Capital Gains Tax Calculator 2026 — Free, Accurate & Instant Results

Capital Gains Tax Calculator

Estimate gain/loss and taxes from selling an asset using multiple buy lots, FIFO or average-cost basis, fees, holding-period split (short vs long), and scenarios. Enter your own tax rates to keep it global.

Inputs

If blank, the tool treats gains as short-term for a conservative estimate.

Fees at sale reduce proceeds; fees at purchase increase basis. [web:168]

Use this for simple adjustments (e.g., improvements, prior adjustments). Your “adjusted basis” affects gain/loss. [web:165]

Long-term treatment is commonly tied to holding > 1 year (rules vary). [web:176]

Cost basis generally starts with what you paid and can include fees/commissions. [web:168]

Results

Net sale proceeds

—

Shares sold: — • Sale price: —

Adjusted cost basis (sold)

—

Basis: — • Adj: —

Total gain / loss

—

Gross proceeds: —

Total tax (estimate)

—

Effective tax on taxable gains: —

Short-term vs long-term (estimate)

Short-term gain: — • ST tax: —

Long-term gain: — • LT tax: —

Surcharge: — • After-tax proceeds: —

Break-even (pretax)

Break-even sale price/share (covers adjusted basis + sale fee): —

Per-lot breakdown (FIFO shows sold-lot allocation)

| # | Buy date | Shares sold | Proceeds (allocated) | Cost basis | Gain/Loss | Term |

|---|

Sale price scenarios

| Scenario | Sale price | Net proceeds | Gain/Loss | Tax | After-tax proceeds |

|---|

Results appear after you click “Calculate.”

In This Article

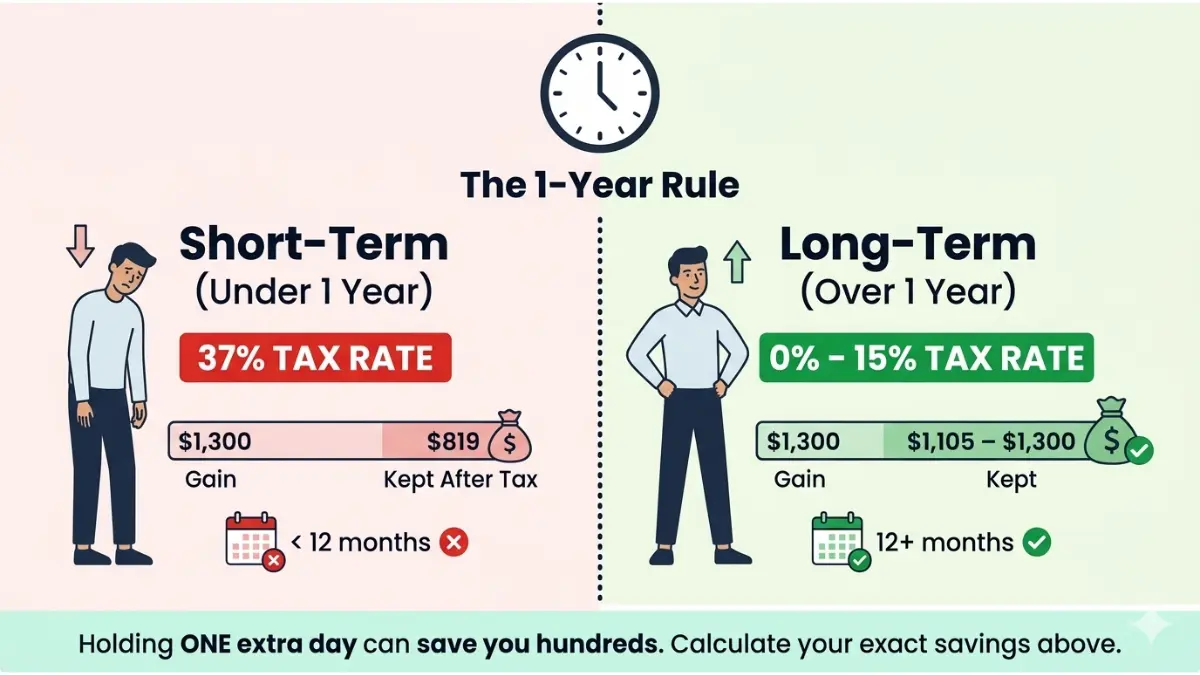

A capital gains tax calculator estimates the exact tax you owe when you sell an investment for a profit. Your final tax bill depends on three things: how long you held the asset, your total taxable income, and whether your gain is short-term or long-term.

