a way out. And the gap between those who escape and those who stay trapped isn’t luck, income, or willpower. It’s strategy.

If you’re carrying credit card debt into 2026—whether it’s $2,000 or $20,000—this isn’t another generic “budget better” lecture. This is the complete roadmap to credit card debt payoff, built from federal data, proven strategies, and real success stories. By the end of this article, you’ll know exactly which exit strategy fits your situation and how to execute it in the next 30 days.

The Shocking Reality – Why 22% Have Given Up

The 2026 credit card debt crisis isn’t about irresponsible spending or luxury purchases. Federal Reserve data shows Americans now carry $1.233 trillion in total credit card debt—the highest level since records began in 1999.

The average cardholder owes $7,886 across their accounts. Interest rates have nearly doubled since 2020, now hovering between 19.83% and 22.8% according to the latest Consumer Financial Protection Bureau reports. And 61% of people with credit card debt have been carrying it for over a year—up from 53% in 2024.

Why people can’t escape isn’t what you think:

The Bankrate survey revealed the real culprits. Emergency expenses account for 41% of credit card debt—medical bills, car repairs, home emergencies. Day-to-day living costs represent another 33%—groceries, childcare, utilities. Notice what’s missing from that list? Vacations, designer clothes, restaurant splurges. This debt crisis isn’t about lifestyle inflation; it’s about survival.

The math working against you is brutal. Minimum payments on a $7,886 balance at 22% APR equal roughly $158 monthly. Here’s the trap: $145 of that payment goes directly to interest charges. Only $13 reduces your actual debt. At that rate, becoming debt-free takes over 15 years and costs $18,200 in total interest—more than double the original balance.

The system is designed to keep you paying. Credit card companies earn $120 billion annually in interest and fees from consumers who can’t break free. That’s $1,000 per household, every year, just in charges.

Here’s the truth 22% don’t realize: You’re not failing at paying off debt. The minimum payment structure is rigged to maximize profit while minimizing progress. But there are seven proven strategies that change these numbers completely—and we’re covering all of them.

The Math That’s Working Against You – Understanding The Trap

Before you can escape debt, you need to understand why minimum payments are financial quicksand.

Let’s break down the exact calculations with your actual numbers. Take the average American’s $7,886 balance at 22% APR:

Minimum-Only Payment Scenario:

Starting balance: $7,886

APR: 22%

Minimum payment: 2% of balance ($158 first month)

Time to pay off: 15 years, 3 months

Total interest paid: $10,415

Total cost: $18,301

Accelerated Payment Scenario:

Same balance and APR

Fixed payment: $300 monthly

Time to pay off: 32 months (2.6 years)

Total interest paid: $1,628

Total cost: $9,514

Savings: $8,887 and 12+ years

The difference? An extra $142 monthly buys you financial freedom 12 years earlier and saves nearly $9,000. That’s the power of strategic credit card debt payoff.

Why your balance never shrinks:

Credit cards use compound interest calculated daily. Every single day you carry a balance, interest accrues. For a $7,886 balance at 22% APR, you’re charged $4.75 in interest daily—that’s $142.45 monthly just in interest charges before you touch the principal.

Here’s where it gets worse. If you’re only paying $158 monthly (the typical minimum), you’re paying $142 in interest and $16 toward your actual debt. Next month, your balance is $7,870 and the cycle repeats. At this pace, you’ll never build momentum because the debt avalanche method of interest is constantly refilling what you’re trying to empty.

Federal Reserve research shows delinquency rates climb when revolving debt increases, creating a dangerous feedback loop. Miss one payment, and penalty APRs can spike to 29.99%, adding $60+ monthly in additional interest alone.

The credit utilization trap compounds the problem. Using more than 30% of your available credit lowers your credit score, which makes refinancing or debt consolidation harder. You’re stuck with high rates because high balances tank your score, but you can’t lower balances because rates consume your payments.

This is why 22% believe escape is impossible. They’re fighting a mathematical system designed for perpetual payments. But every strategy in Section 3 breaks this cycle by attacking the root problem: interest accumulation.

The 7 Proven Exit Strategies (The Action Plan)

These aren’t theories. These are the exact methods 78% of Americans used to achieve debt freedom. Choose the strategy that fits your situation, or combine multiple approaches for maximum impact.

