What a Variable Annuity Really Costs You

A variable annuity blends market growth with insurance — but its ~1.25% M&E fee, surrender charges, and 10% early-withdrawal penalty hide the real cost.

A variable annuity blends market growth with insurance — but its ~1.25% M&E fee, surrender charges, and 10% early-withdrawal penalty hide the real cost.

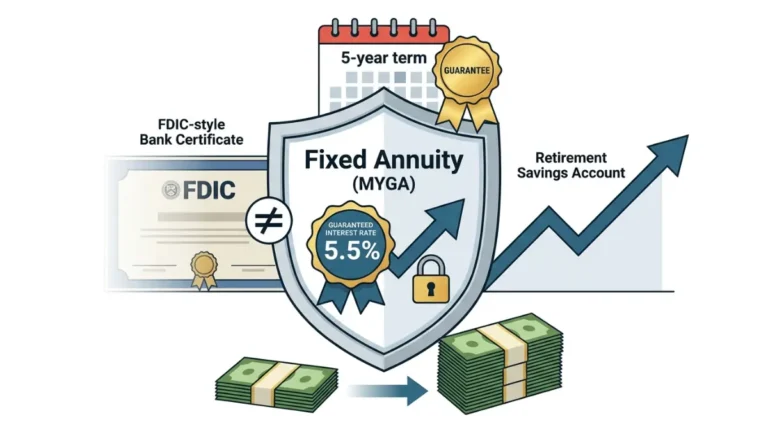

Fixed annuity rates look attractive right now, but the real cost of a MYGA shows up if you cash out before 59½. Here’s how they actually work.

The types of annuities aren’t interchangeable: fixed locks a rate, variable rides the market, indexed caps gains behind a 0% floor. Here’s which fits.

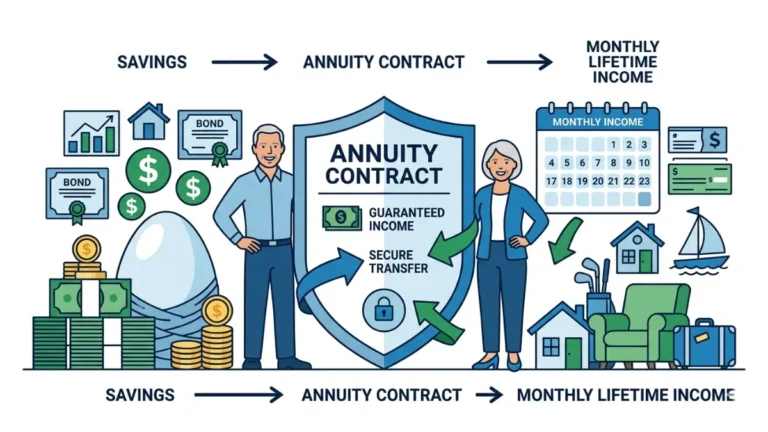

How annuities work comes down to two phases and their cost. The honest version: payouts, the 10% penalty before 59½, and the fees that erode returns.

Is an annuity worth it? The answer is in the fees — near zero on a fixed annuity, over 3% a year on a variable one. Here’s how to decide.

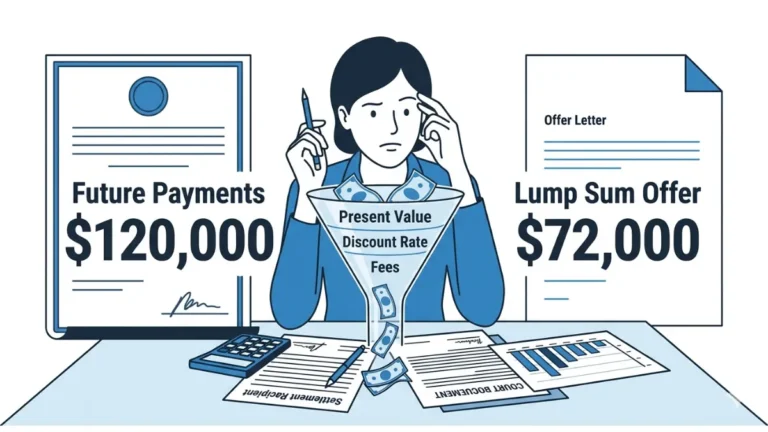

Structured settlement payments of $1,500 a month feel safe—until a buyer offers cash. See the real cost, court approval, and keep-or-sell math.

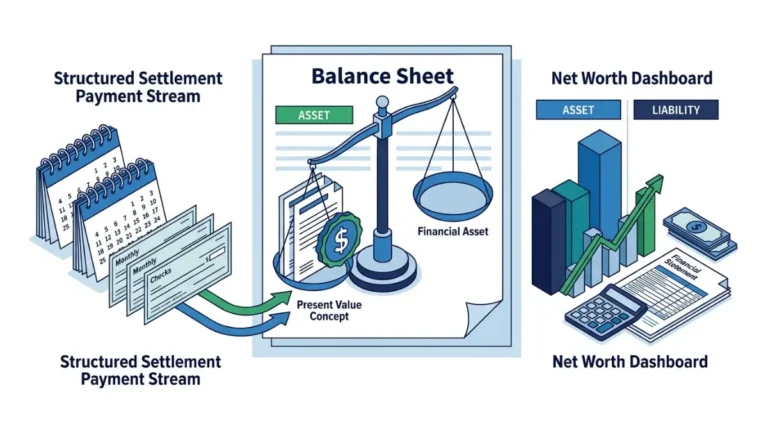

Structured settlement net worth confuses most people—it’s present value, not face total. Here’s the right number for every form you fill out.

Structured settlement factoring requires court approval and a ‘best interest’ finding — see the four inputs that shape your lump-sum offer.

Florida structured settlement sales need court approval, and the payout runs well below face value. See the 45–90 day process and what you keep.

A structured settlement cash advance is legal only with a judge’s approval — and a 2026 personal loan near 12% APR often costs far less.