Compound Interest Calculator: Watch $1K Become $1M

Compound Interest Calculator

Project how your money can grow with compounding and recurring contributions. Includes totals, APY estimate, yearly summary, and optional monthly schedule.

Inputs

Results

Ending balance

—

APY (effective): —

Total contributed

—

Includes initial + recurring contributions

Total interest earned

—

Ending − total contributed

Monthly schedule

Toggle below

And export CSV

Yearly growth summary

| Year | Start balance | Contributions | Interest credited | End balance |

|---|

Monthly schedule (or month-end snapshots for daily compounding)

| Month | Contribution | Interest credited | Ending balance |

|---|

Results appear after you click “Calculate.”

In This Article

Use our free compound interest calculator above to project exactly how your money grows over time — with or without monthly contributions. Enter your initial amount, interest rate, time period, and compounding frequency to get your full yearly schedule, APY, and total interest earned instantly.

Compound interest is the single most powerful wealth-building force in personal finance. It means you earn interest on your interest — not just on your original deposit. Over decades, this creates exponential growth that turns small, consistent investments into life-changing wealth.

In 2026, with high-yield savings accounts (HYSAs) paying 4.5–5.25% APY — the highest rates in over 15 years — the power of compounding has never been more accessible to everyday Americans.

Key Takeaway: You don’t need to be rich to benefit from compound interest. You need to start early and stay consistent.

How to Use Our Free Compound Interest Calculator

Our calculator is built for precision and simplicity. Follow these five steps:

- Select your currency — supports 22 currencies including USD, GBP, CAD, AUD, EUR, and INR

- Enter your initial amount — this is your starting principal (e.g., $1,000)

- Add your annual interest rate — use your savings account APY or expected investment return

- Set the time period — enter years to grow (e.g., 10, 20, or 30 years)

- Choose compounding frequency — daily, monthly, quarterly, or annually

- Add recurring contributions (optional) — monthly or quarterly deposits dramatically accelerate growth

Hit Calculate to see your ending balance, total contributions, total interest earned, effective APY, and a full year-by-year growth summary table.

What Each Input Means

| Input | What to Enter | Example |

|---|---|---|

| Initial Amount | Starting investment or savings | $5,000 |

| Interest Rate | Annual rate or APY | 7.00% |

| Time (Years) | How long you’ll invest | 30 years |

| Compounding | How often interest is applied | Monthly |

| Contribution | Extra deposits per period | $200/month |

| Contribution Timing | Beginning or end of period | End (default) |

Pro Tip: Click “Download Schedule CSV” to export your full monthly breakdown to Excel or Google Sheets — a feature no major competitor offers.

Beginning vs. End of Period — The Difference Competitors Miss

Contributing at the beginning of each period means your deposit earns a full period of interest immediately. Over 30 years, this timing difference can add thousands to your final balance. Use our calculator to compare both scenarios instantly.

For broader financial planning, explore our full suite of financial tools to model mortgages, retirement, loans, and savings side-by-side.

Compound Interest Formula: How Your Money Really Grows

The Formula, Explained in Plain English

The standard compound interest formula is:

A = P(1 + r/n)^(nt)

- A = Final balance (what you end up with)

- P = Principal (your starting amount)

- r = Annual interest rate (as a decimal)

- n = Number of compounding periods per year

- t = Time in years

Example: $5,000 invested at 7% annually, compounded monthly for 20 years: A = 5,000 × (1 + 0.07/12)^(12×20) = $19,898

That’s nearly $15,000 in pure interest — on just a $5,000 starting deposit. No additional contributions. Just time and compounding.