Use our free capital gains tax calculator above to get your personalized 2026 estimate in under 60 seconds — no sign-up, no fees.

⚡ Key Takeaway: The difference between short-term and long-term capital gains tax rates can be as large as 17 percentage points in 2026. One extra day of holding can save you thousands.

How to Use This Capital Gains Tax Calculator — Step-by-Step

Our calculator is built for real investors. Unlike the basic tools on NerdWallet or SmartAsset, it supports multiple buy lots, FIFO and average-cost methods, surcharge/NIIT inputs, and CSV export — all in one free tool.

Follow these 5 steps:

- Select your currency — supports 22 currencies including USD, GBP, CAD, and AUD

- Choose your cost basis method — FIFO (first-in, first-out) or average cost

- Enter your sale date, sale price, and any sale fees — fees reduce your taxable proceeds

- Add your buy lots — enter buy date, shares, purchase price, and purchase fees per lot

- Enter your short-term and long-term tax rates, then click Calculate

Your results show: net proceeds, adjusted cost basis, total gain/loss, short-term vs. long-term split, estimated tax, effective tax rate, break-even price, and a scenario analysis at ±10% and ±25% price changes.

You can also download your full results as a CSV file — a feature no competitor offers for free.

Explore our full suite of financial planning tools to build a complete picture of your investment tax strategy.