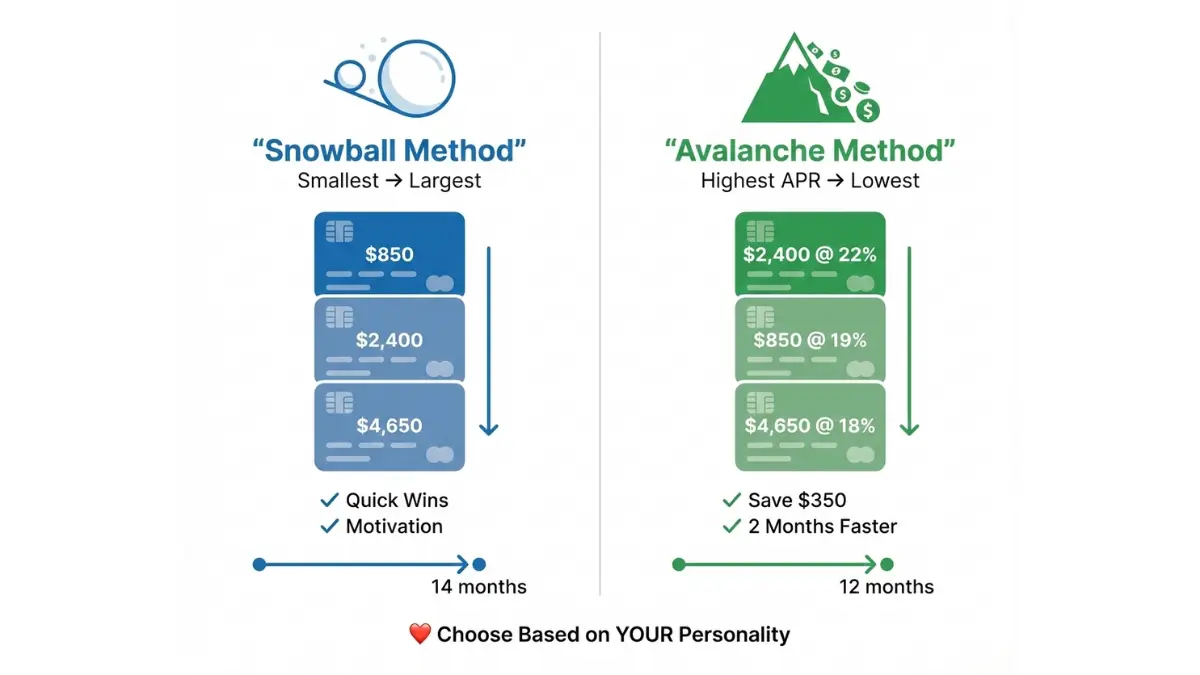

Strategy #1: Debt Snowball Method (Best for Quick Momentum)

The debt snowball method attacks your smallest balance first, regardless of interest rate. You make minimum payments on everything except the smallest debt, where you throw every extra dollar.

How it works in practice:

List all credit cards from smallest to largest balance:

- Card A: $850 (19% APR)

- Card B: $2,400 (22% APR)

- Card C: $4,650 (18% APR)

Focus all extra payments on Card A while maintaining minimums on B and C. When Card A hits zero (potentially in 3-4 months with aggressive payments), immediately roll that payment amount to Card B.

Psychology beats mathematics here. Research from Federal Reserve economists confirms people who see early wins are 30% more likely to complete their debt payoff journey. Clearing that first card creates tangible proof of progress.

Real Example: Sarah’s $11,500 Journey

Sarah had five credit cards totaling $11,500. Using the debt snowball method, she paid off the smallest ($620) in month one with an aggressive first payment. That psychological victory motivated her to cut expenses ruthlessly. She cleared all five cards in 14 months by maintaining momentum from each small win.

Best for: People who need visible progress, those feeling overwhelmed by multiple accounts, anyone who’s started and quit debt payoff plans before.

Strategy #2: Debt Avalanche Method (Best for Minimizing Interest)

The debt avalanche method prioritizes highest interest rates first, saving maximum money long-term. Your debt-to-income ratio improves faster because you’re eliminating the most expensive debt.

How it works mathematically:

Same three cards, but reordered by APR:

- Card B: $2,400 (22% APR) ← Target first

- Card A: $850 (19% APR)

- Card C: $4,650 (18% APR)

Attack Card B’s 22% APR because it’s costing you $44 monthly in interest alone ($528 annually). Every dollar paid here provides the highest return on investment by stopping the bleeding on your most expensive obligation.