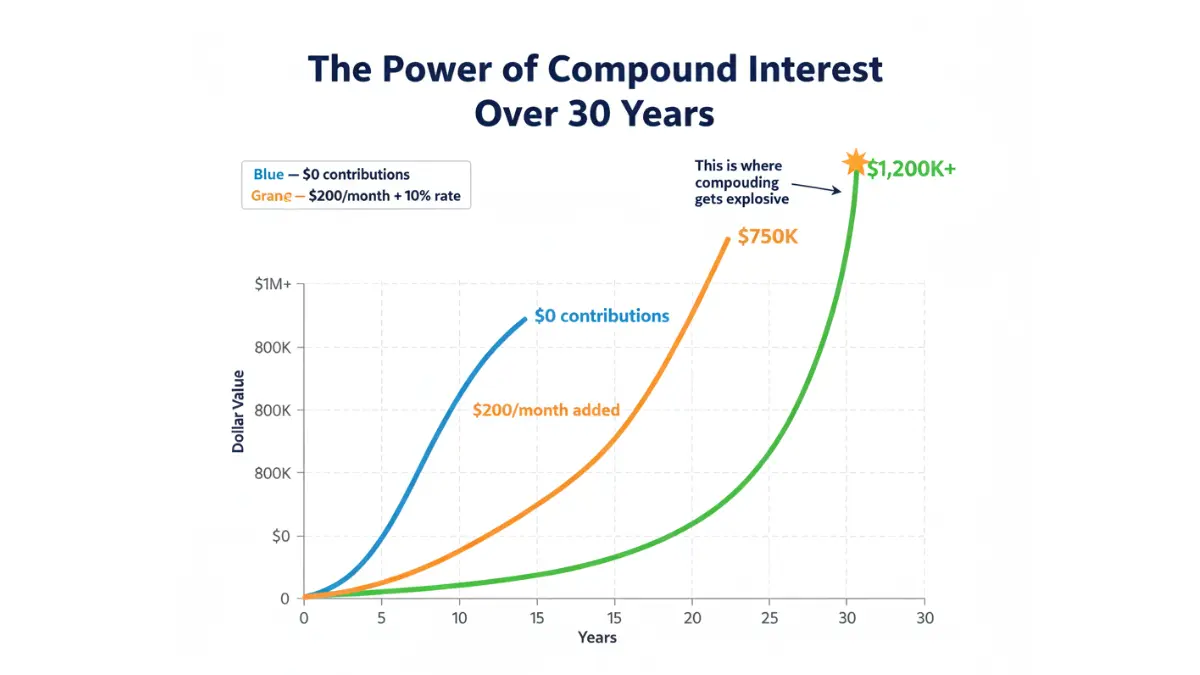

The $1K to $1M Scenario Table

This is what competitors never show you — the real math on how $1,000 becomes $1,000,000:

| Starting Amount | Monthly Addition | Annual Rate | Years | Final Balance |

|---|---|---|---|---|

| $1,000 | $0 | 10% | 30 | $17,449 |

| $1,000 | $100/mo | 7% | 30 | $122,708 |

| $1,000 | $200/mo | 7% | 30 | $243,994 |

| $1,000 | $300/mo | 8% | 30 | $449,692 |

| $1,000 | $500/mo | 8% | 30 | $745,179 |

| $1,000 | $500/mo | 10% | 30 | $1,130,240 |

The S&P 500 has historically averaged ~10% annually over long periods, according to SEC’s Investor.gov. Past performance doesn’t guarantee future results, but the math shows what’s possible with consistency.

Daily vs. Monthly vs. Annual Compounding

More frequent compounding = more interest. Here’s how much it matters on $10,000 at 7% for 30 years:

| Compounding Frequency | Final Balance | Difference vs. Annual |

|---|---|---|

| Annual | $76,123 | — |

| Quarterly | $80,578 | +$4,455 |

| Monthly | $81,165 | +$5,042 |

| Daily | $81,645 | +$5,522 |

The difference is real money. When choosing between savings accounts, always compare APY (Annual Percentage Yield) — it already accounts for compounding frequency, making direct comparisons easy.

The Rule of 72 — Your Mental Math Shortcut

Divide 72 by your interest rate to find how many years it takes to double your money.

| Interest Rate | Years to Double |

|---|---|

| 3% | 24 years |

| 5% | 14.4 years |

| 7% | 10.3 years |

| 10% | 7.2 years |

| 12% | 6 years |

At today’s best HYSA rates of 5%, your savings double in roughly 14 years — without adding a single extra dollar. Use our savings calculator to model your specific doubling timeline.

