CD Calculator: See Your 2026 Earnings Instantly

CD Calculator (Certificate of Deposit)

Estimate CD growth with APY/APR, compounding, optional interest payout, optional monthly contributions (not all CDs allow), taxes, and an early-withdrawal scenario.

Inputs

Results

Maturity balance (CD balance)

—

Maturity date: —

Total interest earned

—

Interest paid out: —

Effective APY / Nominal APR

Effective APY: —

Nominal APR: —

Total value (balance + paid-out)

—

Total contributions: —

Tax estimate (optional)

Tax on interest: — • After-tax interest: —

After-tax total (contrib + after-tax interest): —

Early withdrawal scenario (estimate)

Withdraw date: —

Balance then: — • Paid-out then: —

Penalty: — • Net proceeds: —

Approx annualized return: —

Yearly summary

| Year | Contributions | Interest earned | Interest paid out | Ending balance |

|---|

Monthly schedule

| Month | Start balance | Contribution | Interest earned | Interest paid out | End balance | Paid-out total |

|---|

Results appear after you click “Calculate.”

In This Article

What Is a CD Calculator and How Does It Work?

A CD calculator computes exactly how much money your certificate of deposit will earn — before you open an account. Enter your deposit amount, APY, and term length, and it instantly shows your maturity value, total interest earned, and after-tax take-home.

Unlike a standard savings account, a CD locks your money for a fixed term in exchange for a guaranteed, higher interest rate. The CD calculator above removes all the guesswork.

Key Takeaway: A certificate of deposit calculator shows your exact maturity balance, total CD interest earned, and after-tax earnings — before you commit a single dollar.

Why use it in 2026? After three consecutive Fed rate cuts in late 2025, the federal funds rate now sits at a target range of 3½ to 3¾ percent — and CD rates are trending lower. Locking in today’s rates of 4%+ using a CD calculator could be one of the smartest financial moves you make this year.

Use our full suite of free financial tools to plan every part of your savings and investment strategy.

How to Use This CD Calculator: Step-by-Step

Most CD calculators ask for three fields. Ours has six advanced inputs — each one designed to show you a more accurate real-world result. Here’s exactly what each field does.

Step 1 — Enter Your Initial Deposit (Principal)

This is the amount you plan to lock into the CD. Most banks require a minimum of $500–$1,000. Larger deposits earn more total interest in dollar terms, even at the same APY.