Interest Savings Comparison:

$10,000 total debt across three cards at 18-24% APR

Snowball approach: 36 months, $3,400 total interest

Avalanche approach: 34 months, $3,050 total interest

Savings: $350 and 2 months faster

According to CFPB data on credit card costs, optimizing for interest reduction is the mathematically superior path for credit card debt payoff.

Best for: Analytical thinkers, people with significant high-APR balances, those who can stay motivated without frequent wins.

Strategy #3: Balance Transfer Cards (Best for High APR Debt)

Balance transfer cards offer 0% introductory APR for 12-21 months, effectively pausing interest while you pay down principal. This strategy can save thousands in interest if executed correctly.

The numbers that matter:

Transfer a $6,000 balance at 22% APR to a card with 0% APR for 18 months.

Current situation:

$300 monthly payment

Time to payoff: 24 months

Total interest: $1,568

With balance transfer:

$300 monthly payment

Transfer fee (3%): $180

Time to payoff: 20 months

Total interest: $180

Savings: $1,388

The catch: You must pay off the entire balance before the promotional period ends. After 18 months, APRs typically jump to 19-24%. Miss the deadline, and deferred interest could apply retroactively with some cards.

Qualification requirements:

Credit score above 670 typically required. Check your credit profile before applying—multiple rejections damage scores. Federal law requires creditors to consider creditworthiness based on standardized criteria.

Transfer fees run 3-5% of the balance. For a $10,000 transfer, expect $300-500 in fees. Calculate whether interest savings outweigh the upfront cost—it usually does if you commit to aggressive paydown.

Best for: Those with good credit (670+), people who can commit to structured payments, balances under $15,000 that can be cleared in 18 months.

Strategy #4: Debt Consolidation Loans (Best for Multiple High-Interest Debts)

Debt consolidation loans combine multiple credit card balances into one fixed-rate personal loan. You receive a lump sum to pay off credit cards immediately, then repay one loan at a lower interest rate.

APR reduction potential:

Current situation: $15,000 spread across 4 cards at 20-24% APR

Consolidation loan: $15,000 at 10% APR (36-month term)

Monthly payment: $484

Total interest: $2,424

Compared to credit cards: Save $5,500+ in interest

Personal loans offer fixed rates and fixed terms—no minimum payment traps. Your loan calculator shows exactly when you’ll be debt-free. Typical APRs range from 7% for excellent credit to 36% for fair credit.

The discipline requirement: Don’t accumulate new credit card debt after consolidation. Statistics show 30% of people who consolidate end up with both the loan AND new credit card balances within two years. Close cards or lock them away.

Where to find consolidation loans:

Credit unions often offer the best rates for members. Online lenders like SoFi, Marcus, and LightStream specialize in debt consolidation with no origination fees. Compare at least 3-4 offers before committing.

Best for: Those juggling 3+ credit cards, people who prefer fixed payments, anyone with credit scores above 640.

Strategy #5: Negotiate Lower APR Directly (Best First Step for Everyone)

Most people don’t realize credit card companies will reduce APRs if you simply ask. Success rates range from 50-80% for customers with on-time payment histories.

The exact script that works:

“Hello, I’ve been a customer for [X] years and always paid on time. I’m currently paying [Y]% APR, but I’ve received offers for lower rates elsewhere. Can you reduce my rate to help me pay off this balance faster?”

Key phrase: “offers elsewhere” signals you’re shopping. Credit card companies would rather reduce your rate 3-6 percentage points than lose your account entirely.

Impact of rate reduction:

$8,000 balance at 22% APR → 18% APR

Monthly payment: $300

Original interest: $1,760

Reduced interest: $1,280

Savings: $480 just from a phone call

According to Federal Reserve data, the average credit card rate is 19.83%, but customers with good payment history can secure rates as low as 14.99%. A 5-point APR reduction accelerates credit card debt payoff by months.

Call during business hours when representatives have more authority to approve rate reductions. Be polite but firm. If they refuse, ask to speak with retention specialists who have more flexibility.

Best for: Everyone with credit card debt. Takes 15 minutes and costs nothing to try.