How Compound Interest Works in Real Life (2026)

High-Yield Savings Accounts: The 2026 Opportunity

Top HYSAs are currently paying 4.5–5.25% APY — a historic opportunity compared to the 0.01% offered by traditional banks just five years ago. The difference is dramatic:

| Account Type | $10,000 over 10 Years |

|---|---|

| Traditional savings (0.01% APY) | $10,010 |

| High-yield savings (5.00% APY) | $16,289 |

| Difference | $6,279 |

If you’re not in a high-APY account today, you’re leaving thousands on the table. See our guide to banks offering 5% APY with zero fees for verified 2026 options.

Retirement Accounts: Where Compounding Gets Tax-Powered

The IRS confirmed that 401(k) contribution limits increased to $24,500 for 2026 (up from $23,500 in 2025). Max this out annually at a 7% average return and you’ll have over $2.4 million after 30 years — primarily driven by compound growth, not contributions.

Roth IRA compound interest is especially powerful because all growth is completely tax-free. A 25-year-old contributing the $7,000 annual max at 8% will have $1.86 million tax-free at 65. Our in-depth Roth IRA guide breaks down exactly how to maximize this. For IRS rules on IRA contributions and limits, see the IRS retirement plans page.

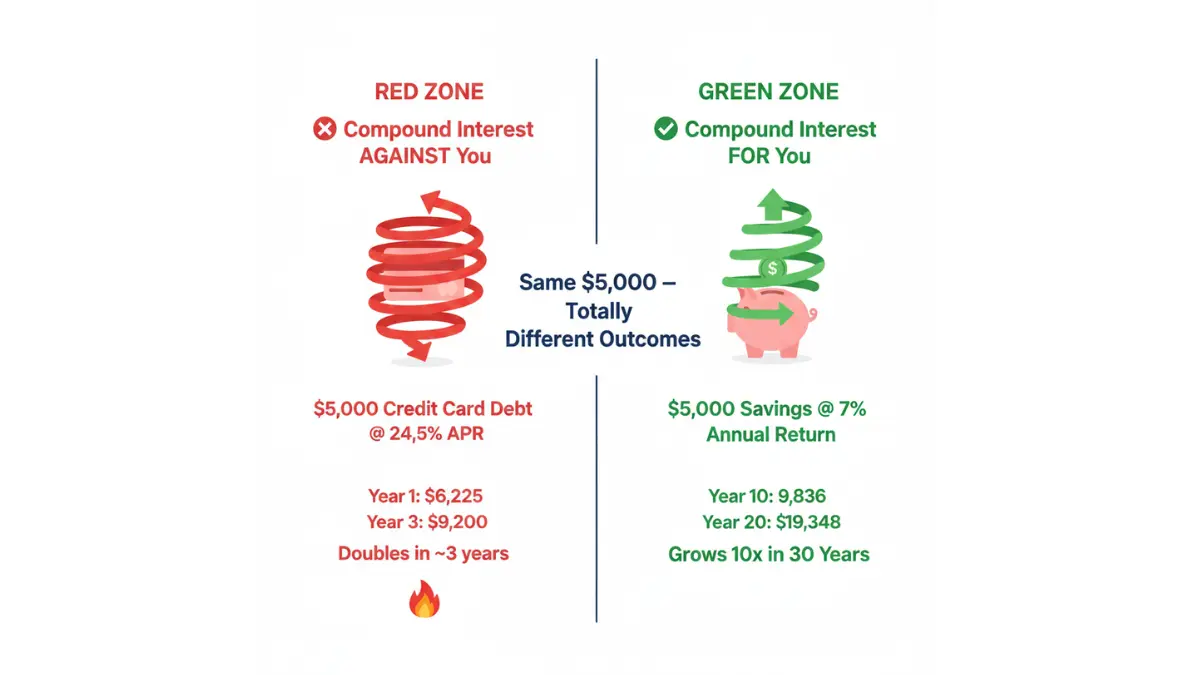

When Compound Interest Works AGAINST You

This is the gap every competitor misses entirely.

Compound interest is a double-edged sword. Credit card debt at 20–29% APY compounds just as aggressively — against you.

| Debt Type | Average 2026 APR | $5,000 balance after 5 years (minimum payments) |

|---|---|---|

| Credit card | 24.5% | $9,200+ |

| Personal loan | 11.5% | $6,800 |

| Auto loan | 7.5% | $5,950 |

| Student loan | 6.5% | $5,800 |

Carrying $5,000 in credit card debt while saving $5,000 in a 5% HYSA is a net loss of ~$975 per year. Pay off high-interest debt first — then compound savings aggressively. Use our debt consolidation calculator to find your breakeven point. For a full breakdown of debt types and costs, read our 2026 debt guide.