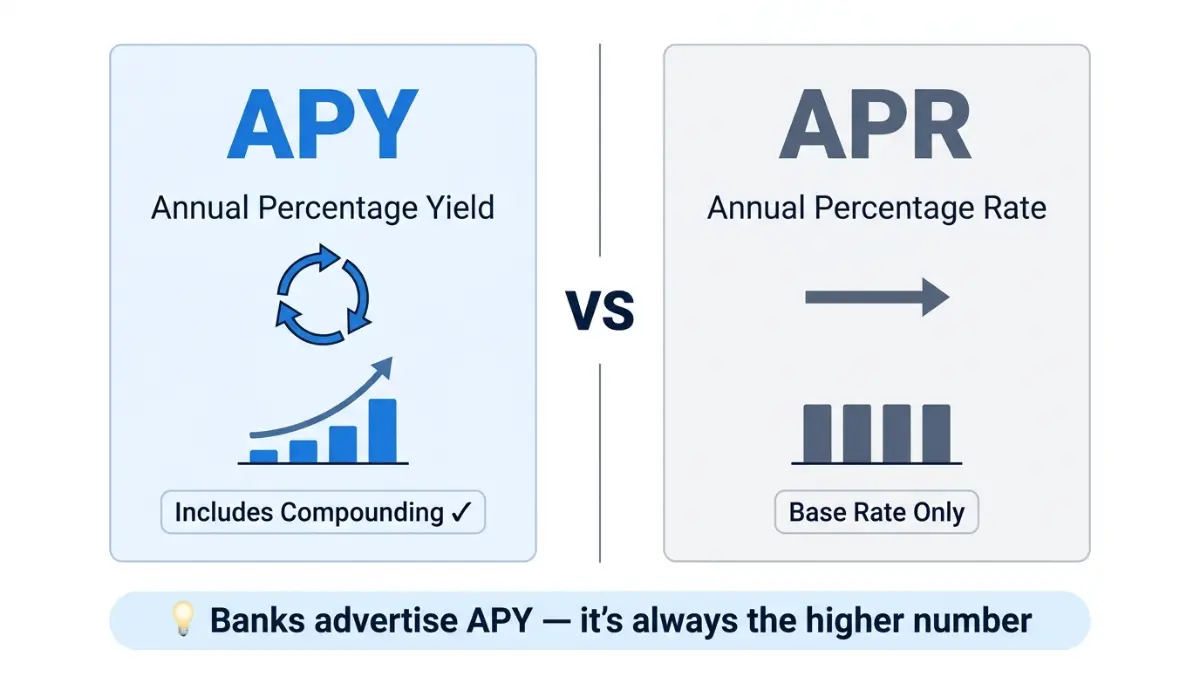

Step 2 — Choose APY or APR and Enter Your Rate

This is where most savers get confused. Here’s the difference:

| Rate Type | What It Means | Best Used For |

|---|---|---|

| APY (Annual Percentage Yield) | Effective annual rate including compounding | Comparing CD offers across banks |

| APR (Nominal Annual Rate) | Base rate before compounding effects | Calculating exact monthly interest |

Banks advertise APY because it’s the higher-looking number. Our CD calculator accepts both — just select which one your bank quoted you. For a deeper breakdown, read our full guide on APR vs. interest rate.

Step 3 — Select Compounding Frequency

Compounding frequency determines how often interest is added to your balance. Here’s what it means for $10,000 at 4.00% APR over 1 year:

| Compounding | End Balance | Total Interest |

|---|---|---|

| Daily | $10,408.08 | $408.08 |

| Monthly | $10,407.42 | $407.42 |

| Quarterly | $10,406.04 | $406.04 |

| Annually | $10,400.00 | $400.00 |

Daily compounding earns you $8.08 more on a $10,000 CD than annual compounding. Small difference on one CD — significant across a ladder. The FDIC confirms that deposit insurance covers principal plus any accrued interest through the date of default, so every dollar of compounded interest is protected too.

Step 4 — Interest Treatment: Reinvest or Pay Out

- Reinvest (Compound Growth): Interest stays in the CD and earns more interest. Best for building maximum maturity value.

- Pay Out: Interest is transferred out monthly or quarterly. Best if you need income now.

Most CD holders choose reinvest — it maximizes the compound growth effect over the full term.

Step 5 — Optional Advanced Inputs

Our CD interest calculator includes three optional fields that competitors skip entirely:

- Tax Rate: Enter your federal bracket (e.g., 22%) to see real after-tax earnings. CD interest is taxed as ordinary income — this matters more than most people realize.

- Monthly Contributions: Some specialty CDs allow ongoing deposits. Toggle this on if yours does.

- Early Withdrawal Scenario: Enter the month you might withdraw and the penalty term (in months of interest forfeited) to see your actual net proceeds.

Competitor Gap: Bankrate and NerdWallet’s CD calculators don’t show tax estimates or early withdrawal penalty math. Ours does — because those numbers change your real return significantly.

