The 1982 Law Behind Tax-Free Structured Settlements

Structured settlement payments escape federal income tax because of one 1982 law—and a later rule decides who pays the 40% tax when you sell.

Structured settlement payments escape federal income tax because of one 1982 law—and a later rule decides who pays the 40% tax when you sell.

Qualified assignments make injury settlements tax-free under IRC 130—but selling those payments can trigger a 40% tax most sellers never see coming.

Structured settlement money never counts toward the $184,500 Social Security wage base or your self-employment tax—see why, and what still gets taxed.

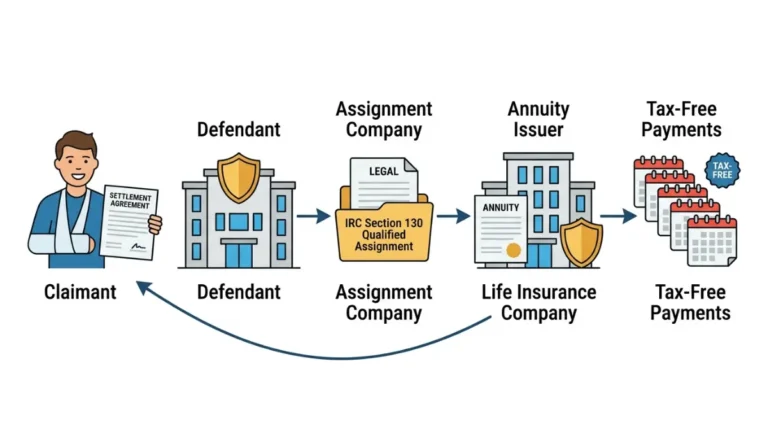

Personal injury structured settlement talks involve five parties and one irreversible signature. Know who’s across the table before you negotiate.

Received a structured settlement offer? A CFA explains the tax-free rules and the one move to make before you sign.

Structured settlement payments taxable? IRC Section 104(a)(2) excludes most — but selling triggers a 40% excise under IRC 5891. Here’s the IRS test that controls your answer.

Structured settlement factoring companies charge effective annual rates

between 9% and 29% — a gap that costs recipients $314,000 or more on a $500,000

payment stream.