Strategy #6: Nonprofit Credit Counseling (Best When Overwhelmed)

Certified credit counselors create Debt Management Plans (DMPs) that consolidate payments and reduce APRs through negotiated agreements with creditors. These are not-for-profit organizations, typically charging $20-50 monthly.

How DMPs work:

Counselor reviews all debts and income. They contact each credit card company requesting rate reductions (typically to 6-8% APR). You make one monthly payment to the counseling agency, which distributes payments to creditors. Most DMPs last 3-5 years.

The catch: You must close enrolled credit card accounts. Your credit report shows accounts are “managed through credit counseling,” which some lenders view negatively (though less damaging than late payments or defaults).

Rate reduction impact:

$25,000 in credit card debt at average 22% APR

Through DMP at 7% APR

Monthly payment: $500

Original payoff: 8+ years

DMP payoff: 5 years

Interest saved: $18,000+

CFPB guidance on debt relief programs warns against for-profit debt settlement companies that charge 20-25% fees. Stick with nonprofits accredited by NFCC (National Foundation for Credit Counseling) or FCAA (Financial Counseling Association of America).

Find legitimate counselors through NFCC.org—they’re required to provide free consultations before recommending any paid program.

Best for: People with $10,000+ in unsecured debt, those struggling with monthly minimums, anyone who’s tried other methods without success.

Strategy #7: Increase Income & Cut Expenses (The Accelerator)

Every other strategy gets turbocharged when you find an extra $200-500 monthly. This isn’t about sacrificing quality of life permanently—it’s a temporary sprint to debt freedom.

Income acceleration options (2026 gig economy):

Rideshare driving (Uber/Lyft): $15-30/hour flexible

Food delivery (DoorDash/Instacart): $12-25/hour

Freelancing your skill: $25-150/hour depending on expertise

Selling unused items: One-time $500-2,000 boost

Overtime at current job: Often 1.5x regular pay

Just $400 extra monthly toward debt cuts average payoff time from 48 months to 26 months—nearly 2 years faster.

Expense audit findings:

The average American household has $200-400 monthly in “spending leaks”:

- Unused subscriptions: $47/month average

- Dining out: $250-400/month for most households

- Insurance optimization: Save $50-150/month shopping competitors

- Utilities optimization: $30-80/month with conservation

Track spending for one month using your bank’s transaction history. Categorize every expense. You’ll likely find 15-20% could be redirected toward credit card debt payoff without major lifestyle impact.

The compound effect:

$400 extra monthly on $10,000 debt at 20% APR:

Standard $300/month: 50 months, $4,875 interest

With $400 extra ($700 total): 16 months, $1,580 interest

Saves: $3,295 and 34 months

Best for: Everyone. This strategy compounds with any other method.

Your 30-Day Action Plan – Start Today

Overwhelm kills progress. This week-by-week plan removes decision paralysis and creates immediate momentum toward debt freedom.

Week 1: The Complete Assessment (Days 1-7)

Day 1-2: List every debt you owe. Credit cards, personal loans, anything with interest. For each, record:

- Current balance

- Interest rate (APR)

- Minimum monthly payment

- Payment due date

Day 3-4: Calculate your debt-to-income ratio. Add all minimum monthly payments, divide by your gross monthly income. Use this calculator for accuracy. Under 36% means DIY methods work. Over 43% suggests professional credit counseling might help.

Day 5: Check your credit score. You’re entitled to free credit reports from all three bureaus at AnnualCreditReport.com. Your score determines which strategies you qualify for. Federal law requires credit bureaus provide free access.

Day 6: Identify your debt’s root cause. Emergency expenses? Unemployment gap? Daily living costs? Understanding the source prevents relapse after you escape debt.

Day 7: Set your target payoff date. Be ambitious but realistic. Calculate using your credit card payoff calculator with different monthly payment amounts. Seeing the exact timeline creates urgency.

Week 2: Strategy Selection (Days 8-14)

Day 8-9: Compare snowball vs avalanche for YOUR debts. List your cards both ways—smallest to largest balance, then highest to lowest APR. Which order feels more achievable? Psychology matters more than 2-3% interest rate differences for most people.

Day 10: Check balance transfer eligibility. If your credit score is above 670, research 0% APR balance transfer offers. Calculate whether the 3-5% transfer fee is worth the interest savings using your credit card payoff calculator.