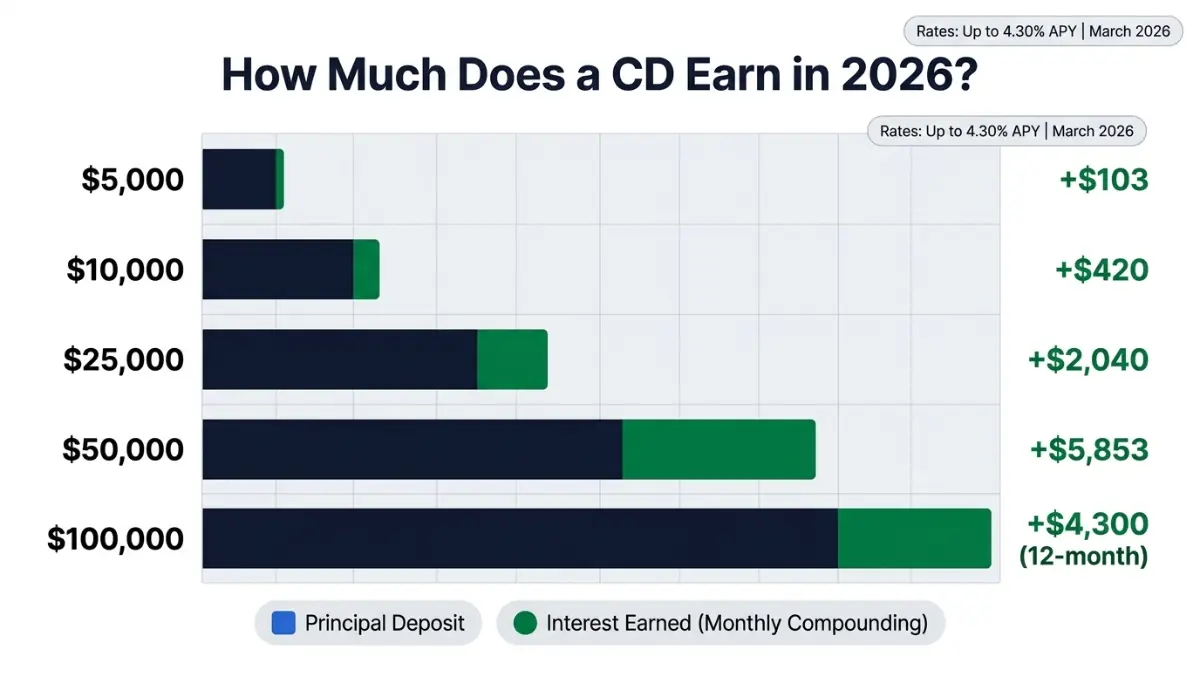

CD Calculator in Action: Real 2026 Earnings Examples

Here’s exactly what different deposit amounts earn at current top 2026 CD rates — modeled directly through the calculator above.

“With rates still above 4%, locking in a 12-month CD before further Fed cuts is a low-risk move most savers should seriously consider in Q1 2026.” — Laura M. Bennett, CFP®, FinanceAuthorityHub.com Expert Panel

Real-Money 2026 Scenarios

| Deposit | APY | Term | Total Interest | After-Tax (22%) | Maturity Value |

|---|---|---|---|---|---|

| $5,000 | 4.10% | 6 months | ~$103 | ~$80 | ~$5,103 |

| $10,000 | 4.20% | 12 months | ~$420 | ~$328 | ~$10,420 |

| $25,000 | 4.00% | 24 months | ~$2,040 | ~$1,591 | ~$27,040 |

| $50,000 | 3.80% | 36 months | ~$5,853 | ~$4,565 | ~$55,853 |

| $100,000 | 4.30% | 12 months | ~$4,300 | ~$3,354 | ~$104,300 |

Calculated with monthly compounding and interest reinvested. Results are estimates.

The Early Withdrawal Trap — A Real Example

Say you open a 2-year CD at $10,000 and 4.00% APY, but withdraw at month 6. Your bank applies a 6-month interest penalty.

- Earned interest by month 6: ~$200

- Penalty (6 months of interest): ~$200

- Net earnings after penalty: ~$0

You essentially earned nothing. This is why the early withdrawal scenario tool in our CD calculator is critical — always model this before you commit. For comparison, run the same numbers through our savings calculator to see if a high-yield savings account offers better flexibility for your timeline.

CD vs. Leaving Money in a Regular Savings Account

On $10,000 over 12 months in 2026:

- Top CD (4.20% APY): Earns ~$420

- National average savings account (0.39% APY): Earns ~$39

- Difference: $381 — just for locking funds for 12 months

CD Strategy in 2026: Should You Lock In Now?