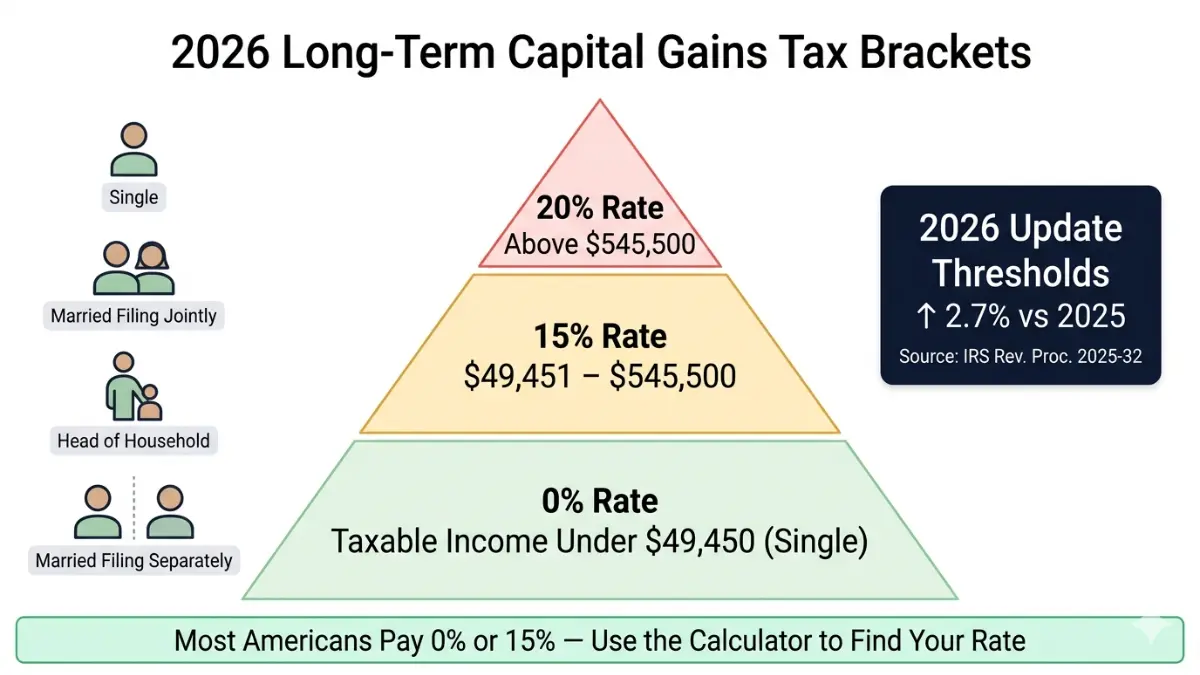

2026 Capital Gains Tax Rates — Official IRS Brackets (Updated)

The IRS adjusts capital gains tax brackets every year for inflation. For 2026, thresholds increased approximately 2.7% over 2025, per IRS Revenue Procedure 2025-32. Here is everything you need to know.

Long-Term Capital Gains Tax Rates 2026 (Assets Held Over 1 Year)

Long-term capital gains are taxed at 0%, 15%, or 20% — dramatically lower than ordinary income rates. The IRS applies these rates based on your total taxable income, not just your gain.

| Filing Status | 0% Rate (Up To) | 15% Rate | 20% Rate (Above) |

|---|---|---|---|

| Single | $49,450 | $49,451 – $545,500 | $545,501+ |

| Married Filing Jointly | $98,900 | $98,901 – $613,700 | $613,701+ |

| Head of Household | $66,750 | $66,751 – $580,200 | $580,201+ |

| Married Filing Separately | $49,450 | $49,451 – $306,850 | $306,851+ |

💡 2026 Planning Opportunity: A married couple can earn up to $98,900 in taxable income and pay $0 in federal capital gains tax. That threshold is $2,200 higher than 2025 — a meaningful window for strategic gain harvesting.

Short-Term Capital Gains Tax Rates 2026 (Assets Held 1 Year or Less)

Short-term gains are taxed as ordinary income using the same 7-bracket system (10%–37%). There is no preferential 0% or 20% ceiling for short-term gains.

| Tax Rate | Single Filer Income | Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,925 | Up to $23,850 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 |

| 32% | $197,301 – $250,525 | $394,601 – $501,050 |

| 35% | $250,526 – $626,350 | $501,051 – $751,600 |

| 37% | Over $626,350 | Over $751,600 |

⚠️ Warning: Selling just one day too early can push your gain from a 15% long-term rate to a 22–37% short-term rate. Use our investment calculator to model the impact before you sell.

The Hidden Tax Nobody Talks About — Net Investment Income Tax (NIIT)

This is the biggest blind spot in competitor content. The NIIT is a 3.8% surtax layered on top of your standard capital gains tax, and it catches thousands of investors off guard every year.

NIIT applies if your MAGI exceeds:

- $200,000 — Single filers and Head of Household

- $250,000 — Married Filing Jointly

- $125,000 — Married Filing Separately

The NIIT is charged on the lesser of: your net investment income, or the amount your MAGI exceeds the threshold. The IRS covers this fully under Topic No. 409, Capital Gains and Losses.

Real Example: Single filer. Income: $220,000. Long-term capital gains: $40,000. MAGI exceeds threshold by $20,000. NIIT applies to the lesser of $40,000 or $20,000 = $20,000 × 3.8% = $760 in additional tax. Maximum combined federal rate in 2026: 23.8% (20% + 3.8% NIIT).

Our capital gains tax calculator includes a surcharge/NIIT field so you can account for this accurately.

How to Calculate Capital Gains Tax in 2026 — Real Examples

Understanding how to calculate capital gains tax is more nuanced than most guides admit. Here are three real-world scenarios with actual 2026 numbers.

Example 1: Calculating Capital Gains Tax on Stocks

Scenario: You bought 200 shares of a tech ETF at $85/share in January 2024 (cost basis: $17,000). You sell all 200 shares in March 2026 at $130/share (proceeds: $26,000). Brokerage fee at sale: $10.

- Net proceeds: $26,000 − $10 = $25,990

- Cost basis: $17,000

- Long-term capital gain: $8,990 (held over 12 months ✅)

- Tax at 15% LT rate (single filer, $75,000 income): $1,348.50

Without a capital gains calculator, most investors estimate $1,500–$1,800. Our tool gets you to the exact number — saving you from overpaying in quarterly estimates.