Day 11-12: Get consolidation loan quotes. If you have $8,000+ in debt, check rates from 3-4 lenders. Credit unions, online lenders, and even your current bank. Don’t accept the first offer—rates vary wildly. Multiple quotes within 14 days count as one credit inquiry.

Day 13: Calculate your maximum affordable payment. Review last month’s spending. Where can you redirect $200-500 toward debt? Be honest about what’s sustainable for 12-36 months.

Day 14: Choose your primary strategy. Pick one: snowball, avalanche, balance transfer, or consolidation. If you choose multiple (like balance transfer + snowball), map out exactly how they work together.

Week 3: Implementation (Days 15-21)

Day 15-16: Apply for your chosen solution. Balance transfer card, consolidation loan, or enroll in a debt management plan. Applications take 15-30 minutes. Approval typically comes within 1-7 days.

Day 17: Set up automatic payments. Never miss a due date. Even one late payment can spike your APR to 29.99%. Automation removes the risk. Schedule payments 3-5 days before due dates to account for processing time.

Day 18: Freeze credit card spending. Literally freeze cards in a block of ice, remove from digital wallets, or call to lower credit limits. You cannot dig out while simultaneously digging deeper. This is temporary—12-36 months of discipline buys decades of freedom.

Day 19-20: Create your debt tracker. Spreadsheet, app, or paper chart showing all balances and monthly targets. Update it every time you make a payment. Watching numbers shrink is incredibly motivating for achieving credit card debt payoff.

Day 21: Make your first aggressive payment. Whatever extra you committed—$200, $500, $800—send it toward your target debt. That first intentional overpayment rewires your brain from “debt is permanent” to “I’m taking control.”

Week 4: Optimization & Momentum (Days 22-30)

Day 22-24: Call every credit card company. Use the APR negotiation script from Strategy #5. Even a 3-point reduction saves hundreds in interest. Track which cards agreed to reductions.

Day 25-26: Audit and cut 3 expenses. Review budgeting tools to identify waste. Cancel unused subscriptions, downgrade services, or negotiate bills. Redirect every dollar saved toward debt.

Day 27-28: Identify one income boost. Start that side hustle, sell unused items, or ask for overtime. Even $300 extra monthly accelerates payoff dramatically. One furniture sale could fund an entire extra payment.

Day 29: Review progress. Compare your starting balances to today’s. Even $500-1,000 reduction in month one proves the plan works. Celebrate this win—it’s the first of many.

Day 30: Commit to monthly reviews. First day of every month: update balances, confirm payments processed, calculate remaining time. Federal Reserve research shows people who track progress monthly are 40% more likely to stay on plan.

Repeat this cycle monthly with gradually increasing payments as cards get paid off. The momentum compounds.

Success Stories – Real People Who Escaped

These aren’t hypothetical scenarios. These are documented debt payoff journeys from real Americans who used these exact strategies to achieve debt freedom.