This is the question every saver is asking in 2026. Here’s the data-driven answer.

The 2026 Rate Environment: What the Fed Cuts Mean for Your CD

The Fed lowered the federal funds rate target to 3½ to 3¾ percent in December 2025, the third cut of the year. At the January 2026 FOMC meeting, the Committee held rates steady — but signaled further cuts remain possible if inflation continues cooling.

What this means for your certificate of deposit strategy:

- CD rates are falling — the top 1-year CD rates have dropped from 5%+ in 2023 to approximately 4.10–4.30% in March 2026.

- The window to lock in 4%+ is narrowing. Every Fed cut that follows will push bank CD rates lower.

- Savers who lock in now protect their yield for the full term — even if rates drop further.

See how the Federal Reserve’s rate decisions directly influence what banks offer on certificates of deposit.

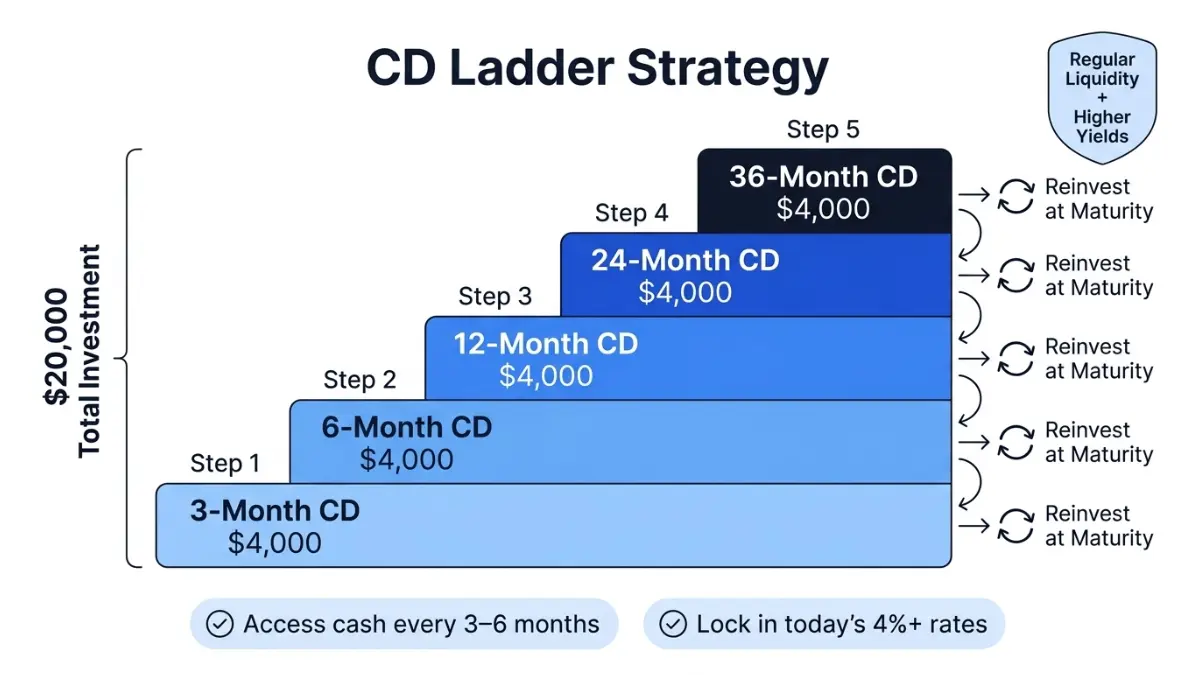

CD Ladder Strategy — The Smartest Way to Use Multiple CDs

A CD ladder splits your total deposit across multiple CDs with staggered maturity dates. This gives you the benefits of higher long-term rates while maintaining regular access to portions of your money.