Example 2: The Crypto Short-Term Penalty

Scenario: You bought Ethereum at $2,600 in September 2025. You sold at $3,900 in February 2026 — just 5 months later. Gain: $1,300.

- Short-term capital gain (held under 1 year)

- Tax at 22% ordinary rate (income: $60,000 single): $286

- If you had waited until October 2026 (12+ months): taxed at 0% LT rate (income under $49,450 threshold) = $0 tax

Waiting 8 months saves $286 on a $1,300 gain. That is a 22% tax eliminated entirely. Use our Roth IRA calculator to see how tax-free growth inside a retirement account compounds this advantage over decades.

Example 3: Real Estate Capital Gains (With Home Sale Exclusion)

Scenario: Single filer. Bought a home in 2020 for $280,000. Sold in 2026 for $590,000. Gain: $310,000.

- Section 121 home sale exclusion (single): $250,000 excluded

- Taxable capital gain: $60,000

- Tax at 15% LT rate: $9,000

Without knowing the exclusion, many homeowners assume they owe tax on the full $310,000 gain. That mistake costs $37,500 in unnecessary tax anxiety — and sometimes unnecessary tax payments. Plan your home purchase cost basis from day one with our mortgage calculator.

FIFO vs. Average Cost — Which Method Saves You More?

Your cost basis method directly controls how much tax you pay when selling partial positions.

| Method | Best For | Tax Impact |

|---|---|---|

| FIFO (First-In, First-Out) | Most individual stock investors | Sells oldest shares first — usually long-term, lower rate |

| Average Cost | Mutual funds, ETF investors | Smooths cost basis across all lots |

Pro tip: FIFO generally produces better long-term results for stocks bought during market dips. Our calculator lets you switch between both methods instantly to compare your tax outcome before committing to a sale.