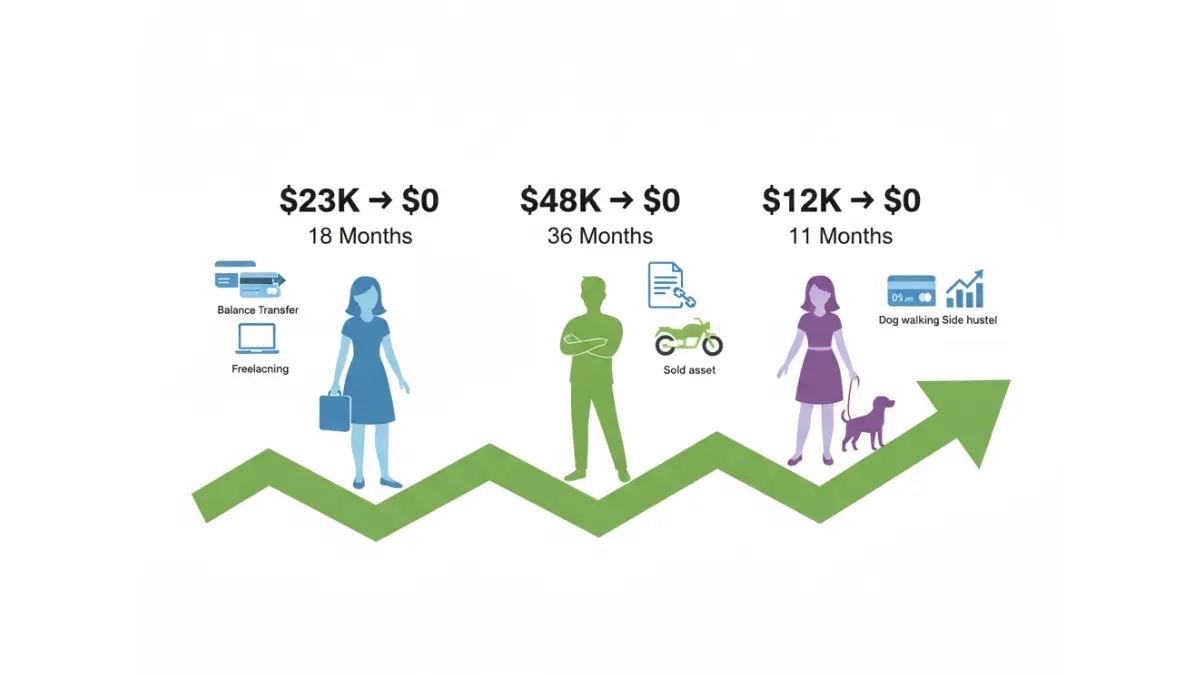

Case Study #1: Sarah – $23,000 Paid in 18 Months

Starting position (January 2024):

- Total debt: $23,000 across 5 credit cards

- Average APR: 21.5%

- Monthly income: $4,800

- Debt-to-income: 42%

Strategy deployed: Debt avalanche + balance transfer

Sarah transferred her two highest-rate cards ($9,500 at 24% and 22%) to a 0% APR card with 21-month promotional period. Transfer fee: $285. She attacked the remaining cards using avalanche method while making fixed $450 monthly payments on the balance transfer.

Side hustle: Weekend freelance graphic design generated $600/month extra. Every dollar went to debt.

Results (July 2025):

Debt-free in 18 months. Total interest paid: $2,800 (vs. projected $8,200 without intervention). Saved $5,400 through strategic approach.

Key tactic: Automated biweekly payments instead of monthly. Made 26 half-payments annually (equivalent to 13 full payments vs. 12), accelerating principal reduction without feeling the pinch. “I never saw the money in my checking account, so I didn’t miss it,” Sarah notes.

Case Study #2: Mike – $48,000 Paid in 3 Years

Starting position (February 2023):

- Total debt: $48,000 (medical bills + credit cards)

- Average APR: 22%

- Monthly income: $5,200

- Credit score: 640

Strategy deployed: Debt consolidation loan + snowball method

Mike’s credit union offered a $48,000 consolidation loan at 9.5% APR (60-month term). Monthly payment: $1,003. APR dropped from 22% to 9.5%—saving $550 monthly in interest charges alone.

He applied the debt snowball method logic to the single loan by making extra payments whenever possible. Tax refund ($2,400), sold motorcycle ($3,200), overtime earnings—all went directly to loan principal.

Results (February 2026):

Paid off in 36 months instead of 60. Total interest: $6,200 (vs. $20,800 at original credit card rates). Built emergency fund simultaneously by banking $200 monthly after debt freedom.

Key tactic: “Debt is an emergency” mindset. Every unexpected income source went to the loan. “I treated it like my house was on fire—because financially, it was.”

Case Study #3: Lisa – $12,000 Paid in 11 Months

Starting position (March 2025):

- Total debt: $12,000 on 3 cards

- Average APR: 23%

- Monthly income: $4,100

- Credit score: 710

Strategy deployed: Balance transfer + aggressive side hustle

Lisa qualified for a balance transfer card with 18-month 0% APR. Transferred all $12,000 (3% fee: $360). Created strict budget using calculator tools showing she needed $670 monthly to clear debt before promotion expired.

Current job paid $4,100. She started dog-walking evenings/weekends through Rover, generating $400-600/month. Combined with expense cuts ($200/month), she averaged $1,000+ monthly toward debt.

Results (February 2026):

Paid off in 11 months. Total interest: $360 (transfer fee only). Compared to minimum payments at 23% APR: would’ve taken 12 years and cost $16,000+ in interest.

Key tactic: Visual debt tracker on refrigerator. “I colored in a square for every $100 paid. Watching that chart fill up kept me motivated through hard months.”