Example: $20,000 CD Ladder

| Rung | Amount | Term | Approx. APY | Matures |

|---|---|---|---|---|

| 1 | $4,000 | 3 months | 3.90% | June 2026 |

| 2 | $4,000 | 6 months | 4.00% | Sept 2026 |

| 3 | $4,000 | 12 months | 4.20% | March 2027 |

| 4 | $4,000 | 24 months | 4.00% | March 2028 |

| 5 | $4,000 | 36 months | 3.80% | March 2029 |

- Every 3–6 months, one CD matures — giving you access to cash.

- You reinvest each matured CD into a new 36-month term to maintain the ladder.

- Result: Higher average yield than a single short-term CD, with built-in liquidity.

After each CD matures, evaluate your full financial picture. Our compound interest calculator can help you model reinvestment scenarios.

CD vs. High-Yield Savings Account in 2026

| Feature | CD (12-month) | High-Yield Savings Account |

|---|---|---|

| APY (March 2026) | Up to 4.30% | Up to 4.75% (variable) |

| Rate guarantee | Fixed for full term ✅ | Variable — can drop anytime ❌ |

| Liquidity | Penalty to exit early ❌ | Withdraw anytime ✅ |

| Best for | Locked savings goals | Emergency fund, flexible savings |

Bottom line: If you might need the money within 90 days, keep it in a high-yield savings account. If you can commit to a fixed term, the CD’s guaranteed rate wins in a declining-rate environment. To explore how to build long-term tax-advantaged savings alongside CDs, check our guide to Roth IRA 2026.

IRA CD — Tax-Advantaged CD Strategy

An IRA CD combines the guaranteed return of a certificate of deposit with the tax advantages of an Individual Retirement Account.

- Traditional IRA CD: Contributions may be tax-deductible; growth taxed on withdrawal.

- Roth IRA CD: Contributions from after-tax dollars; withdrawals in retirement are tax-free.

- 2026 IRA contribution limit: $7,000 (under 50) or $8,000 (50+).

For retirement-focused savers, pairing an IRA CD with a broader retirement strategy is worth modeling in our retirement calculator.

Types of CDs You Can Calculate — and What Protects Your Money

Our CD calculator works for all standard CD types. Here’s what each one means for your earnings and flexibility.

CD Types at a Glance

| CD Type | Best For | Rate vs. Standard | Early Exit? |

|---|---|---|---|

| Traditional CD | Max guaranteed yield | Highest | Penalty applies |

| No-Penalty CD | Flexibility + decent yield | Slightly lower | Yes, after 7 days |