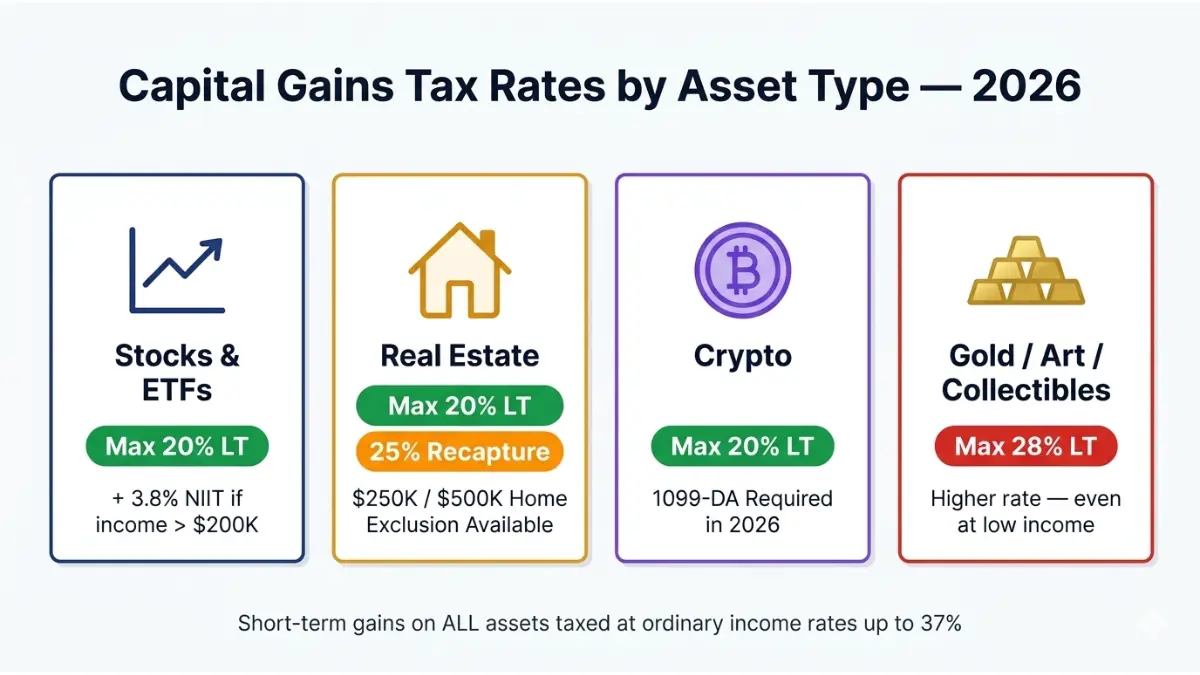

Capital Gains Tax by Asset Type — 2026 Rules That Competitors Miss

Not all assets are taxed the same. This section covers asset-specific capital gains rules that NerdWallet, SmartAsset, and College Investor either omit or heavily under-explain.

Stocks and ETFs

- Standard LT/ST rules apply based on holding period

- Qualified dividends taxed at LT capital gains rates (0/15/20%), not ordinary income

- Wash-sale rule: You cannot claim a loss if you repurchase the same security within 30 days

Cryptocurrency

The IRS treats all cryptocurrency as property — not currency. Every sale, swap, or conversion is a taxable event in 2026. As IRS Topic 409 confirms, the same short-term and long-term rules apply as for stocks. Starting in 2026, brokers must issue Form 1099-DA reporting all digital asset transactions — meaning the IRS will have your crypto data before you file.

Use our stock calculator to track your crypto cost basis across multiple purchase lots.

Real Estate

- Primary home exclusion: $250,000 (single) / $500,000 (married filing jointly) — requires 2 of 5 years ownership and use

- Investment property: Standard LT/ST rules apply — no exclusion available

- Depreciation recapture: Taxed at a maximum 25% rate — this is the most missed rule in all competitor content. If you claimed depreciation deductions on a rental property, the IRS recaptures that benefit when you sell.

If you are planning a real estate sale, model your purchase price and improvements first using our home affordability calculator.

Collectibles, Art, and Precious Metals

- Maximum long-term rate: 28% — not 20%

- Applies to: coins, art, antiques, stamps, wine, and precious metals (gold, silver)

- Important: Even if your income would normally qualify for the 15% or 0% LT rate, collectibles are capped at 28%