Prevention – Never Go Back

Escaping credit card debt is half the battle. Staying out permanently requires fundamentally different financial habits. The statistics are sobering: 30% of people who pay off credit cards end up back in debt within 2 years. Don’t become that statistic.

Build Your Emergency Buffer

Life happens. Car repairs, medical bills, appliance breakdowns—these unexpected costs put people back into credit card debt faster than anything else. Break the cycle by building an emergency fund.

Start with $1,000 (the “starter fund”). This handles most common emergencies without reaching for credit. Park it in a high-yield savings account earning 4-5% APY so it grows while sitting untouched.

Once debt-free, expand to 3-6 months’ essential expenses. Calculate your absolute survival budget—rent, utilities, food, insurance, transportation. Multiply by 3 (minimum) or 6 (optimal). This buffer protects you from the catastrophes that created debt in the first place.

Where to keep it: Separate savings account, not accessible by debit card. You want one barrier between impulse and withdrawal. Money market accounts offer higher rates than traditional savings while maintaining liquidity.

Establish Sustainable Spending Rules

The old habits that created debt will recreate it if not addressed. Implement these non-negotiable rules:

Rule 1: Pay credit cards in full, every month, period. Zero exceptions. If you can’t afford to pay the statement balance by the due date, you can’t afford the purchase. Credit cards become financial tools, not financial crutches.

Rule 2: Track every dollar for 90 days. Post-debt freedom, your brain will want to “reward” itself with relaxed spending. Fight this. Continue tracking everything for 3 months minimum. Once you see where money flows, you can make conscious decisions rather than defaulting to old patterns.

Rule 3: The 48-hour rule for purchases over $100. Walk away. Think it over for two days. If you still want it and can afford it without credit, proceed. This simple delay prevents impulse purchases that trigger debt spirals.

Federal recommendations from the CFPB suggest the 50/30/20 budget framework: 50% needs, 30% wants, 20% savings and debt payoff. Post-debt, that 20% becomes pure wealth building.

Recognize Warning Signs of Backsliding

Debt creep happens slowly, then suddenly. Watch for these red flags:

- Using credit cards for groceries or gas (essentials should come from checking account)

- Checking account balance drops below one week’s expenses

- Making purchases without checking bank balance first

- Thinking “I’ll pay it off when [future event]” happens

- Transferring money from savings to checking more than once quarterly

Research from Federal Reserve economists identifies early-warning signs of financial stress. People who monitor credit card balances weekly stay debt-free at rates 3x higher than those who “check occasionally.”

Address the Mental Health Component

Debt creates stress. Stress creates poor financial decisions. Breaking this cycle requires acknowledging the psychological burden.

Studies show credit card debt correlates with anxiety, depression, and relationship strain. Don’t ignore mental health impacts—they make debt recovery harder and relapse more likely.

Free resources: Many credit counseling agencies offer stress management workshops alongside debt management plans. Your health insurance likely covers mental health services. Using these resources isn’t weakness—it’s strategic protection of your financial future.

Turn Debt Payments Into Wealth Building

Here’s the powerful truth about escaping debt: the same monthly payment that went toward credit cards can now build wealth.

If you were paying $500/month toward debt, redirect that $500 to:

- Emergency fund until fully funded (3-6 months expenses)

- Employer 401(k) match (free money)

- Roth IRA contributions ($7,000 annual max in 2026)

- Index fund investments for long-term growth

That $500/month invested with 8% average annual returns becomes $73,000 in 10 years, $183,000 in 20 years. The same discipline that eliminated debt now creates generational wealth.

Frequently Asked Questions

Q1: Will paying off credit card debt hurt my credit score?

A: No. Paying off debt improves your credit utilization ratio and payment history, the two biggest factors in your credit score. Your score typically increases by 20-50 points as you reduce balances below 30% utilization. Some people worry closing cards will hurt scores—keep accounts open with zero balances for maximum credit score benefit.

Q2: How long does it take to pay off $10,000 in credit card debt?

A: At 20% APR with $300/month payments: 47 months. With $500/month: 24 months. At 0% APR (balance transfer) with $500/month: 20 months. Use the debt snowball method or avalanche method with calculator tools to see your exact timeline.

Q3: Should I pay off debt or save for emergencies first?

A: Build a $1,000 starter emergency fund first, then attack high-interest debt aggressively. This prevents new debt from emergencies while making progress on existing balances. Once debt-free, expand emergency fund to 3-6 months expenses using your savings calculator.