| Bump-Up CD | Rising rate environments | Lower | No |

| Jumbo CD | $100,000+ deposits | Marginally higher | No |

| Step-Up CD | Automatic rate increases | Lower to start | No |

| IRA CD | Retirement savers | Same as standard | IRA rules apply |

| Brokered CD | Brokerage account holders | Competitive | Secondary market |

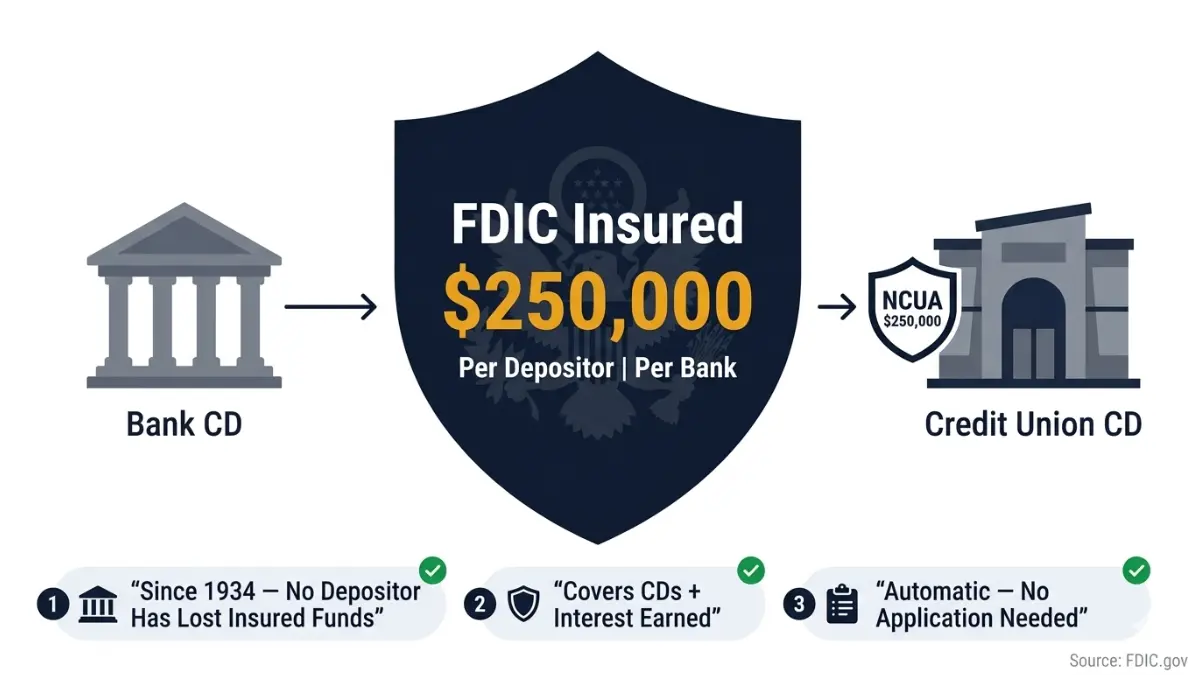

FDIC vs. NCUA Insurance — What’s Covered

Every dollar you deposit in an FDIC-insured bank’s CD is protected up to strict limits. FDIC deposit insurance covers Certificates of Deposit and protects your money automatically when you open an account — up to $250,000 per depositor, per FDIC-insured bank, per ownership category.

Key rules to know:

- Joint accounts: Each co-owner is insured separately, up to $250,000 each.

- Multiple banks: You can hold $250,000 at Bank A and $250,000 at Bank B — both fully covered.

- Credit union CDs: Protected by the NCUA (National Credit Union Administration), same $250,000 limit.

- Deposits over $250,000: Spread across multiple FDIC-insured institutions to maintain full coverage.

Verify any bank’s FDIC status using the official FDIC BankFind tool.

The CD Maturity Rollover Trap — What Competitors Don’t Tell You

This is the #1 mistake CD holders make. When your CD matures, most banks automatically roll it over into a new CD at the current rate — which may be significantly lower than your original rate.

How to avoid it:

- Set a calendar alert 7–10 days before your maturity date.

- Review current rates before the grace period closes (typically 7–14 days).

- Compare rates across institutions — your current bank rarely offers the best renewal rate.

- Consider redirecting funds into a high-APY savings account while you shop for the best new CD term.

If you’re also planning major purchases alongside your CD savings, use our home affordability calculator to balance your savings timeline with your goals.

How the CD Calculator Computes Your Earnings

Our certificate of deposit calculator uses the standard compound interest formula, identical to what banks use internally.

The Formula

A = P × (1 + r/n)^(n × t)

Where:

- A = Final maturity balance

- P = Principal (initial deposit)

- r = Annual interest rate as a decimal (e.g., 4.00% = 0.04)

- n = Compounding periods per year (12 for monthly, 365 for daily)

- t = Term in years

Plain English: Your principal grows each compounding period. The new, slightly-larger balance then earns interest in the next period. This snowball effect is compound interest — and it’s why daily compounding beats annual compounding on the same rate.

APY to APR Conversion

When you enter an APY, the calculator back-converts to a nominal APR using:

APR = n × [(1 + APY)^(1/n) − 1]

This ensures the compounding schedule matches your bank’s actual method accurately.