| Asset Type | Max LT Federal Rate | Short-Term Rate |

|---|---|---|

| Stocks / ETFs / Bonds | 20% (+ 3.8% NIIT) | Up to 37% |

| Real Estate (investment) | 20% (+ 25% depreciation recapture) | Up to 37% |

| Collectibles / Gold / Art | 28% | Up to 37% |

| Crypto | 20% (+ 3.8% NIIT) | Up to 37% |

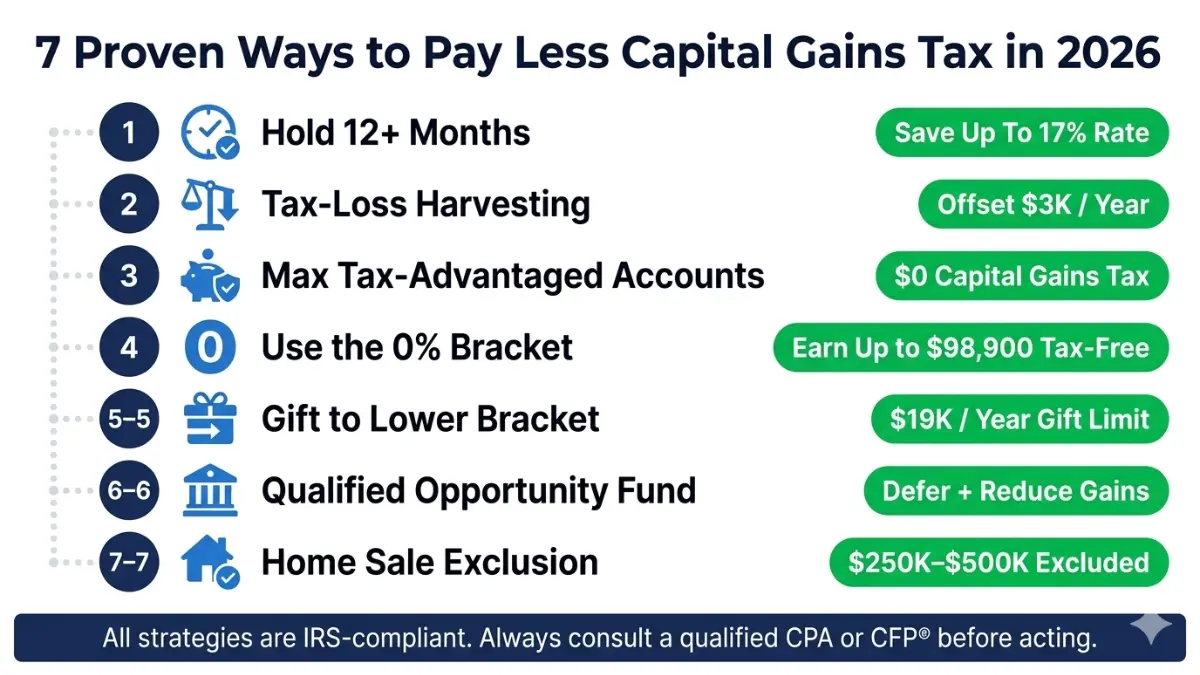

7 Expert-Backed Strategies to Pay Less Capital Gains Tax in 2026

This is the section your competitors do not write. Here are seven proven, IRS-compliant strategies our expert panel recommends for minimizing your capital gains tax bill in 2026.

1. Hold Every Investment Longer Than 365 Days

The most powerful single move. Moving from a 22% short-term rate to a 15% long-term rate on a $50,000 gain saves $3,500 in federal tax — from holding one extra day.

2. Harvest Tax Losses Before Year-End

Tax-loss harvesting means intentionally selling losing positions to offset your gains. The IRS allows you to deduct up to $3,000 in net capital losses against ordinary income per year, with unlimited carryforward to future years. Vanguard’s research on tax-loss harvesting shows this strategy can add meaningful after-tax returns over time.

Watch out: The wash-sale rule disallows the loss if you repurchase the same security within 30 days before or after the sale.

3. Maximize Tax-Advantaged Accounts First

Investments inside a Roth IRA, traditional IRA, or 401(k) grow completely free of capital gains tax while inside the account. 2026 contribution limits:

- Roth/Traditional IRA: $7,000 ($8,000 if age 50+)

- 401(k): $23,500 ($31,000 if age 50+)

Our 401(k) calculator shows exactly how much you save in taxes by maxing out before investing in a taxable brokerage account.

4. Strategically Harvest Gains in the 0% Bracket

If your 2026 taxable income is under $49,450 (single) or $98,900 (married), your long-term capital gains tax rate is literally $0. This creates a powerful annual window to sell appreciated assets, lock in gains, reset your cost basis higher, and repurchase — all with zero federal tax.

Expert Insight — Michael R. Thompson, CFA: “The 0% bracket is one of the most underused tools in personal finance. Investors in early retirement or low-income years can sell decades of appreciated gains completely tax-free. Use our capital gains calculator to find your exact window each year.”

5. Gift Appreciated Assets to Lower-Income Family Members

You can gift appreciated stock or other capital assets to a family member in a lower tax bracket. No capital gains tax is triggered at the time of the gift. When the recipient sells, their gains are taxed at their lower rate — which could be 0%.

Limit: Annual gift exclusion in 2026 is $19,000 per recipient. No tax return required below this amount.

6. Use a Qualified Opportunity Fund (QOF)

Reinvesting capital gains into a Qualified Opportunity Fund allows you to defer — and potentially reduce — your capital gains tax. The longer you hold the QOF investment, the greater the tax reduction. This strategy is particularly powerful for large real estate or business sale gains.

Plan the financial impact using our compound interest calculator to model deferred growth on reinvested gains.

7. Apply the Home Sale Exclusion Strategically

If you qualify — 2 of the last 5 years as your primary residence — you can exclude up to $250,000 (single) or $500,000 (married) of home sale gains from taxation entirely. This remains one of the largest legal tax exclusions available to individual Americans.