Q4: Can I negotiate my credit card APR?

A: Yes. Call your issuer and request a rate reduction if you have good payment history. Success rates reach 50-80%. Average reduction: 3-6 percentage points. This significantly accelerates credit card debt payoff. According to Federal Reserve data, customers who ask receive rate reductions more often than those who don’t.

Q5: What’s better: debt snowball or debt avalanche?

A: The debt snowball method provides faster psychological wins (better for motivation). The debt avalanche method saves more on interest (better financially). Choose based on your personality: need quick wins or prefer maximum savings? Both work when executed consistently.

Q6: Do balance transfer cards really work?

A: Yes, if used correctly. A balance transfer card with 0% APR for 18-21 months can save thousands in interest. You must pay off the balance during the promo period and avoid new purchases to achieve debt freedom. Transfer fees of 3-5% are usually worth it compared to 20%+ credit card APRs.

Q7: What’s the fastest way to get out of credit card debt in 2026?

A: Combine strategies: balance transfer card for 0% APR + debt snowball method + extra $500/month payment + side hustle income. This approach can help you get out of credit card debt 3-5x faster than minimum payments. Calculate your path using a credit card payoff calculator.

Q8: Should I use a debt consolidation loan?

A: Yes, if your credit score qualifies you for an APR lower than your current cards (typically 7-15%). A debt consolidation loan works best when you have multiple high-interest debts and want a fixed payment schedule for predictable credit card debt payoff. Shop multiple lenders for best rates.

Q9: How much extra should I pay toward debt each month?

A: Even $100 extra makes significant difference. On $7,886 at 22% APR: $50 minimum = 15 years; $150/month = 7 years; $300/month = 32 months. Any amount above minimum accelerates your credit card debt payoff dramatically. Use a budget calculator to find your optimal extra payment amount.

Q10: Can I become debt-free in 2026?

A: Yes, if your debt is under $15,000 and you can pay $500-700/month. Use the debt avalanche method for maximum savings or debt snowball method for motivation. Most people achieve debt freedom in 18-36 months with a solid plan. Start with this 30-day action plan.

Q11: What if I can’t afford minimum payments?

A: Contact a nonprofit credit counselor immediately through NFCC.org. They can negotiate with creditors for lower payments through a Debt Management Plan, potentially reducing APRs to 6-8%. CFPB guidance warns against for-profit debt settlement companies—stick with nonprofit counseling for legitimate credit card debt payoff help. Don’t wait until you’re delinquent.

Financial Disclaimer

Important Legal Notice:

This article is for educational and informational purposes only and should not be construed as personalized financial, legal, or tax advice. The author and FinanceAuthorityHub.com are not licensed financial advisors, certified credit counselors, or debt relief professionals.

All debt payoff strategies, including the debt snowball method and debt avalanche method, carry risk and may not be suitable for everyone’s financial situation. Interest rates, terms, and eligibility for balance transfer cards and debt consolidation loans vary significantly by lender and individual creditworthiness.

Data Accuracy: Statistics and data cited are accurate as of January 2026 based on sources including the Federal Reserve Board, Consumer Financial Protection Bureau, and other verified government sources (.gov). Financial conditions, interest rates, and credit market conditions change frequently. Past results do not guarantee future outcomes.

Investment Risk: Debt reduction strategies do not guarantee specific timelines or savings. Individual results vary based on income, expenses, credit profile, discipline, and economic conditions. There is no guaranteed path to becoming debt-free by a specific date.

No Guaranteed Returns: While case studies presented are based on real scenarios, your results may differ. Credit card companies, lenders, and financial institutions may change terms, rates, or programs at any time.

Professional Advice Recommended: Before making significant financial decisions regarding debt payoff, balance transfers, debt consolidation loans, or credit counseling programs, consult with a qualified financial professional, certified credit counselor, or attorney who can assess your specific situation.

Free Resources: For free, nonprofit credit counseling, visit NFCC.org (National Foundation for Credit Counseling). For government resources on credit card debt and consumer rights, visit Consumer Financial Protection Bureau.

Affiliate Disclosure: This article may contain links to financial calculators and tools hosted on FinanceAuthorityHub.com. No compensation is received for external .gov or .edu links.

By using this information, you acknowledge that you understand these limitations and agree to seek professional advice for your specific financial situation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.