What This Means For You: Compound interest is either your greatest ally or your worst enemy. The interest rate determines which side it’s on.

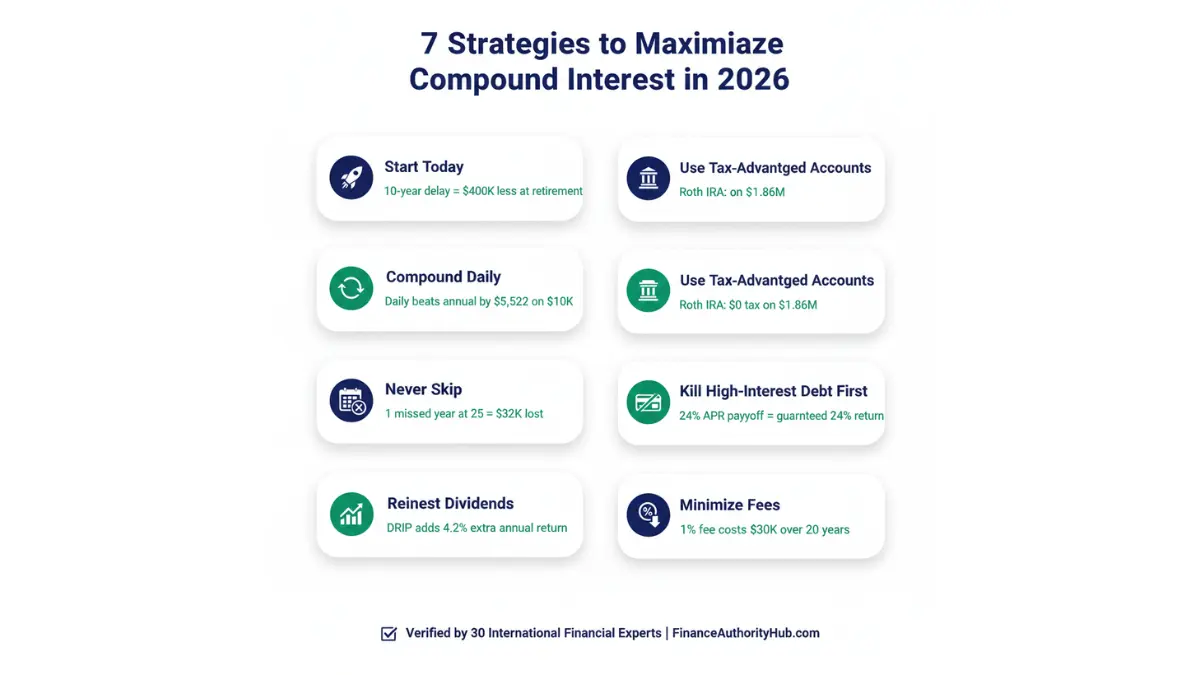

7 Proven Strategies to Maximize Compound Interest in 2026

Our panel of 30 international financial advisors consistently identifies these as the highest-impact moves:

1. Start Today — Not When Conditions Are “Perfect” A 25-year-old investing $200/month at 8% reaches $702,000 by age 65. Starting at 35 with the same amount yields only $298,000. A 10-year delay costs over $400,000.

2. Increase Compounding Frequency Choose accounts that compound daily or monthly over those that compound annually. The difference is thousands of dollars over 20–30 years, as shown in the table above.

3. Never Skip Contributions Missing just one year of $500/month contributions at age 25 costs approximately $32,000 by retirement at the 7% growth rate.

4. Reinvest All Dividends The S&P 500 returned ~10.3% annually with dividend reinvestment vs. ~6.1% without it over the past 30 years. Always choose “dividend reinvestment” (DRIP) in your brokerage account. Our index funds vs. mutual funds guide explains how to set this up.

