Inside a Personal Injury Structured Settlement Negotiation

Personal injury structured settlement talks involve five parties and one irreversible signature. Know who’s across the table before you negotiate.

Personal injury structured settlement talks involve five parties and one irreversible signature. Know who’s across the table before you negotiate.

Lump sum vs structured settlement: the 2026 NPV math reveals what break-even return rate you need before a factoring offer makes financial sense.

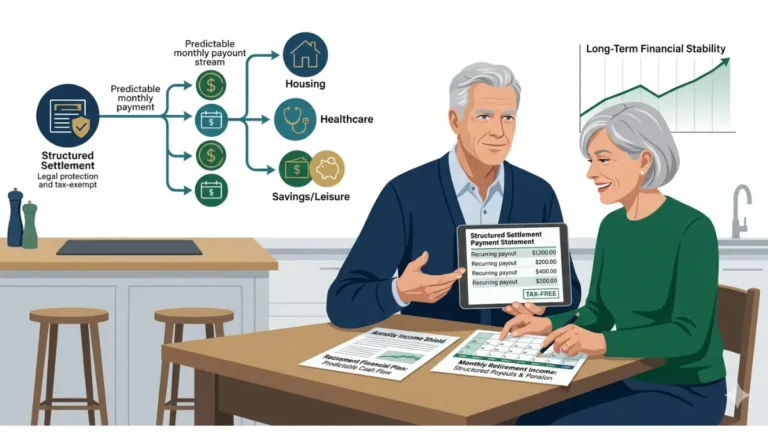

Structured settlement retirement income is federally tax-free — but one IRS carve-out and a factoring decision can erase $30,000. Know both rules first.

Structured settlement taxes under IRC §104 can stay excluded, but one Form 1099 mistake may trigger IRS correspondence and amended returns.

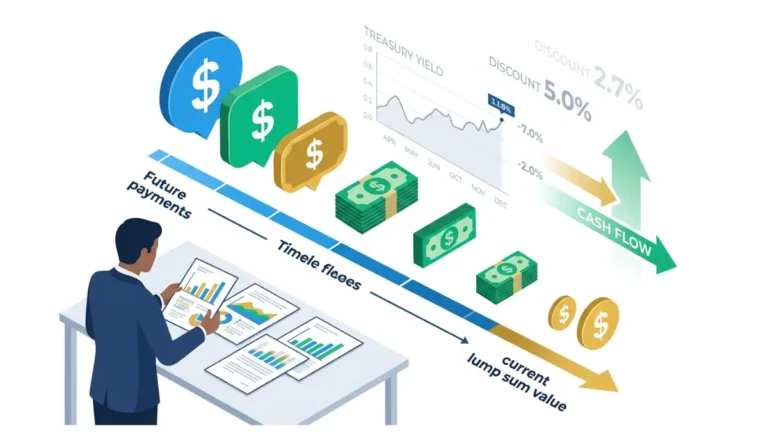

Structured settlement present value isn’t face value — a 2026 CFA calculation shows why $360,000 in payments may be worth just $124,200 to a buyer.

Sell structured settlement credit score concerns stem from confusion about FICO reporting, hard inquiries, and mortgage income verification rules.

Structured settlement loans aren’t loans — factoring companies charge 45% APR while quoting 13%. A CFA breaks down the legal block and the true cost.

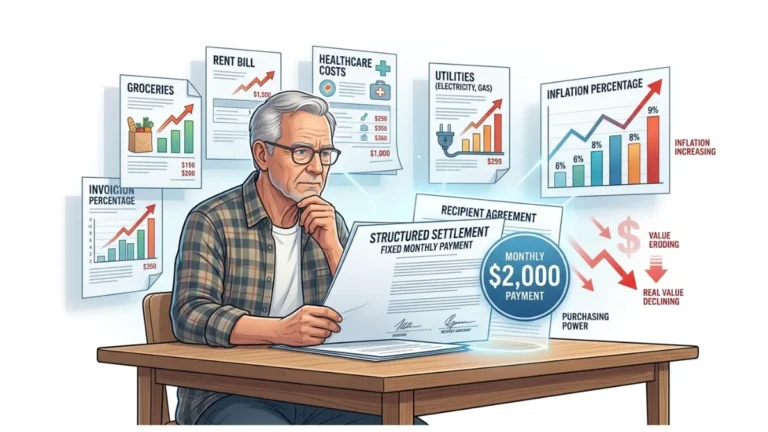

Structured settlement inflation is silently erasing your purchasing power — a $2,000 monthly payment started in 2006 is now worth just $1,126.

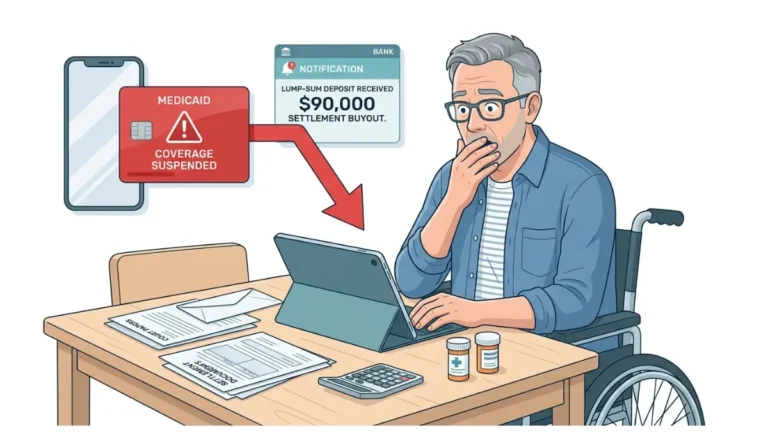

Structured settlement Medicaid rules work against you the moment a lump sum arrives — CMS’s 2026 $2,000 asset limit can suspend coverage that same day.

Structured settlement scams cost recipients $40,200 on a single deal when discount rates exceed the 2026 NSSTA fair-market threshold of 11.4%.