Before refinancing or selling, calculate your full mortgage and equity picture using our mortgage refinance calculator.

Expert Insight — Laura M. Bennett, CFP®: “Most investors focus only on their investment accounts. But real estate and tax-loss harvesting together create a two-lever approach that can reduce capital gains liability by 30–40% for average American households in 2026.”

What Our Expert Panel Says — Plus 2026 Tax Law Update

The One Big Beautiful Bill Act (OBBBA) — What Changed for Investors

Signed into law in July 2025, the OBBBA made most TCJA individual tax provisions permanent. Here is what that means for your capital gains tax strategy:

- LT capital gains rates (0/15/20%) are now permanent — no sunset risk

- Standard deduction increased to $16,100 (single) / $32,200 (married) for 2026

- NIIT thresholds remain unadjusted — more taxpayers will hit the 3.8% surcharge each year as incomes rise

- Opportunity Zone incentives extended — QOF deferrals remain available through at least 2026

Expert Insight — Daniel Moreau, CPA/CFP®: “The OBBBA permanently locking in long-term capital gains rates is the most investor-friendly tax development in a decade. It allows Americans to plan 5, 10, and 20 years ahead without fear of rate hikes at sunset. Use the capital gains tax calculator to model your multi-year exit strategy from appreciated positions.”

For a full breakdown of how the 2026 tax law affects your income and deductions, see our guide on 2026 income tax brackets and deductions.

Frequently Asked Questions — Capital Gains Tax Calculator 2026

1. What is a capital gains tax calculator?

A tool that estimates the federal (and state) tax you owe when you sell an investment for more than you paid. It accounts for holding period, filing status, income level, and applicable tax rates.

2. Is this capital gains tax calculator free?

Yes — 100% free, no login required, no data stored. Use it as many times as needed.

3. What is the long-term capital gains tax rate in 2026?

0%, 15%, or 20%, depending on your total taxable income and filing status. See the full rate table in Section 2 above.

4. What is the short-term capital gains tax rate in 2026?

Your ordinary income tax rate — between 10% and 37%. There is no preferential rate for short-term gains.

5. Do I pay capital gains tax on crypto in 2026?

Yes. The IRS treats cryptocurrency as property. Every sale is a taxable event subject to standard short-term or long-term capital gains rates.

6. What is the NIIT and will it affect me?

The Net Investment Income Tax is a 3.8% surtax applied to investment income for single filers earning over $200,000 or married filers earning over $250,000. It can push your effective long-term rate to 23.8%.

7. What is cost basis and how do I calculate it?

Cost basis is generally what you paid for the asset plus purchase fees. Our calculator supports FIFO and average-cost methods to calculate your adjusted basis accurately across multiple buy lots.

8. Can I legally reduce my capital gains tax?

Yes — through holding assets over 12 months, tax-loss harvesting, maxing out tax-advantaged accounts, gifting appreciated assets, or using the 0% bracket strategically. See Section 5 for the full expert strategy guide.

9. What changed for capital gains tax in 2026?

Income thresholds increased ~2.7% due to inflation adjustments. The OBBBA permanently locked in the 0/15/20% rate structure. See the full 2026 vs. 2025 comparison in Section 2.

10. Does this calculator work for real estate gains?

Yes. Enter your purchase price as cost basis, sale price, any improvement costs as basis adjustments, sale fees, and holding period. Remember to account for the $250K/$500K home sale exclusion separately.

11. Is capital gains tax the same in every state?

No. States like California (up to 13.3%) and New York (up to 10.9%) apply their own rates on top of federal. Florida, Texas, Nevada, and Wyoming have no state capital gains tax. Always factor in your state’s rate when using the capital gains calculator for planning.

Disclaimer: This capital gains tax calculator and all content on this page are for educational and informational purposes only and do not constitute financial, tax, or legal advice. Tax laws are complex and subject to change. Capital gains tax estimates are based solely on the data you input and may not reflect your full tax situation. Always consult a qualified CPA, tax attorney, or CFP® before making investment or tax decisions. FinanceAuthorityHub.com is not a registered tax advisor.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.