Tax Estimate Methodology

The optional tax estimate applies your entered tax rate to total interest earned only — not your principal. For example:

- $10,000 CD at 4.20% for 12 months = $420 in interest

- At 22% federal bracket: $92.40 in taxes

- After-tax earnings: $327.60

CD interest is reported on Form 1099-INT by your bank each January. For a full breakdown of how investment income is taxed, the IRS Publication 550 covers investment income and expenses in detail.

Transparency note: All results from this CD calculator are estimates. Actual earnings may vary based on your institution’s exact compounding schedule, any account fees, and applicable state taxes.

Frequently Asked Questions about CD Calculator

1. What is a CD calculator used for?

A CD calculator estimates how much interest you’ll earn on a certificate of deposit based on your principal, APY or APR, compounding frequency, and term length. It helps you compare CD offers and plan your savings before opening an account.

2. How do I calculate CD interest manually?

Use the formula: A = P × (1 + r/n)^(n×t). For a $10,000 CD at 4% APY with monthly compounding for 1 year: A = 10,000 × (1 + 0.04/12)^12 = approximately $10,407. The CD calculator above does this instantly for any scenario.

3. What is the difference between APY and APR on a CD?

APY (Annual Percentage Yield) reflects your actual annual return after compounding. APR (Annual Percentage Rate) is the base rate before compounding. Banks advertise APY because it’s higher. A 4.00% APR compounding monthly equals an APY of approximately 4.074%.

4. Does compounding frequency affect my CD earnings?

Yes, but modestly on short terms. Daily compounding earns slightly more than monthly, which earns more than annual. On $10,000 at 4% for 1 year, daily compounding earns about $8 more than annual compounding. The difference grows significantly on larger deposits and longer terms.

5. Is CD interest taxable in the USA?

Yes. CD interest is taxed as ordinary income in the year it is earned or credited — not just when you withdraw it. Your bank sends a Form 1099-INT in January covering the prior year’s earnings. Consider holding CDs inside a Roth IRA or Traditional IRA to defer or eliminate this tax.

6. What is the early withdrawal penalty on a CD?

Most banks charge between 3 and 12 months of interest as an early withdrawal penalty, depending on the CD term length. Longer terms carry heavier penalties. Always model the early withdrawal scenario in the CD calculator above before committing to a term.

7. What is a CD ladder and how does it work?

A CD ladder splits your total investment across multiple CDs with different maturity dates (e.g., 3-month, 6-month, 12-month, 24-month, 36-month). As each CD matures, you reinvest at the longest term. This strategy provides regular liquidity while capturing higher long-term rates.

8. Are CDs FDIC insured?

Yes. CDs held at FDIC-insured banks are protected up to $250,000 per depositor, per bank, per ownership category. Credit union CDs are covered by the NCUA under the same $250,000 limit. No depositor has lost FDIC-insured funds since 1934.

9. What happens when my CD matures?

When a CD reaches its maturity date, most banks automatically roll it over into a new CD at the current rate. You typically have a 7–14 day grace period to withdraw, reinvest, or move funds penalty-free. Always review rates before this window closes — don’t let your bank silently lock you into a lower rate.

10. Can I add money to a CD after opening?

Standard CDs do not allow additional contributions after opening. Some banks offer “add-on CDs” that permit ongoing deposits during the term. The CD calculator’s optional monthly contribution field is designed for these specialty products.

11. What are the best CD rates in 2026?

As of March 2026, top 1-year CD rates range from 4.00% to 4.30% APY at online banks and credit unions. After the Federal Reserve made three consecutive rate cuts in September, October, and December 2025, CD rates have continued declining into 2026 — but remain historically strong compared to the near-zero rates of 2020–2021. Use the CD calculator above with your exact deposit and preferred term to model your specific scenario.

Disclaimer

This article and the CD calculator tool are provided for educational and informational purposes only. Results are estimates and do not constitute financial advice. Actual CD earnings may vary based on your institution’s compounding schedule, fees, and applicable tax rates. CD interest tax treatment depends on your individual circumstances — consult a qualified financial advisor or tax professional before making investment decisions. FDIC/NCUA insurance limits are subject to change; verify coverage at fdic.gov.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.