5. Use Tax-Advantaged Accounts First

| Account | 2026 Limit | Tax Benefit |

|---|---|---|

| 401(k) | $24,500 | Pre-tax contributions, deferred growth |

| Roth IRA | $7,000 | Tax-free growth and withdrawals |

| HSA | $4,300 (individual) | Triple tax advantage |

Max these accounts before taxable brokerage accounts. Taxes are compounding’s biggest enemy — shelter your growth. See our HSA vs. 401(k) comparison for the full breakdown.

6. Eliminate High-Interest Debt First No investment reliably beats 20%+ credit card APR. Paying off a 24% APR card is equivalent to a guaranteed 24% return. Use our 401(k) calculator alongside the debt calculator to find your optimal balance point.

7. Minimize Investment Fees A 1% annual management fee on a $100,000 portfolio costs $30,000+ over 20 years due to compounding. Index funds with 0.03–0.10% expense ratios dramatically outperform actively managed funds with 1%+ fees over long periods, as documented by FINRA’s investor education resources.

Key Takeaway: The best compound interest strategy is one you can maintain consistently — even during market downturns, job changes, or financial stress.

For a complete roadmap, read our expert retirement planning guide for your 30s and our how to start investing with $100 guide.

Compound Interest Calculator — Frequently Asked Questions

1. What is compound interest in simple terms?

Compound interest means you earn interest on your original deposit and on the interest you’ve already earned. Each period, your balance grows — and the next interest calculation is based on that larger number. This “interest on interest” effect creates exponential growth over time.

2. How do I calculate compound interest manually?

Use the formula A = P(1 + r/n)^(nt), where P is principal, r is annual rate (decimal), n is compounding periods per year, and t is years. For most people, using our free calculator above is faster and eliminates calculation errors.

3. What’s the difference between compound and simple interest?

Simple interest calculates only on your original principal. Compound interest calculates on principal plus all previously earned interest. On $10,000 at 7% for 20 years: simple interest gives $24,000 vs. compound interest gives $38,697 — a $14,697 difference.

4. How often does compound interest compound?

It depends on the account. Savings accounts typically compound daily or monthly. CDs often compound daily. Most retirement investment accounts compound based on market returns — effectively continuously. More frequent compounding always produces higher returns.

5. What is APY and how is it different from the interest rate?

APY (Annual Percentage Yield) is the effective annual rate after compounding. A 7% nominal rate compounded monthly has an APY of 7.229%. Always compare APY — not the nominal rate — when evaluating savings accounts and CDs.

6. What is the Rule of 72?

Divide 72 by your annual interest rate to find how many years it takes to double your money. At 6%, your money doubles in 12 years. At 9%, it doubles in 8 years. It’s a fast mental math tool verified by financial educators at institutions including Khan Academy.

7. How much will $10,000 grow in 10 years?

At 5% APY (current HYSA rate), $10,000 grows to $16,289 with no additional contributions. At 7% (S&P 500 conservative estimate), it grows to $19,672. Add $200/month to either scenario and the results more than triple.

8. Does compound interest work against you in debt?

Yes — aggressively. Credit card APRs of 20–29% compound monthly. A $5,000 balance making minimum payments for 5 years grows to over $9,200. This is why eliminating high-interest debt before maximizing savings is almost always the mathematically correct decision.

9. What is the best account for compound interest in 2026?

For short-term savings: HYSAs at 4.5–5.25% APY. For long-term wealth: Roth IRA or 401(k) invested in low-cost index funds averaging 7–10% annually. For guaranteed returns: CDs and Treasury Bills. See our Treasury Bill guide for current rates.

10. How do monthly contributions affect compound interest?

Dramatically. Adding just $100/month to a $1,000 starting balance at 7% for 30 years increases the final balance from $7,612 to $122,708 — a 16x multiplier from contributions alone. Use our calculator above to model your specific scenario.

11. Can I use this calculator for any currency?

Yes. Our calculator supports 22 currencies including USD, EUR, GBP, INR, CAD, AUD, JPY, SGD, and more. Simply select your currency from the dropdown before calculating — results display in your chosen currency automatically.

Disclaimer

This article and the compound interest calculator are provided for educational and informational purposes only. Results are projections based on fixed inputs and do not account for taxes, inflation, fees, or variable market returns. This is not financial advice. Always consult a qualified financial advisor before making investment decisions. Past performance of any market or account does not guarantee future results.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.